On October 12, 2023 the U.S. Government Accountability Office (GAO) published a new report entitled “The Affordable Housing Crisis Grows While Efforts to Increase Supply Fall Short.” That GAO report looks specifically at HUD Code manufactured homes. Per the GAO website: “What GAO Does,” “GAO provides Congress, the heads of executive agencies, and the public with timely, fact-based, non-partisan information that can be used to improve government and save taxpayers billions of dollars. Our work is done at the request of congressional committees or subcommittees or is statutorily required by public laws or committee reports, per our Congressional Protocols.”

MHProNews asked Bing AI this question:

> ”Has the GAO allegedly exhibited some level of partisanship?”

The following was Bing’s AI Chat response.

Be that as it may, the information provided ought to broadly be of interest to manufactured housing professionals, investors, and others who believe in the need for a greater access and support for more affordable manufactured homes. There will be more from Bing AI and MHProNews in the analysis that follows in Part II, further below.

While the GAO states their research information differently, which could at times be described as government speak, the GAO findings in several ways confirm concerns raised by the Manufactured Housing Association for Regulatory Reform (MHARR), as well as MHProNews and MHLivingNews on the financing topic.

- Part I (A and B) of today’s report are recent remarks published by the GAO regarding affordable housing and manufactured housing’s role in that arena.

- Part II provides additional information with more MHProNews analysis and commentary.

- Part III is our Daily Business News on MHProNews macro- and manufactured housing connected equities report along with our time saving and insight generating left (CNN) right (Newsmax) ‘market moving’ headline news items.

Significantly to some, the GAO’s report could be described as one branch of the Biden Administration run federal government – the GAO – has formally stated that another branch of the federal government – HUD – hasn’t done its job properly. Ouch, but that too confirms several MHProNews/MHLivingNews evidence-packed reports on the overall housing market and manufactured home industry topics. While new conventional housing starts are beginning to adjust to higher interest rates, both conventional housing and manufactured homes are in a year-over-year decline. Note that by contrast, the Manufactured Housing Institute’s ‘news’ section – on this date and at the time shown – does not mention the GAO report at all. Even the ‘members only’ part of the MHI website only has part of the information about the GAO report posted, per their own search tool.

Note: to expand this image to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

What follows in Part I are the two related GAO press releases. Meaning, the following is the GAO expressing itself in their own ‘government speak‘ words.

Part I (A) – Per the GAO…

The Affordable Housing Crisis Grows While Efforts to Increase Supply Fall Short

Posted on October 12, 2023

Shortages of affordable housing are a long-standing challenge in the United States. High interest rates and low inventory are contributing to this issue, as is the growing number of millennials, who are looking for larger homes to raise families. For low-income Americans, the hunt for affordable housing can be especially tough.

Increasing the supply of housing is one way to address shortages and provide more affordable options. Today’s WatchBlog post looks at our recent work on efforts to expand affordable housing options.

Encouraging affordable housing

The Department of Housing and Urban Development (HUD) leads housing efforts at the national level. This includes everything from mortgage programs to construction. HUD has multiple programs that aim to increase the supply of affordable housing. One of these is the Self-Help Homeownership Opportunity Program (SHOP).

The SHOP program provides grants to nonprofits to help develop affordable housing units for low-income buyers. In our July and September 2023 reports, we found that SHOP grants helped build homes in more than 40 states and 140 metropolitan areas between fiscal years 2011 and 2020.

However, rising land and construction costs have put pressure on the program. For example, land prices increased 60% from 2012-2019, and the cost of homes more than doubled from 1998 to 2021. But HUD doesn’t adjust spending limits for grant recipients’ activities to keep pace with these increased costs. We found that the number of units required to be built with grant funding had declined dramatically overtime.

To help HUD make needed adjustments, we recommended that it use relevant data to determine when and how much to adjust spending limits.

Changes in SHOP’s Affordable Housing Development, FY1998–2020

Manufactured homes—homes that are built in factories—can be an affordable option for some, including lower-income homebuyers. Homebuyers can pay for these homes by taking out a mortgage loan, just like for other home purchases. But sometimes traditional loans are difficult to obtain when purchasing manufactured homes. This could mean that some borrowers use other kinds of financing, such as personal property loans, which can have less favorable rates and terms. Our September report found that HUD and several other federal agencies have taken steps to make manufactured housing loans more affordable. But HUD has not fully implemented proposed changes that would improve homebuyer access to loans for manufactured homes.

We recommended HUD implement planned changes, including establishing time frames and milestones for its actions, to provide additional financing options for manufactured homes.

What about renters?

Many low-income renters also face shortages in affordable housing. During the last three years, rents increased about 24%. HUD’s Housing Trust Fund is designed to preserve and increase the number of affordable rental units available to extremely low-income households. Under this program, HUD provides funding to states for affordable housing rental projects. States have received varying amounts of funding for these projects each year since 2015. And, as of March 2022, the Fund’s grantees had developed almost 2,200 rental units in 263 projects.

Like other housing development and federal grant programs, the Fund faces fraud risks that are important for HUD to monitor. For example, grant recipients must submit audits of the project costs to determine that the funds are used properly. However, we found that the majority of selected grantees did not comply with HUD’s requirements for these audits. In our August report, we found ways to improve HUD’s oversight of the Fund, such as implementing a process to monitor grantee compliance with project reporting requirements.

Housing Trust Fund Allocations for 2022, by State

As demand for affordable housing continues to grow, so will the need for affordable options. Learn more about our work on federal efforts to address affordable housing by checking our key issue page.

- GAO’s fact-based, nonpartisan information helps Congress and federal agencies improve government. The WatchBlog lets us contextualize GAO’s work a little more for the public. Check out more of our posts at GAO.gov/blog. ##

Part I (B)

Manufactured Housing: Further HUD Action is Needed to Increase Available Loan Products

Fast Facts

Manufactured housing—prefabricated, factory built homes—can be an affordable option for lower-income homebuyers. But some borrowers may not qualify for mortgages and might have to turn to other kinds of financing with less favorable rates and terms.

Several federal agencies, Fannie Mae, and Freddie Mac have created new or modified existing loan programs to help manufactured home borrowers. But while the Department of Housing and Urban Development has planned program improvements, it doesn’t have a timeline for putting them in place. We recommended it do so.

What GAO Found

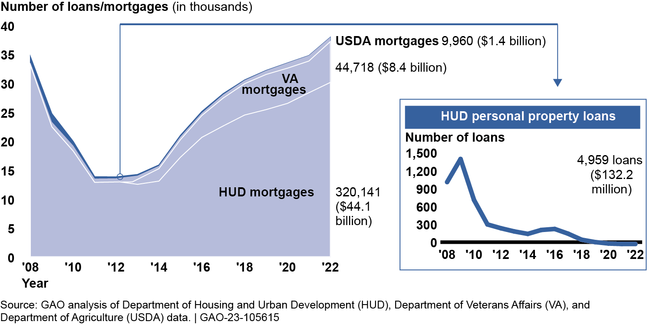

Manufactured housing, prefabricated factory-built homes, can be financed with personal property or mortgage loans. The Departments of Housing and Urban Development (HUD), Veterans Affairs, and Agriculture administer loan guarantee programs for manufactured housing. Federal entities also participate in the secondary market to provide housing finance options. Ginnie Mae guarantees securities backed by federally insured mortgages, and Fannie Mae and Freddie Mac (enterprises) purchase mortgages that are not federally guaranteed and securitize them (package them into securities and sell them to investors).

Federal agency financing of manufactured homes increased for mortgages but not for personal property loans in recent years (see figure). Few personal property loans were made because these loans are capped at an amount lower than the average purchase price of a manufactured home. The limited secondary market for personal property loans also may deter lenders from making them.

Federally Guaranteed Mortgage Loans and Personal Property Loans for Manufactured Housing, Fiscal Years 2008–2022

Notes: Based on available agency data. HUD provided calendar year data for personal property loans and fiscal year data for mortgage loans. VA and USDA provided fiscal year data. VA did not track loans for manufactured housing before 2013.

Several federal entities have supported increasing financing options for manufactured housing. For instance, VA and USDA developed new or modified existing loan programs to assist borrowers. The enterprises expanded eligibility requirements and increased purchase targets to help increase the availability of financing. HUD also has taken some steps to address long-standing requirements to improve the financing and securitization of manufactured housing, but has not fully implemented several proposed changes. Implementing these changes and establishing time frames and milestones for its actions would better assure that HUD could promote the availability and affordability of manufactured homes.

Why GAO Did This Study

The U.S. has a shortage of affordable housing, particularly for low- and medium-income households. Manufactured housing is a source of affordable housing. However, some stakeholders have raised questions about the limited options for financing manufactured housing.

GAO was asked to review the federal role in supporting the financing of manufactured housing. Among its objectives, this report examines (1) trends in the use of federal financing for manufactured housing and (2) federal efforts to assess and improve financing options.

GAO examined federal housing data, reviewed regulations, analyzed information on federal financing products, conducted a literature review, and interviewed federal entity officials and lenders, industry groups, and other stakeholders.

Recommendations

GAO is making two recommendations—one each to the Federal Housing Administration and Ginnie Mae (entities in HUD)—to implement planned changes to increase financing options for manufactured homes, including identifying options for greater securitization of mortgage and personal property loans, and establish time frames and milestones for actions. FHA and Ginnie Mae agreed with these recommendations.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of Housing and Urban Development | The Secretary of Housing and Urban Development should ensure that the Commissioner of FHA implement planned changes to provide additional financing options for manufactured homes, including identifying options for greater securitization of manufactured home mortgages and personal property loans and establishing time frames and milestones for the actions. (Recommendation 1) |

When we confirm what actions the agency has taken in response to this recommendation, we will provide updated information.

|

| Department of Housing and Urban Development | The Secretary of Housing and Urban Development should ensure that the President of Ginnie Mae implement planned changes to provide additional financing options for manufactured homes, including identifying options for greater securitization of manufactured home mortgages and personal property loans and establishing time frames and milestones for the actions. (Recommendation 2) |

When we confirm what actions the agency has taken in response to this recommendation, we will provide updated information.

|

Full Report

##

Part II – Additional Information with More MHProNews Analysis and Commentary

So, the GAO has said that HUD’s secretary (currently Marcia Fudge) has not yet ensured “that the Commissioner of FHA implement planned changes to provide additional financing options for manufactured homes, including identifying options for greater securitization of manufactured home mortgages and personal property loans.” So, despite bluster about the Biden Housing Plan, the GAO said that HUD and the FHA’s efforts are lagging in manufactured housing support. Once more, that confirms reporting by MHARR, MHProNews, and MHLivingNews (see links in preface above and more information linked and stated herein below).

Then recall that the GAO previously got involved with HUD with respect to the Manufactured Housing Improvement Act (MHIA).

The GAO also previously reported on financing and manufactured housing. That was some 9 years ago. Congress itself held hearings on the Manufactured Housing Improvement Act of 2000 in 2011 and 2012. So various branches of the federal government have to some degree recognized the problem. While it begs the question of the obvious problem of the federal government not fulfilling its own legal obligations, it also calls into question MHI’s effectiveness in their self-proclaimed advocacy for “all segments” of manufactured housing.

The good news, to some degree, is that the GAO has done such research, which points out information that is potentially useful for savvy manufactured housing professionals and advocates. Both MHProNews and MHLivingNews have used the illustrations above periodically for some years.

MHProNews recently produced a report that raised some of the same issues that the GAO has now reported.

For instance, according to information generated by prior MHI President and CEO Gail Cardwell, the number of FHA Title I endorsements of HUD Code manufactured home loans cratered years ago. Is it a factor in the 21st century decline of HUD Code manufactured housing? Look at the two graphics that follow and decided for yourself.

Compare and Contrast MHI and with MHARR on the Financing Issue

On paper, the Manufactured Housing Institute (MHI) and the Manufactured Housing Association for Regulatory Reform (MHARR) both appear to support the call for FHA Title I/Ginnie Mae loan reforms, such as removing the so-called 10/10 rule that essentially limited the potential for most manufactured housing lenders from accessing this chattel lending program that once financed tens of thousands of HUD Code manufactured homes.

But upon closer examination, what emerges is a picture that if more FHA Title I loans were being originated (or if the Duty to Serve – DTS – personal property/chattel/home only loan financing from the Government Sponsored Enterprises (GSEs) of Fannie Mae and Freddie Mac were being properly implemented), that would in turn cost Berkshire Hathaway (BRK) lenders in manufactured housing money. Those Berkshire owned lenders – 21st Mortgage Corporation and Vanderbilt Mortgage and Finance (VMF) are MHI member companies, as is Clayton Homes. Warren Buffett himself said during a Q&A at a Berkshire Hathaway annual meeting that the GSEs originating DTS loans would be good for manufactured housing, as the video posted below reflects.

On the governmental support for manufactured housing lending side, flashback to the MOU – the Memorandum of Understanding – by HUD Secretary Marcia Fudge and then-acting director Sandra Thompson.

Recall too that the Manufactured Housing Association for Regulatory Reform (MHARR) offered to assist HUD and the FHFA in the implementation of that plan so as to provide the maximum possible benefit to manufactured housing. But no known outreach in response to that offer from MHARR has occurred. Once more, despite the media fanfare, the GAO report above illustrates one side of the federal government responsible for “accountability” directly saying that another part of government hasn’t done its job. In this instance, failing to do the job is harmful to the interests of affordable housing shoppers, those buyers that were pushed into higher cost loans for a lack of financing options, and these issues play some role in the lack of affordable housing. Government agents tout their efforts, yet fail to do what they claim, as HUD researchers Pamela Blumenthal and Regina Gray have both stated in their own words. With one of the largest ‘peace time’ (to the extent that the U.S. itself is supposedly not officially at war) spending and budgets since World War II (as measured by the ratio of spending vs. GDP), these are examples of federal government researchers pointing out in polite and perhaps ‘politically correct’ words (government speak) that the federal government is simply not efficient at carrying out its own stated goals.

Recall that Doug Ryan with CFED (since rebranded as Prosperity Now) said in an op-ed on American Banker that MHI was not pushing for lower cost chattel lending options because that would cost Berkshire Hathaway owned Clayton Homes and their affiliated lending at 21st Mortgage Corporation and Vanderbilt Mortgage and Finance (VMF) profits. Here is how Ryan said it.

If that sounds vague and perhaps ‘conspiratorial’ at first, Ryan clears up who he is saying is benefiting from “the system” as it stands.

“The Moat” and Manufactured Home Financing

But to illustrate the points made by Ryan, there are the remarks by Buffett-Berkshire “moat” fan, Bud Labitan. The book is entitled: “Moats The Competitive Advantages Of Buffett & Munger Businesses” By Bud Labitan First Edition 2012.

Labitan uses these pull quotes in the book.

- “A truly great business must have an enduring “moat” that protects excellent returns on invested capital. ~ Warren Buffett

- “How do you compete against a true fanatic? You can only try to build the best possible moat and continuously attempt to widen it.” ~ Charlie Munger

Follow along on a highly relevant segue on “the moat” and the lack of manufactured home lending.

MHProNews asked Bing AI the following.

> “Who published Moats the Competitive Advantages Of Buffett & Munger Businesses By Bud Labitan First Edition 2012 and what did Labitan and his researchers say about Clayton Homes and their lending moat?”

Learn more:

Note that Labitan’s book includes these remarks. Clayton and its “moat” specific remarks are found on pages 77-81.

Buffett and Munger respect able and trustworthy managers. As you read about these 70 great businesses, think about the product or service that: (1) is strongly desired; (2) has no close substitute and; (3) has pricing power. As Buffett said, “A moat that must be continuously rebuilt will eventually be no moat at all. Additionally, this criterion eliminates the business whose success depends on having a great manager.”

While this book will help readers learn more about enduring competitive advantages, here is a little reminder about Buffett and Munger’s contribution to behavioral finance.”

Those remarks are stunning, in one sense. Because if you have “a moat” “this criterion eliminates the business whose success depends on having a great manager.” So, for all of the bluster about Kevin Clayton being “a great manager” it begs the question, is Kevin great? Or is it that he has made use of the moat methodology for success? Hold those thoughts, but consider what occurred with ex-Clayton “Chief People Officer” Chase McGee as possibly shedding light on that inquiry.

In a follow up with Bing AI, MHProNews said:

> “Helpful. Didn’t Kevin Clayton make remarks about what Warren Buffett told him about the moat in the context of a video interview with transcript?”

Learn more:

Warren Buffett, Berkshire Hathaway Chairman speaking about “The Moat”, Competitive Advantages, Video Interviews, from Manufactured Home Living News on Vimeo.

Next, MHProNews asked Bing AI this.

> “What did the Nation have to say about Warren Buffett’s moat methods with respect to Clayton Homes and their lending?”

Learn more:

Learn more:

1. advisorperspectives.com 2. advisorperspectives.com 3. realinvestmentadvice.com 4. advisorperspectives.com“

> “Who, if anyone, in manufactured housing trade media raised these issues that Lebowitz, The Nation, The Seattle Times, or Kevin Clayton’s video interview remarks about the Moat, Clayton Homes in manufactured housing?”

Learn more:

> “What has Samuel Strommen said about these issues and what impact it has had on manufactured home lending?”

> “Bing, in fairness, I’m not aware of any declared federal investigation sparked by Strommen’s research thesis, but I am aware of complaints that were made with HUD and the Department of Justice. Can you double check that and clear that up, please?”

However, I could not find any official confirmation or announcement from HUD or DOJ regarding the status or outcome of these complaints…I also could not find any response or comment from Clayton Homes or Berkshire Hathaway regarding these complaints. Therefore, I cannot say for sure what impact Strommen’s paper has had on manufactured home lending. …”

> “Bing, would it be fair to say that Strommen’s paper has brought an evidence-based awareness to some of the concerns that have been widely reported in manufactured housing? For instance, didn’t Strommen make the point that a letter by Tim Williams, CEO of 21st Mortgage Corporation, appears to be an antitrust violation that fostered consolidation in the manufactured home industry?”

Learn more:

To be accurate, but to save the time for yet another follow-up with Bing’s AI, it should be stated that this writer is not aware of Schmitz arguing that the manufactured home industry has been monopolized by Buffett-led Berkshire.

Rather, Schmitz and his colleagues have charged the NAHB and HUD with “sabotage monopoly” tactics, which could be described as evidence of “regulatory capture,” the Iron Triangle, etc. to sabotage manufactured housing. Schmitz’s research-based views on boosting affordable housing and manufactured housing were recently cited in a Congressional hearing, as MHProNews reported. Bing seemed to conflate Strommen with Schmitz at one point, perhaps because they are both mentioned in more than one article on MHProNews, and AI is generating its replies quickly.

That correction noted, Schmitz has said the following. “This [pattern of obscured sabotaging monopoly tactics] leads to whole new set of monopolies, those in [the] manufactured housing industry itself.”

That remark by Schmitz may help close the circle to some extent. In fairness, there are competitors of manufactured housing that have a motivation to ‘subvert’ or “sabotage.” Indeed, there are multiple sources that have made the point that NIMBYism is in part a byproduct of builders flexing their muscles at the local level.

The GAO’s report sheds some light on the federal government’s part in this troubling milieu. Again, the question of regulatory capture and Schmitz’s thesis is worth pondering.

OPB and others reported that a lack of affordable housing is the #1 factor causing homelessness.

There are now multiple antitrust suits that have been launched. That could be additional evidence that Strommen’s thesis was well founded. These are still just some of the puzzle pieces that explain why manufactured housing is underperforming during an affordable housing crisis. The GAO’s report, while it may use some government speak, is nevertheless useful on several levels. Especially so, as a springboard for this type of deeper dive into the issues that are causing manufactured housing production in the 21st century to be at such a low ebb when compared to the manufactured home industry in the last years of the 20th century, from 1995 to 2000. ##

Part III – is our Daily Business News on MHProNews stock market recap which features our business-daily at-a-glance update of over 2 dozen manufactured housing industry stocks.

This segment of the Daily Business News on MHProNews is the recap of yesterday evening’s market report, so that investors can see at glance the type of topics may have influenced other investors. Thus, our format includes our signature left (CNN Business) and right (Newsmax) ‘market moving’ headlines.

The macro market move graphics below provide context and comparisons for those invested in or tracking manufactured housing connected equities. Meaning, you can see ‘at a glance’ how manufactured housing connected firms do compared to other segments of the broader equities market.

In minutes a day readers can get a good sense of significant or major events while keeping up with the trends that are impacting manufactured housing connected investing.

Reminder: several of the graphics on MHProNews can be opened into a larger size. For instance: click the image and follow the prompts in your browser or device to OPEN In a New Window. Then, in several browsers/devices you can click the image and increase the size. Use the ‘x out’ (close window) escape or back key to return.

Headlines from left-of-center CNN Business – from the evening of 10.19.2023

- Why Fed officials aren’t addressing the Israel-Hamas war the way they did with Ukraine

- U.S. Federal Reserve Chair Jerome Powell spoke on the economic outlook at the Economic Club of New York on October 19.

- Fed Chair Powell hints that soaring bond yields could mean end of rate hikes

- America’s frozen housing market: Sales hit a 13-year low

- Mortgage rates advance toward 8%

- An attendee poses for a photograph at a Snapchat stall during the South by Southwest (SXSW) Sydney festival in Sydney, Australia, on Tuesday, Oct. 17, 2023. The event is the first iteration of SXSW to be held outside North America and is expected to attract around 27,000 visitors and inject A$24 million ($15.4 million) into New South Wales state economy, according to the government.

- Snapchat isn’t just for teens anymore. Now it needs to make some real money

- They are tasked with viewing ‘the worst imaginable images’ of the Israel-Hamas war. It’s taking a heavy toll

- The logos of mobile apps TikTok, Facebook and Instagram displayed on a screen in August 2022.

- EU asks Meta for more details on efforts to stop illegal and inaccurate content on Israel-Hamas war

- Rite Aid is closing nearly 100 stores, with more to follow, as part of its bankruptcy. See the list

- Harvard Yard is seen on the closed Harvard University campus in Cambridge, Massachusetts, U.S., on Monday, April 20, 2020.

- Harvard and UPenn donors are furious. It may have a financial domino effect

- New York Attorney General Letitia James speaks outside the courthouse where former President Donald Trump’s New York civil fraud trial is underway in New York City on Wednesday, October 18, 2023.

- New York AG accuses crypto firms of deceiving investors in $1 billion fraud

- Costco’s longtime CEO steps down

- AirAsia chief Tony Fernandes criticized after posting shirtless massage photo on LinkedIn

- How billion-dollar fines are reshaping digital communications in banking

- Nestlé is closing an infant formula factory as China’s birth rate plunges

- US citizen working as journalist detained in Russia

- Nokia says it will cut up to 14,000 jobs

- China’s housing market struggle will weigh on global growth

- From Russia to the Middle East: Why China can’t afford another big conflict

- GM and Honda team up on autonomous ride service for Japan

- UPenn crisis deepens: Former trustee calls for president to resign as donors bail

- Netflix hikes prices again

- Tesla third-quarter earnings slow, missing forecasts

- Delta loyalty program backlash: Airline backtracks on some changes after an uproar from customers

Note: to expand this image to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

Headlines from right-of-center Newsmax 10.19.2023

- Israel’s Defense Minister to Troops: ‘Be Ready’ for Ground Assault

- Meeting with Israeli infantry soldiers on the Gaza border Thursday, Israeli Defense Minister Yoav Gallant urged the forces to “get organized, be ready” for an order to move in for a ground assault. [Full Story]

- Israel at War

- Netanyahu Warns Israel of ‘Long War’ Ahead

- US Warship Intercepts 3 Missiles Heading out of Yemen

- US Intel Says Gaza Hospital Death Toll Likely Between 100-300

- Good: ‘Israel Support Should Stand Alone’ | video

- Gaza Health Ministry: 3785 Palestinians Killed in Israeli Strikes

- Number of Confirmed Israeli Hostages Rises to 203

- Starbucks, Union Battle Over Pro-Palestinian Post

- Hamas Attack Shows Limits of AI, Tech for Global Security |Platinum Article

- IDF Releases Audio of Hamas Admitting Hospital Strike

- Biden Gaffe: Hamas ‘Gotta Learn How to Shoot Straight’

- Biden Mulls $60B Aid for Ukraine, $10B for Israel

- Qatar Plays Key Role to Rescue Hostages

- More Israel at War

- The Race for Speaker

- Jim Jordan Revives Fight, Will Hold 3rd Vote for Speaker

- Van Duyne: House Must Pick Strong Leader | video

- Mike Lawler: GOP Must Find ‘Path Forward’ | video

- Jim Jordan Decries ‘All Threats’ Against GOP Colleagues | video

- Third Ballot Won’t Work for Jordan

- Jordan Loses 4 GOP Votes, Gains 2 More; Next Round Thursday

- Mike Lawler: ‘Need to Find Consensus’ in GOP | video

- Carlos Giménez: McCarthy Had More GOP Votes | video

- Mariannette Miller-Meeks Faces Death Threats

- More The Race for Speaker

- Blackburn: Gaza Aid Won’t ‘Make It’ to Palestinians

- Alan Dershowitz: Must Fight Campus Antisemitism | video

- Lankford: 70K Hostiles Detained at Border | video

- Mike Huckabee: Biden Must Restore Iran Sanctions | video

- Mike Lawler: ‘Need to Find Consensus’ in GOP | video

- Carlos Giménez: Rep. McCarthy Had More Votes | video

- Brian Mast: Don’t Send Aid to Gaza, West Bank | video

- Mullin: Embassy Attack a Test of US Resolve | video

- McFarland: ‘Important’ to See Biden Stand With Israel | video

- Newsfront

- Fed Chair Powell Says Inflation Is Still Too High

- Federal Reserve Chair Jerome Powell said Thursday that inflation remains too high and that bringing it down to the Fed’s target level will likely require a slower-growing economy and job market…. [Full Story]

- US Warship Intercepts 3 Missiles Heading out of Yemen

- A U.S. Navy warship on Thursday took out three missiles that had been [Full Story]

- Kennedy, Schumer Reach Deal on Veterans’ Gun Rights

- John Kennedy and Chuck Schumer have worked out a deal on a bill [Full Story]

- Beth Holloway to Newsmax: ‘Victorious’ Seeing Daughter’s Killer Sentenced

- Beth Holloway, whose daughter Natalee was slain after going missing [Full Story] | video

- Related

- Van der Sloot Admits Murdering Natalee Holloway

- Natalee Holloway Mom to van der Sloot: ‘You’re a Murderer!’

- Mary Lou Retton Suffers Setback in Pneumonia Battle

- Former Olympic gymnast Mary Lou Retton has suffered a “scary setback” [Full Story]

- Russia Carries Out Overnight Air Strikes on Ukraine

- Russian forces carried out new air strikes overnight on targets in [Full Story]

- Related

- Russian Foreign Minister Thanks NKorea for Backing Ukraine War

- N.Y. AG Wants Independent Review in Trump Case

- New York Attorney General Letitia James’ office Thursday accused The [Full Story]

- Massachusetts House Passes ‘Ghost Gun’ Crackdown Bill

- The Massachusetts House of Representatives voted 120-38 Wednesday to [Full Story]

- Hamas Attack Shows Limits of AI, Tech for Global Security

- Hamas’ Oct. 7 attack on Israel is a warning for the West that [Full Story] | Platinum Article

- Border Encounters in September Hit 218K, Most Since 2000

- U.S. Border Patrol recorded 218,777 encounters across the southern [Full Story]

- Fortress Recalls Gun Safes After 12-Year-Old Dies

- More than 60,000 biometric portable gun safes are being recalled [Full Story]

- Israel’s Defense Minister Tells Troops to Be Ready

- Israeli airstrikes pounded locations across the Gaza Strip on [Full Story]

- North Korea Likely Seeking Hypersonics, Satellites From Russia

- Massive shipping containers filled with North Korean weapons and [Full Story] | Platinum Article

- Senate Republicans Urge Biden to Expand Border Wall

- Senate Republicans sent a letter to President Joe Biden on Thursday, [Full Story] | video

- Marine Killed at Camp Lejeune; Second Marine Held

- A U.S. Marine is in custody on suspicion of being involved in the [Full Story]

- UFO Report Reveals 291 New Sightings, Some ‘Unusual’

- The Pentagon and the Office of the Director of National Intelligence [Full Story] | video

- AP-NORC Poll: Most in the US See Mexico as Partner

- Most people in the U.S. see Mexico as an essential partner to stop [Full Story]

- China’s Nuke Arsenal Growing, Aiming for 1,500 by 2035

- A Pentagon report on China’s military power says Beijing is exceeding [Full Story]

- Lawyer Sidney Powell Pleads Guilty in Georgia ’20 Election Case

- Lawyer Sidney Powell pleaded guilty to reduced charges Thursday over [Full Story]

- Fed Remote Work Policies Spark Vacant Office Probe

- The Washington Times is reporting that an inspector general from the [Full Story]

- Putin Claims IOC Using Olympics for Politics, Racism

- President Vladimir Putin on Thursday lashed out at the International [Full Story]

- Woman Arrested at Trump Trial Identified

- A New York state court employee who was arrested after trying to [Full Story]

- CNBC Poll: Trump Leads Biden by 4 at 46%

- CNBC’s All-America Economic Survey, released Wednesday, revealed [Full Story]

- Related

- YouGov Poll: Trump Virtually Tied With Biden

- Woman Arrested Getting Too Close to Trump at Trial

- Trump: Govt Using ‘Vicious Lies’ in Civil Trial

- Trump Backs Gov. Justice Over Sen. Manchin in W.Va.

- Former President Donald Trump endorsed West Virginia’s Republican [Full Story]

- Abbott: Texas Places Barrier on New Mexico Border

- Texas Gov. Greg Abbott on X Wednesday touted his move to further [Full Story]

- Pennsylvania House OKs Bill to Move ’24 Primary

- Pennsylvania’s House of Representatives on Wednesday passed another [Full Story]

- Musk Considering Taking X Out Of Europe Amid Probe

- Elon Musk is considering taking Twitter, or X, out of Europe afterEU [Full Story]

- Activists Turn Backs on US Officials in Geneva

- Dozens of U.S. activists who champion LGBTQ, indigenous and [Full Story]

- Nikki Haley Pushes Back on DeSantis Refugee Claim

- Nikki Haley’s presidential campaign is pushing back against Never [Full Story]

- Biden to Spend $3.5B to Strengthen Electric Grid

- The Biden administration Wednesday announced $3.5 billion for 58 [Full Story]

- Chicago’s Top Cop: Migrants in Police Stations a ‘Burden’

- Chicago’s new police chief said the city’s use of police stations as [Full Story]

- Finance

- Fed Chair Powell Says Inflation Is Still Too High

- Federal Reserve Chair Jerome Powell said Thursday that inflation remains too high and that bringing it down to the Fed’s target level will likely require a slower-growing economy and job market…. [Full Story]

- Hollywood A-List Actors Offer $150M to Help End Strike

- Elon Musk’s EV Demand Warning Sparks Stock Selloff

- US Yields Surge With 10-Year Treasury at Cusp of 5%

- 4 Steps to Improve Your Retirement Savings (Even If You’re Off Track)

- More Finance

- Health

- 10 Best Foods to Lower Cholesterol Levels

- High cholesterol levels increase your risk for heart disease, the leading cause of death, and stroke, the fifth leading cause of death. And yet, according to the Centers for Disease Control and Prevention, about 86 million U.S. adults have cholesterol levels above the…… [Full Story]

- CVS Health to Pull Decongestants with Phenylephrine

- Living Alone Raises Cancer Risk by Nearly a Third

- Eating Red Meat Twice a Week Raises Diabetes Risk

- COVID Treatment Paxlovid Will Cost $1,390 per Course

Note: to expand this image to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

2023 …Berkshire Hathaway is the parent company to Clayton Homes, 21st Mortgage, Vanderbilt Mortgage and other factory-built housing industry suppliers.

· LCI Industries, Patrick, UFPI, and LP each are suppliers to the manufactured housing industry, among others.

· AMG, CG, and TAVFX have investments in manufactured housing related businesses. For insights from third-parties and clients about our publisher, click here.

2022 was a tough year for many stocks. Unfortunately, that pattern held true for manufactured home industry (MHVille) connected stocks too. See the facts, linked above.

====================================

Disclosure. MHProNews holds no positions in the stocks in this report.

· For expert manufactured housing business development or other professional services, click here.

· To sign up in seconds for our industry leading emailed headline news updates, click here.

- Note 1: MHVille means manufactured housing industry, MHVille also means artificially smaller manufactured housing (MH) industry,

- Note 2: Manufactured housing, building, factories, retail, dealers, manufactured home, communities, passive mobile home park investing, suppliers, brokers, finance, financial services, macro-markets, manufactured housing stocks, Manufactured Home Communities Real Estate Investment Trusts, MHC REITs.

That’s a wrap on this installment of “News Through the Lens of Manufactured Homes and Factory-Built Housing” © where “We Provide, You Decide.” © (Affordable housing, manufactured homes, stock, investing, data, metrics, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.) (See Related Reports, further below. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHProNews.

Tony earned a journalism scholarship along with numerous awards in history. There have been several awards, honors and numerous public recognitions for his achievements in manufactured housing. For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. Kovach is a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com, which is ranked as the runaway most read trade media in modern manufactured housing history. This article reflects the LLC’s and/or the writer’s editorial views and may or may not reflect the views of sponsors or supporters.