Part I – Cavco Industries Inc (CVCO) Reports 21.7% Decline in Net Revenue

| Three Months Ended | |||||||||||||||||||||||

| ($ in thousands, except revenue per home sold) | September 30, 2023 |

October 1, 2022 |

Change | ||||||||||||||||||||

| Net revenue | |||||||||||||||||||||||

| Factory-built housing | $ | 434,066 | $ | 559,602 | $ | (125,536) | (22.4) | % | |||||||||||||||

| Financial services | 17,964 | 17,790 | 174 | 1.0 | % | ||||||||||||||||||

| $ | 452,030 | $ | 577,392 | $ | (125,362) | (21.7) | % | ||||||||||||||||

| Factory-built modules sold | 6,912 | 8,863 | (1,951) | (22.0) | % | ||||||||||||||||||

| Factory-built homes sold (consisting of one or more modules) | 4,248 | 5,111 | (863) | (16.9) | % | ||||||||||||||||||

| Net factory-built housing revenue per home sold | $ | 102,181 | $ | 109,490 | $ | (7,309) | (6.7) | % | |||||||||||||||

| Six Months Ended | |||||||||||||||||||||||

| ($ in thousands, except revenue per home sold) | September 30, 2023 |

October 1, 2022 |

Change | ||||||||||||||||||||

| Net revenue | |||||||||||||||||||||||

| Factory-built housing | $ | 891,175 | $ | 1,132,199 | $ | (241,024) | (21.3) | % | |||||||||||||||

| Financial services | 36,730 | 33,531 | 3,199 | 9.5 | % | ||||||||||||||||||

| $ | 927,905 | $ | 1,165,730 | $ | (237,825) | (20.4) | % | ||||||||||||||||

| Factory-built modules sold | 14,318 | 18,105 | (3,787) | (20.9) | % | ||||||||||||||||||

| Factory-built homes sold (consisting of one or more modules) | 8,830 | 10,457 | (1,627) | (15.6) | % | ||||||||||||||||||

| Net factory-built housing revenue per home sold | $ | 100,926 | $ | 108,272 | $ | (7,346) | (6.8) | % | |||||||||||||||

| Three Months Ended | |||||||||||||||||||||||

| ($ in thousands) | September 30, 2023 |

October 1, 2022 |

Change | ||||||||||||||||||||

| Gross profit | |||||||||||||||||||||||

| Factory-built housing | $ | 100,507 | $ | 149,665 | $ | (49,158) | (32.8) | % | |||||||||||||||

| Financial services | 6,450 | 7,934 | (1,484) | (18.7) | % | ||||||||||||||||||

| $ | 106,957 | $ | 157,599 | $ | (50,642) | (32.1) | % | ||||||||||||||||

| Gross profit as % of Net revenue | |||||||||||||||||||||||

| Consolidated | 23.7 | % | 27.3 | % | N/A | (3.6) | % | ||||||||||||||||

| Factory-built housing | 23.2 | % | 26.7 | % | N/A | (3.5) | % | ||||||||||||||||

| Financial services | 35.9 | % | 44.6 | % | N/A | (8.7) | % | ||||||||||||||||

| Selling, general and administrative expenses | |||||||||||||||||||||||

| Factory-built housing | $ | 56,455 | $ | 61,640 | $ | (5,185) | (8.4) | % | |||||||||||||||

| Financial services | 5,051 | 5,254 | (203) | (3.9) | % | ||||||||||||||||||

| $ | 61,506 | $ | 66,894 | $ | (5,388) | (8.1) | % | ||||||||||||||||

| Income from operations | |||||||||||||||||||||||

| Factory-built housing | $ | 44,052 | $ | 88,025 | $ | (43,973) | (50.0) | % | |||||||||||||||

| Financial services | 1,399 | 2,680 | (1,281) | (47.8) | % | ||||||||||||||||||

| $ | 45,451 | $ | 90,705 | $ | (45,254) | (49.9) | % | ||||||||||||||||

| Six Months Ended | |||||||||||||||||||||||

| ($ in thousands) | September 30, 2023 |

October 1, 2022 |

Change | ||||||||||||||||||||

| Gross profit | |||||||||||||||||||||||

| Factory-built housing | $ | 213,875 | $ | 289,251 | $ | (75,376) | (26.1) | % | |||||||||||||||

| Financial services | 10,961 | 13,072 | (2,111) | (16.1) | % | ||||||||||||||||||

| $ | 224,836 | $ | 302,323 | $ | (77,487) | (25.6) | % | ||||||||||||||||

| Gross profit as % of Net revenue | |||||||||||||||||||||||

| Consolidated | 24.2 | % | 25.9 | % | N/A | (1.7) | % | ||||||||||||||||

| Factory-built housing | 24.0 | % | 25.5 | % | N/A | (1.5) | % | ||||||||||||||||

| Financial services | 29.8 | % | 39.0 | % | N/A | (9.2) | % | ||||||||||||||||

| Selling, general and administrative expenses | |||||||||||||||||||||||

| Factory-built housing | $ | 112,476 | $ | 122,563 | $ | (10,087) | (8.2) | % | |||||||||||||||

| Financial services | 10,710 | 10,467 | 243 | 2.3 | % | ||||||||||||||||||

| $ | 123,186 | $ | 133,030 | $ | (9,844) | (7.4) | % | ||||||||||||||||

| Income from operations | |||||||||||||||||||||||

| Factory-built housing | $ | 101,399 | $ | 166,688 | $ | (65,289) | (39.2) | % | |||||||||||||||

| Financial services | 251 | 2,605 | (2,354) | (90.4) | % | ||||||||||||||||||

| $ | 101,650 | $ | 169,293 | $ | (67,643) | (40.0) | % | ||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||

| ($ in thousands, except per share amounts) | September 30, 2023 |

October 1, 2022 |

Change | ||||||||||||||||||||

| Net income attributable to Cavco common stockholders | $ | 41,539 | $ | 74,116 | $ | (32,577) | (44.0) | % | |||||||||||||||

| Diluted net income per share | $ | 4.76 | $ | 8.25 | $ | (3.49) | (42.3) | % | |||||||||||||||

| Six Months Ended | |||||||||||||||||||||||

| ($ in thousands, except per share amounts) | September 30, 2023 |

October 1, 2022 |

Change | ||||||||||||||||||||

| Net income attributable to Cavco common stockholders | $ | 87,896 | $ | 133,718 | $ | (45,822) | (34.3) | % | |||||||||||||||

| Diluted net income per share | $ | 10.05 | $ | 14.88 | $ | (4.83) | (32.5) | % | |||||||||||||||

| Three Months Ended | Six Months Ended | |||||||||||||||||||||||||

| ($ in millions) | September 30, 2023 |

October 1, 2022 |

September 30, 2023 |

October 1, 2022 |

||||||||||||||||||||||

| Net revenue | ||||||||||||||||||||||||||

| Unrealized (losses) recognized during the period on securities held in the financial services segment | $ | (0.3) | $ | — | $ | — | $ | (1.2) | ||||||||||||||||||

| Selling, general and administrative expenses | ||||||||||||||||||||||||||

|

Expenses incurred in engaging third-party consultants in relation to the non-recurring energy efficient home tax credits

|

— | (1.9) | — | (4.5) | ||||||||||||||||||||||

| Legal and other expense related to the Securities and Exchange Commission inquiry | (0.7) | (1.4) | (1.0) | (2.8) | ||||||||||||||||||||||

| Other income, net | ||||||||||||||||||||||||||

| Corporate unrealized gains (losses) recognized during the period on securities held | — | — | 0.1 | (1.1) | ||||||||||||||||||||||

(Dollars in thousands, except per share amounts)

| September 30, 2023 |

April 1, 2023 |

||||||||||

| ASSETS | (Unaudited) | ||||||||||

| Current assets | |||||||||||

| Cash and cash equivalents | $ | 377,264 | $ | 271,427 | |||||||

| Restricted cash, current | 17,180 | 11,728 | |||||||||

| Accounts receivable, net | 88,560 | 89,347 | |||||||||

| Short-term investments | 14,358 | 14,978 | |||||||||

| Current portion of consumer loans receivable, net | 10,503 | 17,019 | |||||||||

| Current portion of commercial loans receivable, net | 48,583 | 43,414 | |||||||||

| Current portion of commercial loans receivable from affiliates, net | 1,959 | 640 | |||||||||

| Inventories | 244,476 | 263,150 | |||||||||

| Prepaid expenses and other current assets | 72,560 | 92,876 | |||||||||

| Total current assets | 875,443 | 804,579 | |||||||||

| Restricted cash | 585 | 335 | |||||||||

| Investments | 20,507 | 18,639 | |||||||||

| Consumer loans receivable, net | 25,233 | 27,129 | |||||||||

| Commercial loans receivable, net | 40,998 | 53,890 | |||||||||

| Commercial loans receivable from affiliates, net | 2,928 | 4,033 | |||||||||

| Property, plant and equipment, net | 223,664 | 228,278 | |||||||||

| Goodwill | 116,015 | 114,547 | |||||||||

| Other intangibles, net | 29,005 | 29,790 | |||||||||

| Operating lease right-of-use assets | 34,413 | 26,755 | |||||||||

| Total assets | $ | 1,368,791 | $ | 1,307,975 | |||||||

| LIABILITIES, REDEEMABLE NONCONTROLLING INTEREST, AND STOCKHOLDERS’ EQUITY | |||||||||||

| Current liabilities | |||||||||||

| Accounts payable | $ | 41,095 | $ | 30,730 | |||||||

| Accrued expenses and other current liabilities | 264,380 | 262,661 | |||||||||

| Total current liabilities | 305,475 | 293,391 | |||||||||

| Operating lease liabilities | 30,529 | 21,678 | |||||||||

| Other liabilities | 7,792 | 7,820 | |||||||||

| Deferred income taxes | 5,740 | 7,581 | |||||||||

| Redeemable noncontrolling interest | — | 1,219 | |||||||||

| Stockholders’ equity | |||||||||||

| Preferred stock, $0.01 par value; 1,000,000 shares authorized; No shares issued or outstanding | — | — | |||||||||

|

Common stock, $0.01 par value; 40,000,000 shares authorized; Issued 9,356,421 and 9,337,125 shares, respectively

|

94 | 93 | |||||||||

|

Treasury stock, at cost; 844,742 and 671,801 shares, respectively

|

(211,646) | (164,452) | |||||||||

| Additional paid-in capital | 274,204 | 271,950 | |||||||||

| Retained earnings | 957,206 | 869,310 | |||||||||

| Accumulated other comprehensive loss | (603) | (615) | |||||||||

| Total stockholders’ equity | 1,019,255 | 976,286 | |||||||||

| Total liabilities, redeemable noncontrolling interest and stockholders’ equity | $ | 1,368,791 | $ | 1,307,975 | |||||||

| Three Months Ended | Six Months Ended | ||||||||||||||||||||||

| September 30, 2023 |

October 1, 2022 |

September 30, 2023 |

October 1, 2022 |

||||||||||||||||||||

| Net revenue | $ | 452,030 | $ | 577,392 | $ | 927,905 | $ | 1,165,730 | |||||||||||||||

| Cost of sales | 345,073 | 419,793 | 703,069 | 863,407 | |||||||||||||||||||

| Gross profit | 106,957 | 157,599 | 224,836 | 302,323 | |||||||||||||||||||

| Selling, general and administrative expenses | 61,506 | 66,894 | 123,186 | 133,030 | |||||||||||||||||||

| Income from operations | 45,451 | 90,705 | 101,650 | 169,293 | |||||||||||||||||||

| Interest income | 5,812 | 1,851 | 10,430 | 3,165 | |||||||||||||||||||

| Interest expense | (257) | (233) | (523) | (394) | |||||||||||||||||||

| Other income, net | 655 | 488 | 781 | 57 | |||||||||||||||||||

| Income before income taxes | 51,661 | 92,811 | 112,338 | 172,121 | |||||||||||||||||||

| Income tax expense | (10,088) | (18,613) | (24,354) | (38,229) | |||||||||||||||||||

| Net income | 41,573 | 74,198 | 87,984 | 133,892 | |||||||||||||||||||

| Less: net income attributable to redeemable noncontrolling interest | 34 | 82 | 88 | 174 | |||||||||||||||||||

| Net income attributable to Cavco common stockholders | $ | 41,539 | $ | 74,116 | $ | 87,896 | $ | 133,718 | |||||||||||||||

| Net income per share attributable to Cavco common stockholders | |||||||||||||||||||||||

| Basic | $ | 4.80 | $ | 8.32 | $ | 10.15 | $ | 15.01 | |||||||||||||||

| Diluted | $ | 4.76 | $ | 8.25 | $ | 10.05 | $ | 14.88 | |||||||||||||||

| Weighted average shares outstanding | |||||||||||||||||||||||

| Basic | 8,656,537 | 8,903,703 | 8,663,430 | 8,910,933 | |||||||||||||||||||

| Diluted | 8,731,419 | 8,978,997 | 8,742,734 | 8,983,425 | |||||||||||||||||||

| Three Months Ended | Six Months Ended | ||||||||||||||||||||||

| September 30, 2023 |

October 1, 2022 |

September 30, 2023 |

October 1, 2022 |

||||||||||||||||||||

| Capital expenditures | $ | 4,287 | $ | 8,181 | $ | 8,470 | $ | 33,188 | |||||||||||||||

| Depreciation | $ | 4,275 | $ | 3,836 | $ | 8,449 | $ | 7,274 | |||||||||||||||

| Amortization of other intangibles | $ | 393 | $ | 502 | $ | 785 | $ | 1,010 | |||||||||||||||

Part II – Additional Information with More MHProNews Analysis and Commentary

From the SEC document linked here are the following remarks found in “Assessing Materiality: Focusing on the Reasonable Investor When Evaluating Errors.”

MHProNews hereby notes that failure for a firm to provide accurate information, and failure to correct information that may be “material” to a “reasonable” investor can be an important legal issue.

That noted, from that same SEC document: “Management is responsible for providing investors with GAAP-compliant financial statements, so whenever a material error is identified in previously-issued financial statements,[2] investors must be notified promptly and the error must be corrected. The determination of whether an error is material is an objective assessment focused on whether there is a substantial likelihood it is important to the reasonable investor.[3]

referred to colloquially as a reissuance restatement or a “Big R” restatement.” “such errors [both Big R and little r] should be transparently disclosed to investors.” “Since the concept of materiality is focused on the total mix of information from the perspective of a reasonable investor, those who assess the materiality of errors, including registrants, auditors, audit committees, and others, should do so through the lens of the reasonable investor.”

The last remark might be worth repeating for emphasis (with bold added by MHProNews) for better understanding the analysis that follows. “Since the concept of materiality is focused on the total mix of information from the perspective of a reasonable investor, those who assess the materiality of errors, including registrants, auditors, audit committees, and others, should do so through the lens of the reasonable investor.”

MHProNews asked Bing AI the following.

> “What is a fiduciary duty in law with respect to investing in publicly traded companies?”

- Exercise due care in how they manage a corporation’s affairs

- Handle their powers only for the collective benefit of the corporation and its stockholders

- Make decisions in good faith for shareholders in a reasonably prudent manner

- Not put other interests, causes, or entities above the interest of the company and its shareholders

- Choose the best option to serve the company and its stakeholders

- Exercise their business judgment in considering and reconciling the interests of various stakeholders, including shareholders, employees, customers, suppliers, the environment and communities, and the attendant risks and opportunities for the corporation.

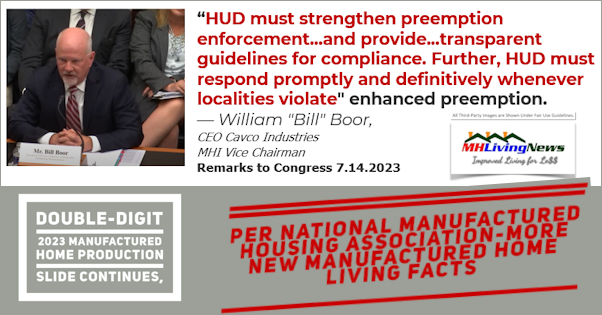

3) Boor ought to play an outsized role at MHI, given that he is their current chairman. Boor’s remarks on behalf of Cavco: “Prospective homeowners have gotten no relief from the impact of rising interest rates and the affordable housing crisis is intensifying” is arguably one more addition to the ‘indictment’ of the Arlington, VA based national trade association that he currently heads up as their corporate board leader.

4) Comparing Cavco’s quarterly results to that of the industry as a whole is a commonsense step for manufactured housing stakeholders and corporate shareholders, among others evaluating the information that Cavco’s has provided. Cavco has reportedly dropped some 22 percent, which is broadly in line with the fall in production reported by MHARR, IBTS, and other sources (see the above and below reports for details).

5) That said, affordable manufactured housing has apparently broadly performed worse than conventional housing, based upon recent reporting. See that data in the report linked below. The fact that manufactured housing is underperforming far costlier conventional housing ought to be a reason for a range of individuals, public officials, and advocates to wonder, why is this the case? What helps explain the apparently poor performance of several manufactured housing industry firms during an affordable housing crisis?

6) MHProNews will not do at this time a page-by-page “fisking” of Cavco’s latest investor pitch deck (investor presentation for November 2023). What we will do is focus this analysis to the following. The following page is from a previous Cavco Industries investor presentation. However, it is also page four of their current (November 2023) presentation (investor pitch deck).

Note: to expand this image below to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

that the industry ought to expect this current downturn because more expensive site-built housing is also in a downturn? MHI’s research and reasoning are arguably a classic example of PALTERING and the use of a RED HERRING logical fallacy. Note: depending on your browser or device, many images in this report and others on MHProNews can be clicked to expand. Click the image and follow the prompts. For example, in some browsers/devices you click the image and select ‘open in a new window.’ After clicking that selection, you click the image in the open window to expand the image to a larger size. To return to this page, use your back key, escape or follow the prompts.

According to a search using Bing AI, the quotation above from the National Association of Home Builders CEO Jerry Howard is based upon remarks he made to Fox Business on the Varney and Company program on 11.22.2022. The precise quoted remark posted on their website says the following.

“Right now, in almost no market in this country, can a homebuilder build a house that is affordable for a first-time homebuyer,” National Association of Home Builders CEO Jerry Howard said on “Varney & Co.” Thursday. “We can’t do it. The costs that are on us make it impossible.” So, first, while Cavco’s quotation is close, it is NOT precise. Cavco’s version of NAHB CEO Howard’s remark omits the word “almost” Here is how Cavco posted it in their investor relations page 4 above. “…(in) no market in this country can a homebuilder build a house that is affordable for a first-time home buyer.” National Association of Home Builders CEO, Jerry Howard. Note that while Cavco cited the sources for 3 other remarks on that page (Pew, NPR, and Forbes), it failed to cite the source for NAHB CEO Howard’s remark. That said, the points that Cavco has made with that slide are important.

Next to “Why it matters” are these three remarks.

- Nationwide impact with approximately 6 million housing unit deficit

- Ownership helps prevent intergenerational poverty

- Shortage of affordable housing costs American economy $2T in lower wages and productivity

Once again, as with the Howard quote, those statements aren’t supported by the sources for those comments. That noted, there is support for those claims, as MHProNews previously noted in detail in the report linked below.

For those interested in ESG, those remarks are powerful. That said, Cavco’s Boor used ESG as a pivot point to make other remarks to Congress on July 14, 2023. Perhaps oddly, Cavco’s CEO Boor made distinctively different remarks to investors just a few weeks after his remarks to Congress.

7). Perhaps this next slide from Cavco’s 11.2023 investor presentation is where a question of materiality and the firm’s fiduciary duty to investors and stakeholders could come in to play (see preface and the introduction to Part II, above).

Note: to expand this image below to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

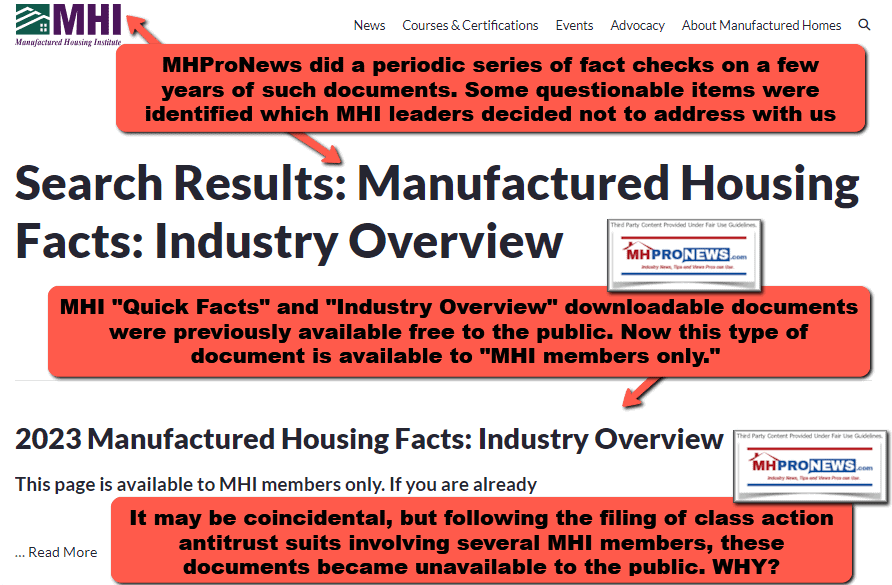

On the bottom left of page 5 (the MHProNews annotated screen capture above) is this statement. “* Source: Manufactured Housing Institute’s 2022 Manufactured Housing Facts: Industry Overview.” MHProNews has raised the topic several times that MHI’s recently revised website has made several changes beyond mere appearances. The case can be made that information previously made available by MHI to the public has been removed. What is interesting is that some of that removed information were the subjects of MHProNews fact checks. That reference from Cavco is to one of those removed (i.e.: now hidden, taken down, or perhaps members only) documents. This has occurred at about the same time as national class action lawsuits were filed against several prominent MHI members.

Keep in mind the information in linked in the opening paragraph of this article. In the recent past, Cavco has had years of legal woes.

For employees working for a firm that may have problematic business practices, the above and next reports are reminders that it can be beneficial to several for formal complaints, and/or news tips to media like ours that is willing to hold firms and organizations accountable for problematic actions/inactions. While the system may be problematic, it would be wrong to say that the system never works. It has worked in numbers of higher profile cases, such as the examples noted in the report and analysis linked below.

8) Cavco has made a big deal about encouraging the raising of concerns and complaints to management. Cavco, and perhaps several other MHI member firms, may have reason to hope and pray that their employees don’t blow the whistle on several aspects of their operations, especially in the light of the class action and other legal cases noted and linked from this report.

9) Back to the point raised in #7 above. Cavco cited an MHI document that was once publicly available, but now no longer is, according to the search of the MHI website shown below.

Note: to expand these images below to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

It isn’t just that document, but others that were once publicly available that have since been removed. Another example recently detected is the one shown below. For the possible significance, see the deeper dive on MHI linked here. But keep in mind that Cavco is a prominent MHI member. That MHI “priorities” document that was removed included the issue of zoning barriers.

10) While MHI is ironically pitching potential and new members on the notion that they should sign up (see report linked above) to get access to a “members only” tool that details zoning barriers in the U.S., Cavco Industries is telling investor that “Zoning restrictions are beginning to ease in response to affordability issues.” Seriously? Where is the evidence for that remark? While there may be a very limited number of possible examples for that which Cavco could point to, the fact that their own CEO – Bill Boor – made remarks to Congress asking for help with HUD’s failure to press zoning issues ought to be a red flag for a disconnect between what Boor told Congress, and what Cavco told investors previously and in recent remarks that questionably claim that “Zoning restrictions are beginning to ease in response to affordability issues.”

11) Put simply, Cavco can’t have it both ways. They can’t tell Congress that zoning barriers are a serious problem (they are, as a notable example, see the report linked here), and then tell investors that zoning barriers are easing. Perhaps more revealing is the point that Cavco and MHI leaders have apparently had face-to-face meetings with HUD Secretary Marcia Fudge, yet there is no known evidence that the topic of “enhanced preemption” (see Boor’s remarks shown above about preemption enforcement) has been raised face to face with Fudge or senior HUD leadership. Yet Fudge said in video recorded remarks to Congress that these issues (zoning barriers) will “perpetually” persist until these legal questions are solved.

12) But those points are conveniently ignored in MHI’s recent or several prior messages to members and on the MHI website. Industry professionals, perhaps especially management, are often busy. They may not think that they have the time to spend checking up on the how ethical their national association (i.e.: MHI) and or MHI affiliated state associations happen to be. That said, state associations (dubbed by MHI as state affiliates) and MHI’s own previously asserted history items are also among the ones seemingly missing from their revised website. MHI boldly claims in their new home page that they are: “Expanding Attainable Homeownership” at a time when the industry is in a documented 11 months of year-over-year declining production. MHI leaders have made statements under oath which arguably have not been supported by the evidence.

13) To illustrate and give evidence in support of several of these points, the following inquiry was put to Bing AI.

> “Is there any known evidence that Manufactured Housing Institute corporate or staff leaders have discussed the lack of enforcement of the enhanced preemption issue under the Manufactured Housing Improvement Act of 2000 with HUD Secretary Marcia Fudge?”

Learn more:

14) Once someone grasps the degree to which the ‘system is rigged’ in manufactured housing, and what the history of several higher profile MHI members are, a sobering “aha” moment may occur. On the one hand, Bill Boor made the remark to investors that the industry (i.e.: manufactured housing) had an opportunity to ‘catch up’ to conventional building. They are still making similar remarks to investors, when they say that millions of housing units are needed, and that manufactured housing can supply that need. That’s true enough, but the question remains: is it also paltering on the part of Cavco and MHI leaders? Are MHI and Cavco (among several other possible MHI members) posturing and paltering in order to get and keep investors, stakeholders, and members? The evidence-based case can be made that answers such questions with “yes.” And if that is true, then materially and legally problematic omissions and misstatements are possible, even likely.

15) To illustrate the concerns raised herein (e.g.: #14) the following was put to Bing AI.

> “Hypothetically speaking. Let’s presume that Manufactured Housing Institute connected corporate leaders, say board members, are implying or telling investors that zoning barriers are improving. But they fail to mention that several Manufactured Housing Institute members apparently do not want the “enhanced preemption” clause of the Manufactured Housing Improvement Act of 2000 enforced at this time. Their reasoning is that limiting or throttling growth can help insiders condolidate the industry. If that is not properly disclosed, is it a possibly material ommission that may violate the fidicuiary obligations of the Manufactured Housing Institute to their members who think that the association is working to mitigate those zoning issues? Similarly, if a publicly traded firm in investor presentations is making the argument that the company wants to grow to sell potentially much larger numbers of homes, but they too are insincerely pressing the preemption issue, are those possibly materially relevant and failures to fulfill a firm’s fiduciary duty to stockholders?”

Note that question doesn’t mention MHProNews, but 3 of the answers linked by Bing AI are on the MHProNews (ManufacturedHomeProNews.com) website.

15) It isn’t just investors that are potentially harmed by policies that limit the opportunities for home ownership. The homebuying public is harmed. The working and middle class are undermined. Employees are harmed through lower wages. Taxpayers are harmed because they are routinely compelled through government spending to fill the gap in programs that might to various degrees be sunsetted if the problems they aim to resolve were in fact fixed. In the respect, Cavco’s page 4 slide shown above helps make several of those points. Ironically, Cavco itself has a poor score with its numbers of its own employees, if the information from Indeed – which are based on actual employee remarks – are relied upon.

So, even this relatively focused report reveals several possible issues that public officials, investors, and other advocates could consider as evidence for an investigation of Cavco, and perhaps others in the Manufactured Housing Institute (MHI) orbit. Why MHI? Why not the Manufactured Housing Association for Regulatory Reform (MHARR) too? Because as the report linked here indicated, Bing AI said what MHProNews previously observed. Namely, that while MHI and several key MHI members has several evidence-based reasons for investigation, there are no known similar evidence-based allegations against MHARR.

Programming Notices: MHProNews plans to unpack the related Cavco quarterly earnings call in the near term. Exploring other corporations remarks and claims are also part of our plan for MHProNews reports and analysis the near term as well.

Summing Up

For a company that has a recent history of significant exposure to governmental as well as civil litigation on behalf of shareholders, the items shown in this report ought to be cautionary flags, if not red flags with respect to Cavco Industries. In as much as Cavco has held key roles at MHI in recent years, these are also reflections on MHI as well as Cavco.

Elements of this report have focused on questionable remarks made about zoning barriers. That’s hardly the only issue involving Cavco and MHI. To illustrate that point, consider the reports linked below.

On 12.11.2022, MHProNews indicated that manufactured housing had become a ‘target rich environment’ for attorneys and public officials sincerely interested in the interests of the public, investors, and others.

In less than a year after that report by MHProNews, multiple class action lawsuits have been filed against MHI member companies. In the manufactured home industry-expert view of this writer for MHProNews, regrettably, the manufactured housing industry remains a target rich environment for still more regulatory and legal action.

Buckle up and stay tuned for more “Intelligence for Your MHLife” © from the biggest and best source for “Industry News, Tips, and Views Pros Can Use” © where “We Provide, You Decide.” © ##

Part III – is our Daily Business News on MHProNews stock market recap which features our business-daily at-a-glance update of over 2 dozen manufactured housing industry stocks.

This segment of the Daily Business News on MHProNews is the recap of yesterday evening’s market report, so that investors can see at glance the type of topics may have influenced other investors. Thus, our format includes our signature left (CNN Business) and right (Newsmax) ‘market moving’ headlines.

The macro market move graphics below provide context and comparisons for those invested in or tracking manufactured housing connected equities. Meaning, you can see ‘at a glance’ how manufactured housing connected firms do compared to other segments of the broader equities market.

In minutes a day readers can get a good sense of significant or major events while keeping up with the trends that are impacting manufactured housing connected investing.

Reminder: several of the graphics on MHProNews can be opened into a larger size. For instance: click the image and follow the prompts in your browser or device to OPEN In a New Window. Then, in several browsers/devices you can click the image and increase the size. Use the ‘x out’ (close window) escape or back key to return.

Headlines from left-of-center CNN Business – from the evening of 11.27.2023

- Volkswagen says its core VW brand is ‘no longer competitive’ financially

- Americans are set to spend a record $12 billion online shopping today

- Elon Musk visits destroyed kibbutz and meets Netanyahu in wake of antisemitic post

- Google Apps like Gmail, Maps, YouTube, Drive, and Hangouts are seen on a phone screen.

- Google to begin deleting inactive accounts this week

- New home sales fell last month as mortgage rates hit 2023 high

- How AI could power the climate breakthrough the world needs

- Jack Ma is betting on a new food business in China

- Signage atop the Zhongrong International Trust Co. offices in Beijing, China, on Monday, August 21, 2023.

- China launches criminal probe into ‘insolvent’ shadow bank

- Meta collected children’s data from Instagram accounts, unsealed court document alleges

- American spending has kept the economy going since the pandemic. It may finally be stopping, in charts

- Honda recalls more than 300K Accords, HR-Vs over seat belt issues

- Energized shoppers break one-day holiday sales record

- Why doesn’t the US have more passenger trains?

- Why Small Business Saturday is a hit with holiday shoppers

- Empty Bed Bath & Beyond stores are hot real estate. Here’s who’s moving in

- The tug-of-war is on between retailers wary of throw-away prices and deal-hungry Black Friday shoppers

- The surprising history of America’s biggest holiday shopping blitz

- Best Buy’s simple strategy for beating shoplifting: More workers in stores

- ‘This is insane.’ Swedish workers are getting under Elon Musk’s skin

- Billionaire Foxconn founder drops out of Taiwan’s presidential race

- Nissan leads $2.5 billion investment to build two more EVs in UK

- ‘Moment of truth’ for oil industry: Deepen the climate crisis or help fix it

Note: to expand this image below to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

Headlines from right-of-center Newsmax 11.27.2023

- Israel Says 11 More Hostages Free With Truce Set for 2-Day Extension

- Hostage, 84, Released by Hamas in ‘Fight for Her Life’

- Released Palestinian Prisoner Investigated for Inciting Terror

- Qatar: 2-Day Truce Extension; 11 More Hostages Freed on 4th Day

- US, Allies Form Task Force to Defund Hamas

- Iraq Sees Risk of Regional Conflict If Gaza War Resumes

- Arab States, EU Push for 2-State Solution

- Hostage Tells Story of Escaping Hamas Terrorists

- IDF Soldier Freed From Hamas in Gaza Raid Speaks Out

- US Navy Seizes Attackers Who Held Israeli Tanker

- Netanyahu Visits Gaza Strip, Tours Terror Tunnel

- Israel’s Gantz Threatens to Quit Unity Govt Over War Budget

- Musk: Israel ‘Has No Choice’ but to End Hamas’ Reign

- Newsmax TV

- Tenney: Northern Border ‘Exposed’

- Napolitano: Jan. 6 Trump Verdict Likely Before Election | video

- Tal Heinrich: ‘No Equivalency’ in Israel-Hamas Swaps | video

- Chad Wolf: ‘Pretty Clear’ Why China Migrants Come | video

- Holt: Cease-Fire Is Hamas Plot to Stay Alive | video

- Blaine Holt: Israel Must Not Fold to Pressure | video

- Fred Fleitz: Hostage Release Not a Prisoner Swap | video

- Greg Murphy: Get Hostages, Eliminate Hamas | video

- Newsfront

- Trump: I ‘Sarcastically’ Mix Up Biden, Obama Names

- Former President Donald Trump said he intentionally has used former President Barack Obama’s name instead of President Joe Biden’s while making some sarcastic comments…. [Full Story]

- Wall Street Ends Lower Amid Cyber Monday Madness

- U.S. stocks edged lower Monday, with investors taking a [Full Story]

- Report: DEI Push Slows in US Companies

- Diversity, equity and inclusion (DEI) efforts by U.S. companies are [Full Story]

- US Defends ‘Robust’ Climate Summit Team Despite Biden Snub

- The White House said on Monday a “robust” U.S. delegation would [Full Story]

- Fmr CNN’s Zucker Plans ‘Center-Right’ Telegraph Against NY Times, Wash Post

- Former CNN President Jeff Zucker is making his pitch for U.K.’s media [Full Story]

- Federal Judge Rules vs Meta in FTC Privacy Fight

- Meta’s Facebook lost the latest round of a court battle over privacy [Full Story]

- Narrowed GOP Primary Field ‘Directly’ Benefits Trump

- The number of Republican presidential hopefuls continues to dwindle [Full Story] | Platinum Article

- Related

- Trump: I ‘Sarcastically’ Mix Up Biden, Obama Names

- Trump Exec: Sweeping Financial Reports No Longer Prepared

- Trump Hints at Expanded Role for Military Within US

- Trump’s Vow to Crack Down on Immigration Faces Backlash

- RNC’s McDaniel Downplays Party’s Donor Concerns

- Drones Provide ‘True Enhancement’ to Law Enforcement

- Drones Provide ‘True Enhancement’ to Law Enforcement

- As police departments continue to struggle with recruitment and [Full Story] | Platinum Article

- Related

- NYPD Exodus Continues to Vex Staffing, Policing |video

- Iran Adds Sophisticated Warship to Caspian Fleet

- Iran’s navy on Monday added a destroyer capable of launching cruise [Full Story]

- Related

- Iraq Sees Risk of Regional Conflict If Gaza War Resumes

- US Navy Seizes Attackers Who Held Israel-Linked Tanker

- Tom Cotton Calls for ‘Massive Retaliation’ on Iran |video

- Turkey Aligns Firmly With Iran Against Israel

- Few Remain in Ukraine’s War-Torn Avdiivka Region

- On a narrow asphalt strip scarcely visible late at night, a Ukrainian [Full Story]

- Related

- Republicans Move to Link Border Security to Ukraine Aid

- Top EU Official Impressed With Ukraine’s Effort to Fight Corruption

- Ukraine Shipping More Grain Through Black Sea Despite Risks

- Ukraine, Balkans Top Blinken’s Agenda for Brussels NATO Meeting

- Crimean Treasures Return to Kyiv After Years of Legal Battles

- Mike Turner: Aid for Ukraine Unlikely This Year

- Qatar Also Working to Return Ukrainian Children

- Pope Francis Getting Antibiotics Via IV for Lung Illness

- Pope Francis is receiving antibiotics intravenously to treat a lung [Full Story] | video

- Related

- Vatican: Can’t Ordain Women, Discuss Homosexuality

- Ailing Pope Has Aide Read His Sunday Message in Broadcast

- Senators Seek Answers on US Readiness in Space Race

- Two senators sent a letterto the Federal Aviation Administration and [Full Story]

- 5 Key Races Make Senate Landscape Dicey for Dems

- With Sen. Joe Manchin, D-W.Va., retiring, the 2024 Senate landscape [Full Story]

- NKorea Girds Border Amid Rising Tensions With South

- North Korea is restoring front-line guard posts it had dismantled [Full Story]

- Related

- UN: North Korean Rockets Threaten Civilian Planes, Ships

- Disney Admits Its Left-Wing Politics Hurt Shareholders

- In new SEC filings, Disney is now admitting it has been slapped by [Full Story]

- Jimmy Carter Expected to Attend Late Wife’s Memorial

- Former President Jimmy Carter, 99, is expected to attend the memorial [Full Story]

- Related

- Rosalynn Carter to Lie in Repose in Georgia

- Joni Ernst to Biden: Finish the Border Wall

- Joni Ernst, R-Iowa, wrote in an opinion piece on Monday that [Full Story]

- Related

- Chad Wolf to Newsmax: ‘Pretty Clear’ Why China Migrants Come |video

- Dem Gov. Evers Uses Warren Spahn Email Alias

- Wisconsin Gov. Tony Evers has been using an alternative state email [Full Story]

- Biden to Skip COP Climate Meeting in Dubai: US Official

- S. President Joe Biden will not attend a gathering of world leaders [Full Story]

- Related

- Biden to Invoke Measure to Boost Medical Supplies

- Biden to Convene New Supply Chain Council

- Ronny Jackson: Biden’s Decline ‘Happening Quickly’

- Already 150,000 Joined Newsmax+ – Did You?

- Move over Netflix, left-wing Disney+ and Hulu, there is a new sheriff [Full Story]

- Childhood Inspires Jill Biden’s WH Holiday Decor

- Ninety-eight Christmas trees, more than 142,000 twinkling lights and [Full Story]

- Related

- Museum’s Tree Display Includes Satanic Worship Tree |video

- Shoppers Nab Early ‘Cyber Monday’ Deals

- As the year’s biggest U.S. online shopping day gets underway Monday, [Full Story]

- Suspect Nabbed in Vermont Shooting of 3 With Palestinian Descent

- A man pleaded not guilty to attempted murder Monday in connection [Full Story]

- Bidenomics Squeezes Americans’ Budgets by 20 Percent

- The cost-of-living squeeze is robbing Americans of 20% of their [Full Story]

- Pentagon: Ship Hijackers Likely Somalis, Not Houthis

- A group of five militants who seized another commercial ship near [Full Story]

- US, Allies Form Task Force Aimed at De-funding Hamas

- The U.S. said on Monday that after Hamas’ assault on Israel last [Full Story]

- Deal-Hunters Fuel $12B Cyber Monday Shopping Spree

- After a busy holiday shopping weekend, discount seekers are expected [Full Story]

- Today in History: Harvey Milk, George Moscone Shot Dead

- On Nov. 27, 1978, San Francisco Mayor George Moscone and City [Full Story]

- Portland Teachers Reach Tentative Deal to End Strike

- The union representing public school teachers in Portland, Oregon, [Full Story]

- Gerard Gibert, the Rush Limbaugh of Mississippi?

- When most are contemplating retirement, former high-tech entrepreneur [Full Story]

- Biden to Convene New Supply Chain Council

- President Joe Biden Monday will convene the first meeting of his [Full Story]

- Finance

- Federal Judge Rules vs Meta in FTC Privacy Fight

- Meta’s Facebook lost the latest round of a court battle over privacy with the U.S. Federal Trade Commission on Monday after a federal judge ruled the regulator can seek to reduce the amount of money the social media company makes from users under 18…. [Full Story]

- President Biden’s Absence From Climate Meeting Sparks Debate and Concerns

- Judge Orders Ex-Binance CEO Zhao to Remain in US

- Are The Big 5 Asset Managers Liars?

- Major Social Security Payment Warning Not to Be Ignored as 2023 Ends

- More Finance

- Health

- ADHD Meds Linked to Increased Heart Disease Risk

- Medications used to treat attention deficit hyperactivity disorder (ADHD) are associated with long-term risk of cardiovascular disease, according to a new study published in JAMA Psychiatry. Swedish researchers found that people taking ADHD medications had a higher risk of…… [Full Story]

- Drones Deliver Defibrillators Faster Than Ambulances

- More Vitamin D May Be Needed for Heart Health

- Stronger Thighs May Reduce Need for Knee Replacement

- Scans Show Brain Changes in People With Long COVID

Note: to expand this image below to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

-

-

- NOTE 1: Chart above of manufactured housing connected equities includes the Canadian stock, ECN, which purchased Triad Financial Services, a manufactured home industry finance lender.

- NOTE 2: Drew changed its name and trading symbol at the end of 2016 to Lippert (LCII).

- NOTE 3: Deer Valley was largely taken private, say company insiders in a message to MHProNews on 12.15.2020, but there are still some outstanding shares of the stock from the days when it was a publicly traded firm. Thus, there is still periodic activity on DVLY.

- Note 4: some recent or related reports to the REITs, stocks, and other equities named above follow in the reports linked below.

-

2023 …Berkshire Hathaway is the parent company to Clayton Homes, 21st Mortgage, Vanderbilt Mortgage and other factory-built housing industry suppliers.

· LCI Industries, Patrick, UFPI, and LP each are suppliers to the manufactured housing industry, among others.

· AMG, CG, and TAVFX have investments in manufactured housing related businesses. For insights from third-parties and clients about our publisher, click here.

2022 was a tough year for many stocks. Unfortunately, that pattern held true for manufactured home industry (MHVille) connected stocks too. See the facts, linked above.

====================================

Disclosure. MHProNews holds no positions in the stocks in this report.

· For expert manufactured housing business development or other manufactured housing professional services, click here.

· To sign up in seconds for our industry leading emailed headline news updates, click here.

- Note 1: MHVille means manufactured housing industry, MHVille also means artificially smaller manufactured housing (MH) industry,

- Note 2: Manufactured housing, building, factories, retail, dealers, manufactured home, communities, passive mobile home park investing, suppliers, brokers, finance, financial services, macro-markets, manufactured housing stocks, Manufactured Home Communities Real Estate Investment Trusts, MHC REITs.

- Note 3:

APO, Apollo Global Management, BAM, Brookfield Asset Management, BLK, BlackRock, BRK-A, Berkshire Hathaway, BX, Blackstone, CDPYF, Canadian Apartment Properties Real Estate Investment Trust, CIGI, Colliers International Group Inc, CG, The Carlyle Group, CSGP, CoStar Group, CVCO, Cavco Industries, ECNCF, ECN Capital Group, ELS, Equity LifeStyle Properties, FGF, FG Financial Group, FG Communities, KEY, KeyCorp, KMMPF, Killam Apartment REITs, LCII, LCI Industries, LEGH, Legacy Housing, LPX, Louisiana Pacific Corporation, MHC-UN.TO, Flagship Communities Real Estate Investment Trust (REIT), MHPC, Manufactured Housing Properties, MMI, Marcus and Millichap, NOBH, Nobility Homes, PATK, Patrick Industries, SKY, Skyline Champion, SUI, Sun Communities, UMH, UMH Properties, UFPI, UFP Industries.

That’s a wrap on this installment of “News Through the Lens of Manufactured Homes and Factory-Built Housing” © where “We Provide, You Decide.” © (Affordable housing, manufactured homes, stock, investing, data, metrics, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.) (See Related Reports linked herein. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHProNews.

Tony earned a journalism scholarship along with numerous awards in history. There have been several awards, honors and numerous public recognitions for his achievements in manufactured housing. For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. Kovach is a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com, which is ranked as the runaway most read trade media in modern manufactured housing history. This article reflects the LLC’s and/or the writer’s editorial views and may or may not reflect the views of sponsors or supporters.