“Legacy’s consumer finance business closed more loans in October of 2023 than any other month in the company’s history,” said Duncan Bates, President and CEO of Legacy Housing. Chief Financial Officer (CFO) Jeff Fiedelman said: “Legacy delivered an 18.6% return on shareholders’ equity over the last 12 months.” As MHProNews reported earlier this week in the tee up to this report, Yahoo Finance indicated that the LEGH stock is “undervalued” – so in the eyes of numbers, it is worth more than it is trading for and the future outlook for Legacy, per analysts, is positive too. But if that is good, this comment from CEO Bates may make the co-founders Kenneth “Kenny” Shipley and Curtis “Curt” Hodgson glow: “Legacy was started with $700,000, and we have grown that equity to $429.5 million in 18 years, make it, save it, invest it again and again.”

EF Hutton analyst Tim Moore, CFA said “congratulations on the continued good operational execution” to Legacy’s CEO Duncan Bates, “it’s vastly improved since you took over Duncan.”

As per our custom in recent years, what follows in Part I – in this case from Yahoo Finance and Insider Monkey Transcripts – the bracketed items are edits of apparent typos by MHProNews. Highlighting is by MHProNews as part of our analysis of the information that follows in Part II.

Insights relative to independent retailers will be part of the focus in Part II, based in part on remarks by Bates but also on prior exclusive reports and analyses by MHProNews. Another item to be explored is this remark by CEO Bates: “Look, the biggest headwind of this — in this entire industry is where to put these homes.

https://finance.yahoo.com/news/legacy-housing-corporation-nasdaq-legh-181322669.html

Legacy Housing Corporation (NASDAQ:LEGH) Q3 2023 Earnings Call Transcript

Insider Monkey Transcripts

November 11, 2023·9 min read

Legacy Housing Corporation (NASDAQ:LEGH) Q3 2023 Earnings Call Transcript November 10, 2023

Operator: Good day, and thank you for standing by. Welcome to the Legacy Housing Corporation Third Quarter 2023 Earnings Call. At this time, all participants are on a listen-only mode. After the speakers’ presentation, there will be a question-and-answer session. [Operator Instructions] Please be advised, today’s conference is being recorded. I would now like to turn the conference over to your speaker today, Duncan Bates. Please go ahead.

Duncan Bates: Good morning. This is Duncan Bates, Legacy’s President and CEO. Thanks for joining our third quarter 2023 conference call. Max Africk, Legacy’s General Counsel, who will read the safe harbor disclosure before getting started. Max?

Max Africk: Thanks, Duncan. Before we begin, may I remind our listeners that management’s prepared remarks today will contain forward-looking statements, which are subject to risks and uncertainties, and management may make additional forward-looking statements in response to your questions. Therefore, the company claims the protection of the safe harbor for forward-looking statements as contained in the Private Securities Litigation Reform Act of 1995. Actual results may differ from management’s current expectations. We, therefore, refer you to a more detailed discussion of the risks and uncertainties in the annual report filed with the Securities and Exchange Commission. In addition, any projections as to the company’s future performance represent management’s estimates as of today’s call. Legacy Housing assumes no obligation to update these projections in the future unless otherwise required by applicable law.

Duncan Bates: Thanks, Max. I’m joined today by Jeff Fiedelman, Legacy’s Chief Financial Officer. Jeff will discuss our third quarter performance, then I will provide additional corporate updates and open the call for Q&A. Jeff?

Jeff Fiedelman: Thanks, Duncan. Product sales decreased $11.7 million or 24% during the three months ended September 30, 2023, as compared to the same period in 2022. This decrease was driven by an industry-wide decrease in unit volumes, a decrease in net revenue per unit and a decrease in the conversion of certain independent dealer consignment arrangements to financing arrangements and other market factors. For the three months ended September 30, 2023, our net revenue per unit sold decreased 1.6% to $63,600. Consumer and MHP loans interest income increased to $8.8 million or 25.7% during the three months ended September 30, 2023, as compared to the same period in 2022. This increase was driven by increased balances in the MHP and consumer loan portfolio.

Between September 30, 2023 and September 30, 2022, our MHP note portfolio increased by $47.8 million, and our consumer loan portfolio increased by $16.8 million. This is net of principal payments and loan loss allowances. This does not include floor plan financing or development loans. Other revenue primarily consists of contract deposit forfeitures, dealer finance fees and commercial lease rents, and increased to $4.1 million or 150.8% in the third quarter of 2023 compared to the third quarter of 2022. This increase was primarily due to an increase in forfeited deposits and an increase in floor plan financing fees. The cost of product sales decreased $8.7 million or 25.9% during the three months ended September 30, 2023, as compared to the same period in 2022.

The decrease in costs is primarily related to the decrease in units sold. Product gross margin was 32.9% for the third quarter of 2023, up from 31.9% for the third quarter of 2022. Selling, general and administrative expenses decreased 9.2% during the three months ended September 30, 2023, as compared to the same period in 2022. This decrease was primarily due to a decrease in warranty costs and a decrease in other miscellaneous costs, partially offset by increased legal expenses and an increase in loan loss provision. Net income increased 9.2% to $16.1 million in the third quarter of 2023 compared to the third quarter of 2022. Net income margin was 32.2% for the third quarter of 2023, up from 25.7% for the third quarter of 2022. We ended the quarter with $0.5 million in cash and $13.0 million drawn on our line of credit.

On July 28, 2023, we closed a new revolving credit facility with Prosperity Bank. The facility is for $50 million with a $25 million accordion feature. It is secured by our consumer loan portfolio. Legacy delivered an 18.6% return on shareholders’ equity over the last 12 months. At the end of the third quarter of 2023, Legacy’s book value per basic share outstanding was $17.61, an increase of 18.7% from the same period in 2022.

An aerial view of a manufactured home community, with the many homes in a grid.

Duncan Bates: Thanks, Jeff. We’re happy to have you on the team. Let’s start with the market, then I’ll discuss Legacy’s financial performance and provide an update on strategic initiatives. According to Manufactured Housing Institute data, industry home shipments through September of 2023 are down 25.7% year-to-date. However, housing affordability in the U.S. continues to deteriorate and large numbers of potential homebuyers are priced out of the traditional housing market. We held our 2023 Fall Show in Fort Worth in early October. As I mentioned in the press release, the 2023 show was one of the most successful sales events in the company’s history. The show orders extend backlogs at our Texas facilities well into the first quarter of 2024 at a higher production rate than the third quarter of 2023.

Both dealer and par[k] customers ordered homes at the Fall Show. The retail or dealer side of our business is showing signs of life. Foot traffic is up and dealers are selling homes. Although it varies by geography, we believe that most of the destocking issues from early 2023 are largely behind us. The reorder rate is lower than we would like, but inventory carrying costs are also higher. One important data point on the dealer side. Legacy’s consumer finance business closed more loans in October of 2023 than any other month in the company’s history. On the community or park side of the business, sales to community owners and developers remain stable. Like other manufacturers, we have battled delayed shipments due to setup-related issues, discriminatory zoning practices and high interest rates are headwinds for new developments.

We secured a few large park orders with deliveries extending through mid-2024. I’m proud of our team’s performance to date in 2023. Despite a 25.7% decline in industry-wide shipments through September, Legacy’s net income is only down 1.5% year-to-date through the third quarter. We are driving sales and managing expenses effectively. Interest income from 12 months of reinvesting our profits back into the loan portfolios drove a meaningful portion of the year-to-date profits as product sales declined in 2023. At September 30, 2023, over 99.3% of MHP notes and 98.5% of our consumer loans are current or less than 30 days without payment. We monitor these numbers closely and are confident in the strength of our loan portfolios. I received positive feedback from the last call about discussing projects that the team is working on.

Here’s where I’m focused. Hiring. We made a big — we’re making a big push to hire young, hungry individuals that are committed to a career at Legacy. Our team is lean, aging and possesses a tremendous amount of industry knowledge. Our goal is to create a path for motivated individuals to harness this information in advance within the company.

Number two, working capital. Our working capital is too high. We have too much raw material and finished goods inventory. We are working to reduce inventory and free up capital that can be reinvested back into the business.

Third, Georgia sales. The Texas plants are in good shape from a sales standpoint. Our team in Georgia has done a great job with product quality and we are now building the highest quality homes that have come out of the Eatonton plant.

Now we need to accelerate sales. Most of the sales team is new and learning. Kenny and I have been heavily involved and we are starting to see results. We need to keep the hammer down though. Number four, workforce housing. We have 40-plus floor plans and have not historically made a push in this space. We continue to bid on large projects with well-known disaster relief service providers. Legacy has the balance sheet to hold and lease large amounts of inventory. It’s too early to discuss specific projects and numbers, but I continue to believe the workforce housing is a huge opportunity for Legacy.

Number five, land development. We hired a dedicated team to prioritize and accelerate land development. Completing Phase 1 of Del Valle or Bastrop County outside of Austin is our top priority.

Water and electricity are in, road construction and construction of the water treatment plant began in November. Delaying construction at several properties may have helped us. For example, some properties were in very rural areas when purchased. Now five-plus years later, there are plans to run city sewer and other services that will increase value and provide flexibility. We continue to evaluate ways to maximize the value of these projects for our shareholders. In addition to these internal projects, we are consistently evaluating inorganic growth opportunities. The new bank line gives us the flexibility to pursue these opportunities if they hit our return threshold. One final thought on valuation. We are growing book value or shareholders’ equity at about 19% a year.

Legacy was started with $700,000, and we have grown that equity to $429.5 million in 18 years, make it, save it, invest it again and again. Our book value primarily consists of finance notes at par with the reserve, inventory at cost and land developments at cost. Our facilities and equipment are mostly depreciated. We believe that our book value is conservatively stated and is near the company’s liquidation value. We publish our book value per share each quarter. As of September 30, 2023, our book value per share was $17.61. That number is a month-and-a-half stale and our stock is trading in the $19 range. It’s not much of a premium. If the stock trades at or below book value per share, we will use the full extent of our balance sheet to repurchase shares.

I believe that we can continue growing shareholders’ equity at 18% to 19% a year in this high interest rate environment and that our share price will begin to reflect this. If you do the math, the numbers get large quickly. Any strategic moves are icing on the cake. Operator, this concludes our prepared remarks. Please begin the Q&A.

Operator: Thank you. [Operator Instructions] Our first question comes from Mark Smith with Lake Street. Your line is open.

Mark Smith: Hi, guys. Duncan, first, I wanted to dig into gross profit margin just a little bit more, really solid execution there. Can you talk about any additional drivers there, maybe what you saw? Has inflationary pressures gone down? What you’re looking at for labor? Any insights there would be great.

Duncan Bates: Yes, sure. Hey, Mark. So, a couple of thoughts for you. Obviously, volume was down pretty significantly in the third quarter. So, managing expenses is extremely important. We’ve been able to hold price even at lower volumes and material prices have come down. Labor and overhead, on the other side of things, have continued to go up. And they’re not accelerating at a quick rate, but it certainly has had an impact on gross margin. I would expect as we ramp up production and continue to manage our costs, that we can — we’re trying to hold these margins where they are, but obviously, managing inventory as well as labor.

Mark Smith: Okay. And then, solid performance on the consumer finance loan business. Did you guys use rate there at all to kind of help drive that? It looks like maybe we saw rates down a little bit. Any discussion around that?

Duncan Bates: Yes. We’re — I think our rates across the loan portfolios have been pretty attractive and certainly helped us drive sales. We are taking rates up a little bit on the consumer loan portfolio, but we’ve not — those won’t be included in the third quarter numbers. So, I think we’ve got an opportunity to pick rates up a little bit here to get back in line with the market.

Mark Smith: Okay. And then any — you guys have done a good job kind of managing charge-offs and any issues within the portfolio. Any changes in kind of your underwriting policies? Or is everything kind of stayed the same there?

Duncan Bates: They’ve stayed the same. I feel pretty good about our underwriting processes. We have added additional collections personnel to the team just in the event that you did start to see some cracks in the loan portfolios. But we’re keeping an eye on it, and we make a lot of calls. We monitor it closely. And we’ve continued to perform with managing those portfolios.

Mark Smith: Okay, great. Thank you.

Duncan Bates: Thanks, Mark.

Operator: One moment for our next question. Our next question comes from Alex Rygiel with B. Riley Securities. Your line is open.

Alex Rygiel: Thank you. Nice quarter, Duncan and team.

Duncan Bates: Hey, Alex.

Alex Rygiel: Nice quarter there. A couple of quick questions here. First, you’ve been holding your average selling price at a nice level here. Any reason for that to change sort of over the intermediate term?

Duncan Bates: No. We plan to continue to hold it. I think the one thing that has changed. Remember last quarter, we saw a pretty significant drop in average selling price quarter-over-quarter. I think that’s stabilized and it stabilized toward kind of smaller, less optioned homes. But I feel pretty good about where it is now. I don’t think we’ll see another major drop. But as far as pricing goes, I mean, we’re now ramping up production at both of the Texas plants. We’ve got a nice backlog well into the first quarter. And so, I don’t plan to see any price degradation into 2024.

Alex Rygiel: And then, you’ve been talking about larger kind of commercial customer orders, and that’s super exciting. Kind of two questions. I suspect it’s a little bit different of a product, but can you talk about that as it relates to average selling price and margin — kind of at the end of the day, the margin on that product? And is there any risk that it’s a different margin and creates a headwind?

Duncan Bates: Yes. So, we’re still in the early stages of this. And all of this came about by obviously, orders were pretty slow through the year, and Kenny and I hit the road and have been meeting with as many people as we can to sell all the product that we can. And we’ve actually — we’ve got — we build this product already, Alex. So — but we’re typically selling it to dealers in South Texas and in West Texas who have relationships with mainly oilfield services companies to house their workers. And so for us, it’s always been four homes here, 10 homes there, and never a focus from a direct sales standpoint. But as we dug in, I mean, there’s a lot of these projects. And we’re primarily competing against a different product.

It’s skid mounted metal product. It’s more expensive to manufacturers. So, I think from a price standpoint, we’re pretty competitive. The margins on that product look similar to our other products. I mean it’s just — it’s essentially large single wides with individual studio-type apartments with or without kitchenettes and all with bathrooms. And so, it’s something that we’re — we have experienced building. It’s not built to a different code or anything like that, that would significantly increase the price. But really, the interesting thing to us is a lot of this product is leased. And from what we can tell, the lease terms are pretty attractive on larger products. And so, it’s still — it’s a little early. I want to get contracts signed on a couple of things before we talk about it.

But I think there is a large opportunity, and I think it does help diversify the business as well as potentially growing the recurring revenue side of our business.

Alex Rygiel: Helpful. And then lastly, as it relates to community development, obviously, Del Valle is your most attractive kind of near term. Can you help us to understand when homes might get delivered to that site? And then, as it relates to other real estate that you own, any opportunities to sell these land assets and redeploy that capital into a share buyback?

Duncan Bates: Yes. Well, I’m putting them in three buckets. I think that there is a bucket for — that makes sense to sell. There are some properties that are just raw land where we haven’t made a lot of progress, and they’re smaller, may be not suited for a development or there’s some reason why they’re cost prohibitive. So I think on those, we can sell them when we feel like the market is right and make a nice return. There’s a second bucket, and I mentioned this on the call, where — since these projects have taken a long time, there have been developments. And so, we’ve got a situation where we’re seeing the area that this was in grow pretty significantly and their city sewer and water coming in the near term. And so, I think that, that bucket are — we’ll have to look at hard on what’s the best use of these projects.

Could be MH, could be single-family, but we want to maximize the value. And so, that’s bucket number two.

And then bucket number three is Del Valle and Horseshoe Bay and some of the other projects that are further along. And I think we’ve got to accelerate those to create value. We’ve now got a full-time team working on these projects. And I still — they’re newer, they’re getting up to speed on what’s been done historically and what needs to happen. I’m hesitant to give you a timeline for Del Valle because we’ve shattered it so many times in the past. But I think by year-end, as we start to get the roads in and the water treatment plant is being built, I think next call, I’ll have a really good idea of when homes actually start getting placed on those lots.

Alex Rygiel: Very helpful. Thank you very much.

Duncan Bates: Yes, thanks, Alex.

Operator: One moment for our next question. Our next question comes from Tim Moore with EF Hutton. Your line is open.

Tim Moore: Thanks, and congratulations on the continued good operational execution.

Duncan Bates: Thanks, Tim.

Tim Moore: Yes, it’s vastly improved since you took over Duncan. I just want to kind of follow up on a thread that’s probably all the investors’ minds. I mean your gross margin has done impressively, if not surprisingly well, the past three quarters despite the industry volumes downturn and even the minor ASP drop in the spring for the industry. So, just for the September quarter, you just reported any way, Duncan or Jeff to maybe parse out how much of that gross margin expansion in the quarter came from maybe cost deflation versus any benefit you might have had from some conversion of floor financing?

Duncan Bates: Yes, there’s no floor financing in this quarter. And so really, I’d say the majority of it is just from better execution on the purchasing side. And I think we still have a ways to go. I think that vendors are obviously reluctant to give price decreases unless you really push for them. And so, the majority of that margin expansion came from purchasing. But labor has continued to go up. And I think the market has softened a little bit, and it’s not accelerating like it was through COVID. But that’s something that we’re certainly keeping a close eye on is our — in our labor cost per square foot produced, and we track it pretty closely. But I’d say over the last five years, you see a continued increase in your labor cost.

And as we talk about ramping up production and hiring people, we’re certainly paying higher wages than we did four, five years ago. So, the goal is to continue to push on purchasing and add labor to ramp up production in an organized way, instead of just you pay a bunch of labors, a lot of money to stand around.

Tim Moore: That makes sense. I mean, it really is very impressive what you’ve done with the gross margin. So, Duncan, maybe you mentioned in your prepared remarks that Legacy close[d] more loans in October than any other month in Legacy’s history, the consumer loan front. Can you maybe share with us just the cadence — the monthly cadence during September quarter? In other words, was it incrementally better every month with the volume and the orders from July through September? Just trying to get a sense, maybe if you’re kind of seeing a bottom.

Duncan Bates: Yes. I mean, I feel like internal sentiment from a sales standpoint was the lowest I’ve seen in the third quarter. I think we’re in a much better place now. And I think that the success of the Fall Show was a big step in the right direction. That was something that I was pretty concerned about. And we sold a lot of homes, and that’s great. How can I answer your question better, sorry, Tim?

Tim Moore: No. I’m just trying to think now that you — if you kind of parse out that amazing show you just had, demand and orders, I mean, do you kind of feel like the floor is in for the industry maybe on volume and consumer sentiment?

Duncan Bates: Yes. I think volumes — we’re ramping up volume. Sales are looking good in Texas. And back to your question, I lost my train of thought, on the lending portfolios, we haven’t changed anything. I think the increase in applications and actually closing loans speak to a little bit of a pickup on the dealer side of the business. These loans don’t close overnight. There’s a whole underwriting process associated with them. So, it’s not perfectly linear. But we had — we saw originations this fall or applications reaching pretty good numbers, and Brandon and his team that run that business for us just did a good job of execution in October, and we plan to keep it going.

Tim Moore: That’s great. I remember meeting Brandon a year ago. And my last question is just regarding the CFO role change. Maybe can Jeff comment on maybe what he brings to enhance Legacy Housing? I read about his accounting background and his finance experience. But maybe just give us a shot to do a little commercial on what he bring?

Duncan Bates: Yes, sure. I’ll turn it over to Jeff, but I’m happy to have him onboard.

Jeff Fiedelman: Thanks, Tim. Thanks for asking the question. I’ve got a pretty diverse background, good operational background, especially in manufacturing, and really good experience helping businesses grow from one stage to the next in terms of process and operations and scale. And I’ve had the benefit of getting exposed to Legacy a couple of years ago and learning the business a little in a consulting role. And so, coming in, it’s been — you always have that luxury of knowing the business pretty well before you come into something new. But it’s a good team here, and I feel like I bring good solid experience across the board from an operations perspective, from a finance — corporate finance perspective, and on the accounting side and getting through some of the issues that the company has had historically.

Tim Moore: Great. Those are helpful insights. Thanks for sharing, Jeff. And Duncan, thanks for answering my questions.

Duncan Bates: Yes, thanks, Tim.

Operator: One moment for our next question. Our next question comes from Jay McCanless with Wedbush. Your line is open.

Jay McCanless: Hey, good morning, guys. Welcome aboard, Jeff. Duncan, could you maybe walk us through — I mean it sounds like the show went really well, but what was the feedback from the dealers? Just a couple or three maybe high points you could give us? And I mean sounds like with the order rate, it sounds like they’re getting more bullish as we think about the spring, but anything that stood out from your talks with the independents?

Duncan Bates: Yes. Jay, 2023 was a pretty hard year for the independent dealers. I mean, you come off of just the market absolutely going gangbusters in 2022 up until the end of the year and backlogs being stretched out. So, when they were selling a lot of homes, they were ordering a lot of homes, but they weren’t able to get those immediately. And so you just — you had a situation where the demand really dried up from the retail customer. And then as backlogs came in, I think that there was a lot of inventory that was forced on these dealers and they were having trouble selling it. And then you’ve got the carrying cost going up as well. So I mean, I think a lot of these guys were in pretty tough shape. And the show was surprisingly optimistic.

I mean we were pretty worried about turnout and about — especially about orders. I mean we kind of thought that, at a minimum, people would come to party in Fort Worth with us, but we were worried about the order front. And so I think the good news is we’re seeing a lot of dealers sell homes and a lot of those homes have been sitting for a while. And so it’s good to see them start to move. We have ran some specials. And I think the sales effort on the dealer side was great. And now they’ve just got to focus on executing and moving any aged inventory they have. But we’re — what we haven’t seen yet is a reorder rate that’s as high as we like it. And I think that that’s mainly driven by the carrying cost of the inventory being higher. But I think as these guys continue to sell homes, they’ll continue to order homes and it’s nice to have that piece of our business moving in the right direction because at the beginning of the year, that certainly wasn’t the case.

Jay McCanless: Great. And then I guess you answered my price question, I think, but just this mid-60% — mid to low 60%s, you think that’s probably going to be a good number to use for the next couple of quarters for modeling in terms of average price?

Duncan Bates: Yes, I think so. I think all the customers are a little squeezed. You’ve got on the retail side, inflation has been tough for this customer, and they probably like a little bit larger home, but the payments may not work. And so we’re selling a lot of single [wid]es with — that aren’t, I’d say, fully optioned. And then we see the same thing on the park side, where some of the community owners are going to a little bit smaller homes to keep the monthly payments down for the financing. So I’d say that’s a pretty good number. If we see a big pickup in double [wid]es going out or we hit one of these workforce housing deals, there are a little bit higher units that could go up. But for right now, from a base case standpoint, that feels like a good ASP to me.

Jay McCanless: Okay. And then just one other question. We’ve heard about some commercial banks in the U.S. pulling back and exiting doing floor plan lending for the MH space. Is there any opportunity for Legacy to maybe go a little further afield and pick up some business as some of these banks have been exiting?

Duncan Bates: Yes, absolutely. I mean, I think it’s actually a pretty big opportunity for us. We’ve made some changes to our floor plan program and the team that executes it. But I’d say there’s a lot of dealers that we don’t floor. And so, there’s an opportunity to expand and add some more dealers. We’ve got other dealers that floor with someone else but carry Legacy’s. And so I think there’s an opportunity to convert those over to us as well as add more Legacy homes on their lot. And I still think there’s an opportunity to grow the consumer finance business. We’ve got — we’ve got a lot of dealers that I wouldn’t say we’re their number one financing choice at this point. And so I think there’s an opportunity to make a push there. So you’re adding floor plan financing, but you’re also pushing the consumer lending business as well.

Jay McCanless: Okay. That sounds great. Thanks for taking the questions.

Duncan Bates: Absolutely. Thanks, Jay.

Operator: One moment for our next question. Our next question comes from George Melas-Kyriazi with MKH Management. Your line is open.

George Melas-Kyriazi: Hey, thank you. Good morning, gentlemen. I have a question on production and inventory. My understanding is that you were sort of increasing production in the quarter, but sales, of course, were rather soft and finished good inventory, even though maybe it’s pretty high, it was flat sequentially. So I’m trying to square that and try to understand if you actually did increase production in the September quarter? Or sort of how do you handle that to manage to keep finished good inventory flat?

Duncan Bates: Yes. I mean production in in the quarter was down pretty significantly. I mean, I felt like third quarter was about the lowest that we were running at all the plants. And we still — we did miss a production day, but we’re really building three homes on average at each plant, which was down pretty significantly from kind of mid-2022 or third quarter of ’22. Now, we’ve got a little bit of an easy comp, because in the third quarter of ’22, that’s when we really started having the issues at Georgia. And so production was down in the third quarter. We’re taking it up in Texas now. We’ve still got some work to do in Georgia. We haven’t ramped production up there. We’ve got too much finished good inventory at Georgia that we’re working to move. And I really feel like by Q1, we’ll be back on track there. We’ll get a lot of that finished goods inventory shipped, and we should have the orders to start taking up production at that time.

George Melas-Kyriazi: Okay. And remind me, Georgia, that’s mostly park homes? Or is it also to the retail channel?

Duncan Bates: Yes, it’s both. We’ve got a couple of large park customers there. So, we have built a lot of that product, and they’ve been just kind of large, I’d say, good entrepreneurs that have large real estate portfolios, and they’ve bought a lot of homes from us, and they’ve been pretty loyal. And so, we’re — we appreciate them. But we’ve also — we have a — Legacy has a dealer presence in the Southeast through Heritage Housing. And we also have some independent dealers there. But as I add to that sales team, we’ve hired a lot of people. I mean, I think we’ve hired seven or so salespeople in the past few months. And we need to get back on track with the dealer business. It’s just — it’s a large territory. And so you can’t have two people covering the entire Southeast for dealers effectively. So, I think there’s a lot of opportunity there now that we’ve gotten through the quality issues and the service issues and they’re starting to regain our customers’ trust.

George Melas-Kyriazi: Okay. That’s great news that quality has improved. Question about sort of cash, your loans and your line of credit. Your line of credit, of course, was unused at the beginning of the year, and now you have $13 million. So, you seem to find good opportunities to increase your own portfolio. Do you think that continues, or is there a limit to that?

Duncan Bates: Yes. I mean, cash is king right now. And so, if you’ve got the ability to lend into this industry, there’s plenty of opportunities. And so, we’re being selective, but we have had some good opportunities to put money to work at pretty attractive yields even though the cost on anybody’s bank line that’s variable is fairly high right now. And so, we’ll be selective. We’re not going to go crazy, but we’re certainly not going to turn down good opportunities to either invest in the loan portfolios or on the development loan side where we can put money to work with a lean on a property and a personal guarantee at kind of high teens yields.

George Melas-Kyriazi: Okay. Makes sense. And then just a final quick question. It seems like your own retail operation seems to be doing a little bit better. Have you worked out some of the kinks there? Or…

Duncan Bates: Yes, we’re working on it. I think Heritage has a lot of potential. I mean we haven’t added additional locations in a couple of years, and we’re seeing some opportunities to do that. But the key is getting the management team in place. We’ve made a few changes at the senior management team. We’ve got a few additions that we need to make. But I feel pretty good about how Heritage is being managed and we’re selling more production through Heritage than we have in the past. And I think — but it’s still lower than where we would like to be. And so that’s another area that I feel like we have a — with the right team, we’ve got a good opportunity to grow that side of our business. And it’s still significantly below where our peers are in terms of production that we are selling through our company-owned retail stores. So I just — I think there’s a big opportunity in Heritage.

George Melas-Kyriazi: Great. Thank you very much.

Duncan Bates: Yes, thanks.

Operator: One moment for our next question. Your next question comes from [Ramon Numshoff] (ph), who is a private investor. Your line is open.

Unidentified Analyst: Thank you. Hey, Duncan and Jeff, congrats on a great quarter. I wanted to ask a question related to the land development. Maybe if you can give us a little bit more specificity regarding who you hired as part of this new team and sort of what the overall vision is for that whole business?

Duncan Bates: Yes. I mean we’re still — we’re in kind of the early stages of it. We broke the developments up into regions, and we’ve got essentially a regional manager with some team members below him in each region. And the goal right now is just to prioritize and accelerate the development on these properties. And so, like I was speaking about earlier, we’ve got three buckets we’re looking at. I think some of them, as we dig a little bit deeper, may make sense to sell. There are some that may make sense to hold. And then, they are certainly the ones that we’ve made good progress on that we’re really trying to push forward quickly. And so, I’ll continue to provide updates. I understand it’s kind of — it’s high level, but I’m still getting my arms around it and making sure that whatever decision we make on these properties, they’re all being executed from the lens of creating the most value for the shareholders.

And so, it’s not going to be overnight, but I think that the easy ones are either, hey, we need to accelerate this, or hey, we should just look at selling this, and what’s it worth, and if there’s something that make sense to sell, and you can make 3 times, 4 times, 5 times your money, it’s probably a good opportunity to do that.

Unidentified Analyst: Thanks. That’s helpful. I guess my question is, do you see this as like a vertical of the business? Like is this going to be a full rent type of product that’s going to be held on the balance sheet for a long time and you’re just going to sort of accelerate? Or is this something that’s more of — I guess I’m trying to figure out if this is a trade, or is this a long-term hold?

Duncan Bates: Yes. I’m trying to figure that out too. Look, the biggest headwind of this — in this entire industry is where to put these homes. And so, I think if you can create a model that is — that you can replicate over and over again that allows our customers to sell homes into communities, that’s a pretty good model, but it’s going to take some time to get there. And so that’s — I mean you hit the nail on the head. That’s what I’m trying to understand now. I’d like to think that we can come up with something pretty creative where this is a model that we can replicate and solve the largest headwind for our industry, but I’m not — and we have a good starting point. We just have to execute on that and use the knowledge to create something that we can replicate over and over again. And so that is precisely what I’m trying to figure out.

Unidentified Analyst: And sorry, one more question on this. What do you think is the biggest headwind for you to sort of figure this out? Is it capital? Is it time? I mean, what is the limiting capital to sort of…

Duncan Bates: I think we’ve got the capital. I think we’ve just got to understand how it’s viewed and — from a public market standpoint and how the cash flows will be valued, and that’s going to determine if these are long holds, or are these, can you get them to a point where you can maximize the value for the shareholders. Because if I add — if I finished Del Valle and I’ve got 1,100 spaces and rents coming off of those, are investors going to value that at 7 times earnings or are they going to value it like some communities at 30 times earnings? And so, I don’t know the answer to that question yet.

Unidentified Analyst: Understood. Thank you so much.

Duncan Bates: Yes, thank you.

Operator: And I’m not showing any further questions at this time. I’d like to turn the call back over to Duncan for any closing remarks.

Duncan Bates: Sure, thank you. I’d like to thank everybody who joined today’s earnings call. We certainly appreciate your interest in Legacy. And operator, this concludes our call.

Operator: Ladies and gentlemen, this does conclude today’s presentation. You may now disconnect, and have a wonderful day. ##

Part II – Additional Information with More MHProNews Analysis and Commentary

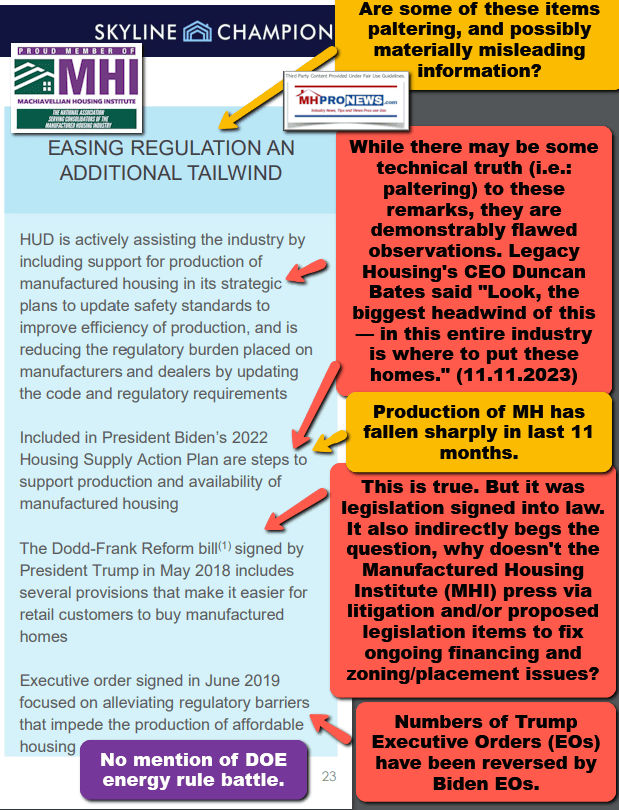

Every highlighted item above is significant. But the two items highlighted above which are provided below for clarity and emphasis are perhaps at or near the top of the most important manufactured housing industry-macro topics.

Per Legacy’s CEO Duncan Bates:

- “Like other manufacturers, we have battled delayed shipments due to setup-related issues, discriminatory zoning practices and high interest rates are headwinds for new developments.”

- “Look, the biggest headwind of this — in this entire industry is where to put these homes.”

Compare Bates’ remarks about zoning barriers on behalf of Legacy Housing (LEGH) with what Cavco Industries (CVCO) and Skyline Champion (SKY) said in their recent quarterly reporting and related investor relations (IR) informational pitches.

Numerous points could be made about the Legacy Housing earnings call. Some of those were previously discussed in the report linked below. The evidence-based case can be made that in several ways, Legacy is outperforming larger rivals at MHI.

But to leave the focus with the regulatory hurdles that manufactured housing has faced despite 15+ years since the Duty to Serve (DTS) manufactured housing was enacted, or the almost 23 years since the Manufactured Housing Improvement Act of 2000 (MHIA) and its so-called “enhanced preemption” provision was made law, let’s wrap up for today on that startling contrast between Bates candor and the apparent paltering and arguably misleading remarks in Skyline Champion and Cavco Industries pitches as noted in the annotated graphics above. Legacy’s Bates was blunt. “Look, the biggest headwind of this — in this entire industry is where to put these homes.” Skyline and Cavco are seemingly attempting to mislead some investors and perhaps others into thinking that the circumstances of manufactured housing are better than they are.

This is the problem with paltering and attempting to mislead by whatever label one wishes to accurately use to describe arguably deceptive remarks deployed by MHI and several, but not all, of their members. The deceptive behaviors and remarks have been going on for so long that those who use such statements may not be able to nuance in a way that could be used to justify the various conflicting statements.

This inquiry was put to Bing AI. Note that it is the Manufactured Housing Association for Regulatory Reform (MHARR) that is twice cited by Bing AI in its response, not MHI.

> “Explain the potential benefit of the Manufactured Housing Improvement Act of 2000 and its so-called “enhanced preemption” provision in its ability to overcome zoning barriers.”

> “Can you find any evidence that the Manufactured Housing Institute, Clayton Homes, Skyline Champion, or Cavco Industries has deployed legal resources to attempt to use the courts to enforce enhanced preemption?”

Learn more:

![DuncanBatesPhotoLegacyHousingLogoQuoteZoningBarriersLookBiggestHeadwindIinThisEntireIndustryIsWhereToPut[HUDCodeManufactured]HomesMHProNews](http://www.manufacturedhomepronews.com/wp-content/uploads/2023/11/DuncanBatesPhotoLegacyHousingLogoQuoteZoningBarriersLookBiggestHeadwindIinThisEntireIndustryIsWhereToPutHUDCodeManufacturedHomesMHProNews.webp)

Bates’ remarks serve to reinforce the prior statements by Legacy’s co-founder and chairman of the board, Curtis “Curt” Hodgson on the zoning/placement barriers, which he called a “place to put” problem.

For all the dancing, prancing, and metaphorical romancing deployed by MHI and its ‘insider’ members, when all the known facts are examined, what emerges is a vexing snapshot of the manufactured housing industry. There are those involved in the Manufactured Housing Association for Regulatory Reform (MHARR) who are steadily seeking to expose how existing federal laws could create a boom for the manufactured home industry. In fairness, some at MHI may also sincerely want to see “enhanced preemption” under the MHIA and other federal laws, such as the Duty to Serve (DTS) or more useable lending under the FHA Title I program turned from words in the Federal Register into robustly enforced laws. Even the Government Accountability Office (GAO) has tagged HUD for failing to implement needed reforms.

Legacy’s leadership has more or less successfully worked at looking at the issues blunting manufactured housing and dealing with those issues themselves. To address the lack of industry lending in the chattel loan arena, Legacy has long had a profitable captive lending program. To deal with the “place to put” challenge, Legacy began buying land with the aim of creating opportunities to place their own homes on their own properties. While that second effort, as Bates made clear, is not yet bearing fruit, that doesn’t mean that it won’t. Meanwhile, their land investments are growing in value.

But obviously not all companies can rapidly replicate what Legacy has done, by creating captive lending and investing in possible developments. Those are capital intensive efforts, meaning portfolio lending and developing. That creates barriers of entry, sustainability, and exit for actual or potential manufactured home producers, retailers, and others.

This article opened in part with this part of the preface. EF Hutton analyst Tim Moore, CFA said “congratulations on the continued good operational execution” to Legacy’s CEO Duncan Bates, “it’s vastly improved since you took over Duncan.” Kurt Shipley and Curt Hodgson apparently felt that Bates could benefit their firm, and per Moore, he has.

What is generally working for Legacy has been or is being replicated to some degree by others. For instance.

- Skyline Champion has deployed capital to create their own ‘captive’ lending in a deal with ECN Capital/Triad Financial Services. They have recently stressed the importance of that lending program as part of their strategic plan.

- To a significant extent captive lending helped make Clayton Homes move from the number four producer of HUD Code manufactured housing pre-Buffett/Berkshire Hathaway buyout to the runaway #1 manufactured home producer post-Berkshire acquisition of Clayton Homes and their lending.

Clayton, Skyline Champion, and Cavco Industries may have the capital and capital access needed to buy and develop properties where manufactured homes could be placed and sold. Legacy, now that Regional Homes has been acquired by Skyline Champion, could be the #4 largest producer of HUD Code manufactured homes and the largest remaining ‘independent’ in the industry. While Bates has previously signaled that they may do some acquisitions of their own, thus far, no deals have been announced. Bing AI said the following: “Duncan Bates was appointed as the President and CEO of Legacy Housing Corporation in June 2022. I could not find any evidence of Legacy Housing Corporation announcing any acquisition deals since then,” and provided a link to the report below.

While manufactured housing was described as an oligopoly by the late Sam Zell, there are still some firms that are in ‘competition’ with each other.

Legacy generally stays clear of industry politics, and per sources, doesn’t routinely attend MHI meetings. At trade shows, they are focused on selling product.

To learn more about Legacy or the topics discussed, see the linked and related reports.

Part III – is our Daily Business News on MHProNews stock market recap which features our business-daily at-a-glance update of over 2 dozen manufactured housing industry stocks.

This segment of the Daily Business News on MHProNews is the recap of yesterday evening’s market report, so that investors can see at glance the type of topics may have influenced other investors. Thus, our format includes our signature left (CNN Business) and right (Newsmax) ‘market moving’ headlines.

The macro market move graphics below provide context and comparisons for those invested in or tracking manufactured housing connected equities. Meaning, you can see ‘at a glance’ how manufactured housing connected firms do compared to other segments of the broader equities market.

In minutes a day readers can get a good sense of significant or major events while keeping up with the trends that are impacting manufactured housing connected investing.

Reminder: several of the graphics on MHProNews can be opened into a larger size. For instance: click the image and follow the prompts in your browser or device to OPEN In a New Window. Then, in several browsers/devices you can click the image and increase the size. Use the ‘x out’ (close window) escape or back key to return.

Headlines from left-of-center CNN Business – from the evening of 11.29.2023

- GM lavishes shareholders with cash weeks after saying it couldn’t afford workers’ demands

- GM cuts spending on Cruise self-driving cars

- The Okta Inc. application for download in the Apple App Store on a smartphone arranged in Dobbs Ferry, New York, U.S., on Sunday, Feb. 28, 2021.

- Identity management company Okta reveals far more extensive hack of its systems

- Jamie Dimon says to be prepared for recession

- Rite Aid is closing another 30 stores

- The Jezebel website is seen on a laptop on November 9, 2023.

- The US economy grew by 5.2% in the third quarter, even faster than previously estimated

- From turtle doves to lords-a-leaping, the price of the ‘12 Days of Christmas’ just hit a record high

- After year of ‘fixing things,’ Bob Iger tells Disney employees his plans to reshape the company for the future

- The dollar is heading for its worst month in a year. It’s not all bad news

- Kraft’s newest Mac & Cheese is ditching cheese

- Charlie Munger’s best quotes on investing, life and everything in between

- The holiday spending spree is fueled by ‘Buy Now, Pay Later’ shoppers

- Charlie Munger mourned in China, where he said his best investment was made

- Elon Musk visits destroyed kibbutz and meets Netanyahu in wake of antisemitic post

- Charlie Munger, friend and business partner of Warren Buffett, dies

- Uber announces partnership with London’s iconic black cab taxis

- Harvard student groups issued an anti-Israel statement. CEOs want them blacklisted

- Thanksgiving weekend deal hunting crowds broke records but their spending didn’t

- FTC can seek tough new restrictons on Meta’s use of personal data, federal judge rules

- Rupert Murdoch to be deposed in Smartmatic’s election defamation case against Fox News

- Harvard, Penn and MIT presidents to testify before Congress on antisemitism

- Students are lawyering up in the wake of the Israel-Hamas war

Note: to expand this image below to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

Notice: our image capture for this Daily Business News on MHProNews feature failed yesterday.

MHProNews regrets that error. That said,

the Manufactured Housing Industry Connected Stocks and other Equities Capture is Below as Usual.

Headlines from right-of-center Newsmax 11.29.2023

-

- GOP Weighs Formal Vote to Authorize Biden Impeachment Inquiry

- President Joe Biden salutes while boarding Air Force One at Denver International Airport on Wednesday. (Andrew Caballero-Reynolds/Getty Images)

- GOP Weighs Formal Vote to Authorize Biden Impeachment Inquiry

- The House Republicans under Speaker Mike Johnson, R-La., are weighing a formal vote on an impeachment inquiry into President Joe Biden amid continued allegations of Democrat obstruction. “While we take no pleasure in the proceedings here, we have a responsibility to do it,” Johnson said at a press conference Wednesday with the leaders of the investigation. [Full Story]

- Related Stories

- Comer: Hunter Must Comply or Face Charges

- Comer Wants to Hear From Freed Hostage’s Aunt

- Comer: Deposition First, Then Public Hearing

- Jason Smith to Newsmax: Hunter Subpoena Not Negotiable

- Ben Cline: Dems Obstructing GOP Oversight

- Hunter Biden Offers to Testify Publicly, Sans Deposition

- Israel at War

- Kin of US Hostages Describe Anguish, Implore Urge Govt. to Help

- Report: Hamas to Release 1 American

- CIA Official Posted Pro-Palestinian Image to Facebook

- Glick: Biden Primary Obstacle to Israeli Victory

- IDF’s Lt. Col. Lerner: Israel Focused on Hostage Rescue | video

- Family Told of Claims 10-Month-Old Hostage Killed

- Freed Israeli Hostages Tell of Beatings, Death Threats

- UN Chief: Gaza in ‘Epic Humanitarian Catastrophe’

- Can Hamas Locate Remaining Hostages in War’s Mayhem?

- Blinken in Mideast, Seeks New Cease-Fire Extension

- 3 IDF Soldier Hostages Now Confirmed Dead

- UN Calls for 2-State Solution to Israel Conflict

- Hamas to Release 2 Russian-Israelis in Side Deal

- Pope Calls for Release of All Hostages, Ongoing Truce

- 10 Worst of Hamas Returned for Israeli Hostages |Platinum Article

- More Israel at War

- Newsmax TV

- James: US Must Stand for Israel, Against Antisemitism

- Ben Carson: Hamas Hijacks the Narrative

- Burchett: Comer’s Biden Probe ‘Over the Target’ | video

- Biggs: Hunter Has to Come In Like Anyone Else | video

- Fallon: ‘Every State a Border State’ Under Biden

- IDF’s Lt. Col. Lerner: Israel Focused on Hostage Rescue | video

- Comer: Liz Hirsh Naftali’s Testimony Sought | video

- Comer: Hunter Must Comply or Face Contempt | video

- DeSantis: Biden Failing Troops | video

- Jason Smith: Hunter Biden Subpoena Not Negotiable | video

- Huckabee: GOP Call for Two-State ‘Dumb Idea’ | video

- More Newsmax TV

- Newsfront

- Jailed US Marine Vet Paul Whelan Attacked in Russian Prison by Another Inmate

- Marine veteran Paul Whelan was attacked by another inmate in a Russian prison while serving a 16-year sentence on espionage charges, Russia’s prison service said on Wednesday, after Whelan’s brother publicized the incident.The U.S. Embassy in Moscow has been in phone…… [Full Story]

- JPMorgan’s Dimon Tells Corporate Leaders to Back Haley

- JPMorgan CEO Jamie Dimon on Wednesday told a group of wealthy [Full Story]

- Sands Casino Family to Buy Mavs Majority From Cuban

- Dallas Mavericks owner Mark Cuban has entered into an agreement to [Full Story]

- Related

- Mark Cuban: No Plans to Run in 2024

- US Suicide Numbers Hit New Record High in 2022

- S. suicide numbers reached a grim new high in 2022.The increase was [Full Story]

- Disney CEO to Step Down at the End of 2026

- Walt Disney CEO Bob Iger said at the Dealbook conference he “will [Full Story]

- Kerry: US, China to Work Together at Climate Summit

- The United States will work with China to make the United Nations [Full Story]

- Related

- COP28 Leader Denies Using Talks to Push Oil Deals

- New Jersey ‘Virtue Signaling’ With Gas-Powered Vehicle Ban |Platinum Article

- Virgin Jet Lands Maiden Transatlantic Low-Carbon Fuel Flight

- 10 Worst Offenders Hamas Received for Israeli Hostages

- Israeli families rejoiced this weekend after some of the hostages [Full Story] | Platinum Article

- Trump Rails Against Courthouse Campaigning

- Former President Donald Trump, who is the frontrunner for the 2024 [Full Story]

- Related

- Morning Consult Poll: Trump Up 50 on GOP, Tied With Biden

- Trump Campaign Sells Mug Shot Wrapping Paper

- Trump Urges Adams, Cuomo to Fight ‘Unconstitutional’ Sex Allegation Law

- Report: Ga. Prosecutors Oppose Deals for Trump, Giuliani

- SPONSOR: NASA scientist discovers baldness breakthrough

- ‘Hair Fertilizer’ Grows Crazy Amounts of Hair

- SPONSOR: NASA scientist discovers baldness breakthrough [Full Story]

- Blinken: ‘No Sense of Fatigue’ With Ukraine Support

- Secretary of State Antony Blinken said Wednesday that there was “no [Full Story]

- Related

- Ukraine Official: No Sign of War Fatigue From NATO

- NATO’s Stoltenberg: Russia Has Large Pre-winter Stockpile

- Russia Preparing ‘Loyalty Agreement’ for Foreigners

- Ukraine Has Only 300K of EU’s Promised Million Shells

- Kremlin: Polish Troops at Border Will Stoke Tensions

- Russia Attacks Ukraine With 21 Drones, 3 Missiles

- Arizona Election Officials Indicted by Grand Jury

- Officials in a rural Arizona county who delayed canvassing the 2022 [Full Story]

- Biden White House Christmas Tree Back Up After Fall

- The National Christmas Tree in front of the White House fell down [Full Story]

- Disney’s ‘Wish’ Bombs at Box Office

- The Walt Disney Company commemorated its 100th anniversary with [Full Story]

- Related

- Disney Admits Its Left-Wing Politics Hurt Shareholders

- Rosalynn Carter Eulogized in Georgia Ceremony

- Her frail husband a silent witness, Rosalynn Carter was celebrated by [Full Story]

- CIA Official Posted Pro-Palestinian Image to Facebook

- A high-ranking CIA official posted a pro-Palestinianimage to Facebook [Full Story]

- US Navy Downs Houthis Drone Launched From Yemen

- A U.S. Navy warship sailing near the Bab el-Mandeb Strait shot down a [Full Story]

- Cardinal Burke 2nd Conservative Pope Critic Punished

- Pope Francis has punished one of his highest-ranking critics, [Full Story]

- Related

- Pope Still ‘Not Well,’ Aide Reads Speech

- Pope Calls for Continued Gaza Truce, Release of All Hostages

- US Catholic Bishops Cling to Fossil Fuels Despite Pope’s Climate Push

- Priests for Life Seeks Info on ‘Targeting’ Pro-lifers

- Pope Cancels Dubai Trip Due to Lung Inflammation, Breathing Issues

- ADL: 73 Percent of College Jews Saw Antisemitism

- Nearly three in four Jewish college students in the United States who [Full Story]

- Related

- Dem Sen. Schumer Laments Antisemitism Surge

- McCarthy: Haley Should Be Trump’s VP Pick

- Former Speaker Kevin McCarthy, R-Calif., said former President Donald [Full Story]

- Related

- Ousted Speaker McCarthy Remains Undecided on Future

- GOP Weighs Formal Biden Impeachment Inquiry Vote

- House Republicans are considering holding a formal vote next month to [Full Story]

- Dylan Mulvaney Tops Forbes 30 Under 30 List

- Forbes magazine includes LGBTQ activist Dylan Mulvaney on its “30 [Full Story]

- Pope Francis’ Lung Inflammation Persists

- Pope Francis presided at his weekly audience with the public at the [Full Story]

- Comer: Hunter Must Comply or Face Contempt

- The House Oversight and Accountability Committee will recommend [Full Story] | video

- Indian National Charged With Conspiracy to Kill Sikh Separatist

- The U.S.charged an Indian national with conspiring to assassinate a [Full Story]

- Alec Baldwin Settles Lawsuit Over Instagram Posts: Report

- Alec Baldwin has reportedly reached a settlement in a $25 million [Full Story]

- Taylor Swift Is Spotify’s Most-Streamed Artist of ’23

- It’s her, hi – Taylor Swift is Spotify’s 2023 most-played artist. [Full Story]

- 3rd Quarter GDP Revised Up to 5.2 Percent

- Shrugging off higher interest rates, America’s consumers spent enough [Full Story]

- FAA Tightens Aircraft Rules After Boeing MAX Crashes

- The Federal Aviation Administration has adopted a new aircraft [Full Story]

- Biden to Target Boebert on Colorado Visit

- President Joe Biden will try to turn Rep. Lauren Boebert of Colorado [Full Story]

- Judge Recuses Himself From Musk-Media Matters Case

- The judge presiding over Elon Musk’s lawsuit against Media Matters [Full Story]

- Report: Ga. Prosecutors Oppose Deals for Trump, Giuliani

- Fulton County, Georgia, prosecutors won’t consider plea deals for [Full Story]

- Amazon Left Scrambling As Shoppers Find out About Secret Deals

- Online Shopping Tools

- More Newsfront

- Finance

- Sands Casino Family to Buy Mavs Majority From Cuban

- Dallas Mavericks owner Mark Cuban has entered into an agreement to sell a majority stake in the NBA franchise to the family that runs the Las Vegas Sands casino company, it was announced Wednesday…. [Full Story]

- Betting on Doom is a Losing Proposition

- Supreme Court Weighs Legality of SEC In-House Ruling

- Is Next Taxpayer Bailout for ‘Too Big to Fail’ China?

- Jet-Set Climate Crusaders Try to Save Us From Cows

- More Finance

- Health

- Don’t Ignore These Early Warning Signs of Dementia

- Forgetfulness is common, but if persistent difficulty with memory and performing everyday tasks is making life challenging, it may be a sign of something serious. It may signal the onset of dementia. According to AARP, dementia is an umbrella term for changes that occur in…… [Full Story]

- Cold Weather Helps Runners Burn More Fat

- New Study Finds That Headaches May Start in the Neck

- Highway Air Pollution Increases Blood Pressure

- How Fast You Need to Walk to Lower Diabetes Risk

Note: to expand this image below to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

-

-

- NOTE 1: Chart above of manufactured housing connected equities includes the Canadian stock, ECN, which purchased Triad Financial Services, a manufactured home industry finance lender.

- NOTE 2: Drew changed its name and trading symbol at the end of 2016 to Lippert (LCII).

- NOTE 3: Deer Valley was largely taken private, say company insiders in a message to MHProNews on 12.15.2020, but there are still some outstanding shares of the stock from the days when it was a publicly traded firm. Thus, there is still periodic activity on DVLY.

- Note 4: some recent or related reports to the REITs, stocks, and other equities named above follow in the reports linked below.

-

2023 …Berkshire Hathaway is the parent company to Clayton Homes, 21st Mortgage, Vanderbilt Mortgage and other factory-built housing industry suppliers.

· LCI Industries, Patrick, UFPI, and LP each are suppliers to the manufactured housing industry, among others.

· AMG, CG, and TAVFX have investments in manufactured housing related businesses. For insights from third-parties and clients about our publisher, click here.

2022 was a tough year for many stocks. Unfortunately, that pattern held true for manufactured home industry (MHVille) connected stocks too. See the facts, linked above.

====================================

Disclosure. MHProNews holds no positions in the stocks in this report.

· For expert manufactured housing business development or other manufactured housing professional services, click here.

· To sign up in seconds for our industry leading emailed headline news updates, click here.

- Note 1: MHVille means manufactured housing industry, MHVille also means artificially smaller manufactured housing (MH) industry,

- Note 2: Manufactured housing, building, factories, retail, dealers, manufactured home, communities, passive mobile home park investing, suppliers, brokers, finance, financial services, macro-markets, manufactured housing stocks, Manufactured Home Communities Real Estate Investment Trusts, MHC REITs.

- Note 3:

APO, Apollo Global Management, BAM, Brookfield Asset Management, BLK, BlackRock, BRK-A, Berkshire Hathaway, BX, Blackstone, CDPYF, Canadian Apartment Properties Real Estate Investment Trust, CIGI, Colliers International Group Inc, CG, The Carlyle Group, CSGP, CoStar Group, CVCO, Cavco Industries, ECNCF, ECN Capital Group, ELS, Equity LifeStyle Properties, FGF, FG Financial Group, FG Communities, KEY, KeyCorp, KMMPF, Killam Apartment REITs, LCII, LCI Industries, LEGH, Legacy Housing, LPX, Louisiana Pacific Corporation, MHC-UN.TO, Flagship Communities Real Estate Investment Trust (REIT), MHPC, Manufactured Housing Properties, MMI, Marcus and Millichap, NOBH, Nobility Homes, PATK, Patrick Industries, SKY, Skyline Champion, SUI, Sun Communities, UMH, UMH Properties, UFPI, UFP Industries.

That’s a wrap on this installment of “News Through the Lens of Manufactured Homes and Factory-Built Housing” © where “We Provide, You Decide.” © (Affordable housing, manufactured homes, stock, investing, data, metrics, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.) (See Related Reports linked herein. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHProNews.

Tony earned a journalism scholarship along with numerous awards in history. There have been several awards, honors and numerous public recognitions for his achievements in manufactured housing. For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. Kovach is a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com, which is ranked as the runaway most read trade media in modern manufactured housing history. This article reflects the LLC’s and/or the writer’s editorial views and may or may not reflect the views of sponsors or supporters.