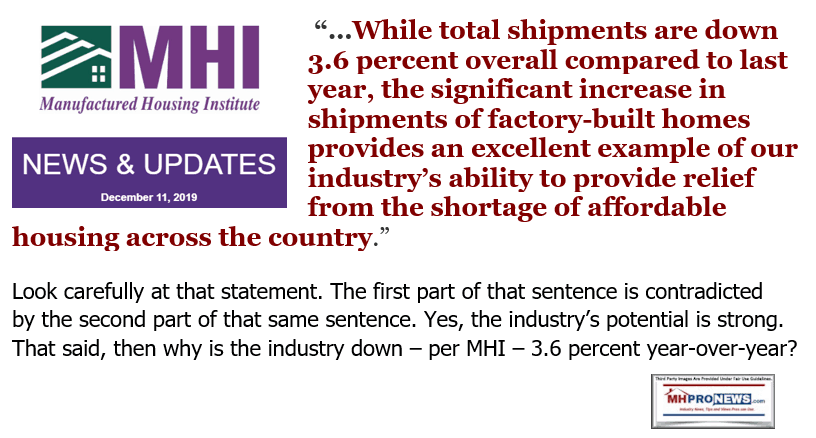

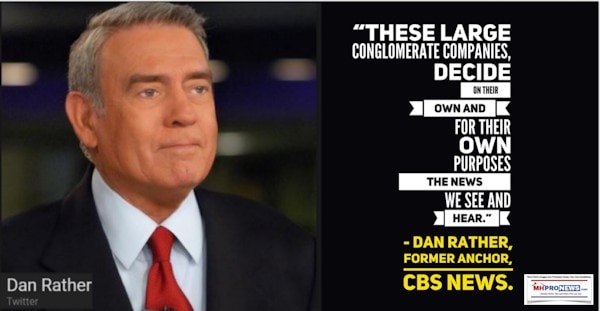

Preface. Based on several surveys, there is a perception held by tens of millions – including from media personalities such as investigative journalist John Solomon – that ‘news’ has become a largely partisan, corporate, or other agenda-driven exercise. That is not to say that all ‘news’ is ‘fake news,’ as psychologist and Director of Media researcher Dr. Chrysalis Wright, PhD, has been cited saying. But there is so much problematic news that a recent public opinion survey reflected that 58 percent – the majority of Americans reflecting a range of political views – believe that the much of mainstream American media are the “enemy of the people.” In response to years of such concerns and our own research as to how those trends are playing out in the world of manufactured housing, MHProNews has for some time periodically refocused our modes of reporting. For example, while regularly providing an opportunity for those who are presenting a narrative that is not in keeping with known facts, MHProNews reaches out for clarification while doing some level of fact check and “fisking” of a specific report or statement. Further, MHProNews periodically does follow ups to see if such fact-checks, analysis, and expert commentary have stood the test of time. In fact, the evidence reflects that such reports by MHProNews in recent years have held up far better than the hidden agenda, paltering, spin, or other narrative driven posturing and claims that are palmed off as genuine ‘news’ by others. That’s perhaps because of the simple yet profound advice of award-winning journalist Sharyl Attkisson. Attkisson, like others in the know, have said “check your facts” – meaning make sure that what is reported is true – and “follow the money.” It is with those notions in mind that this MHProNews Masthead will provide statements by the Texas Real Estate Center, the Manufactured Housing Institute (MHI), and other insights that include the Texas Manufactured Housing Association (TMHA). The specific topics are manufactured home financing and the controversial “CrossModTM” manufactured home plan pushed by Clayton Homes and branded MHI, which is dominated by Berkshire and their consolidation focused allies.

Given that preface, this report and analysis will cover and link the evidence and reports for the following items.

Preview Part I. The Texas Real Estate Center report on MHI branded CrossModTM type manufactured homes.

- Insights from the Texas Real Estate Center’s media relations office, including as it relates to the Texas Manufactured Housing Association (TMHA), the Manufactured Housing Institute (MHI), and Berkshire Hathaway owned Clayton Homes.

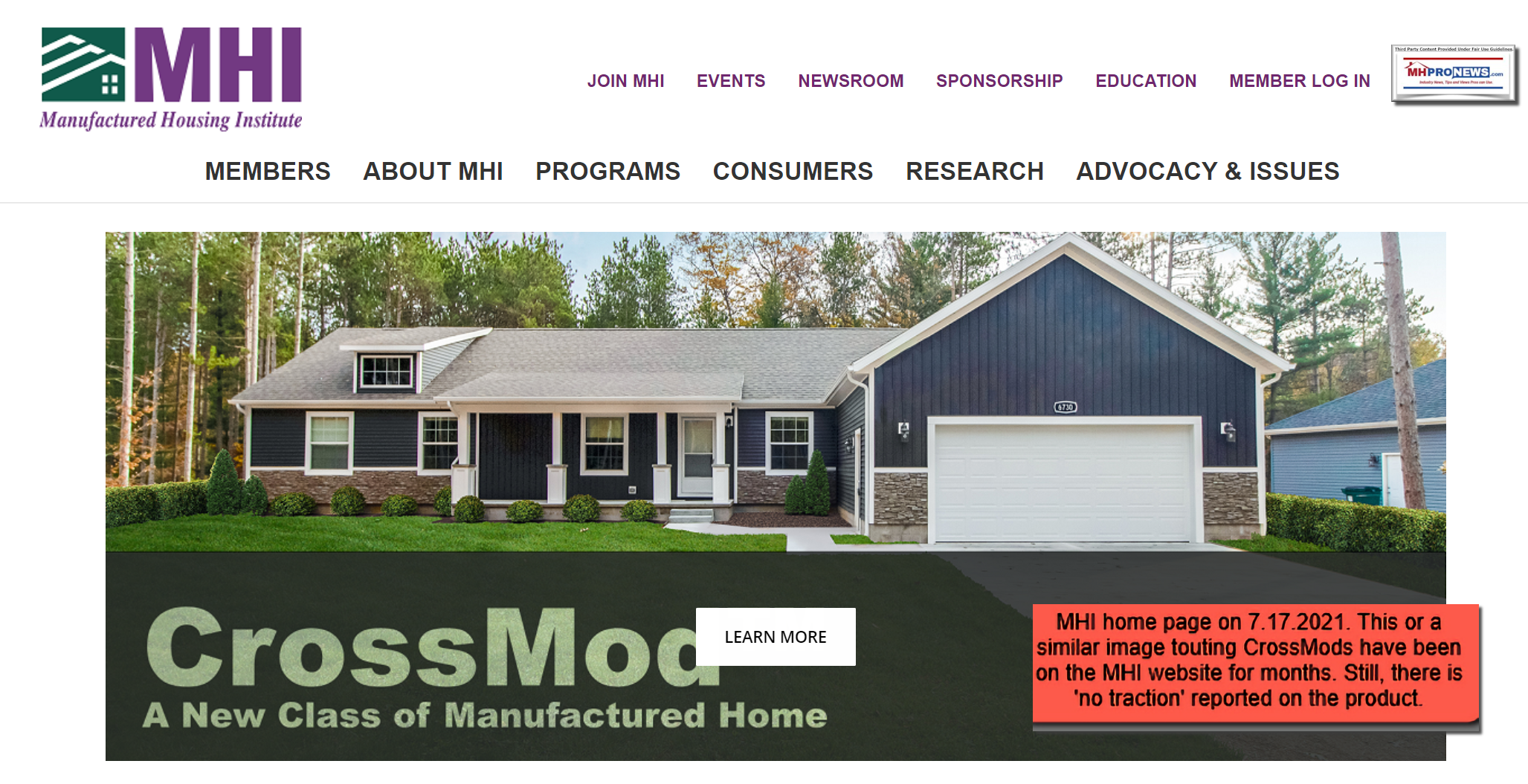

- MHI’s featuring CrossModTM on their home page, as they have for months on end.

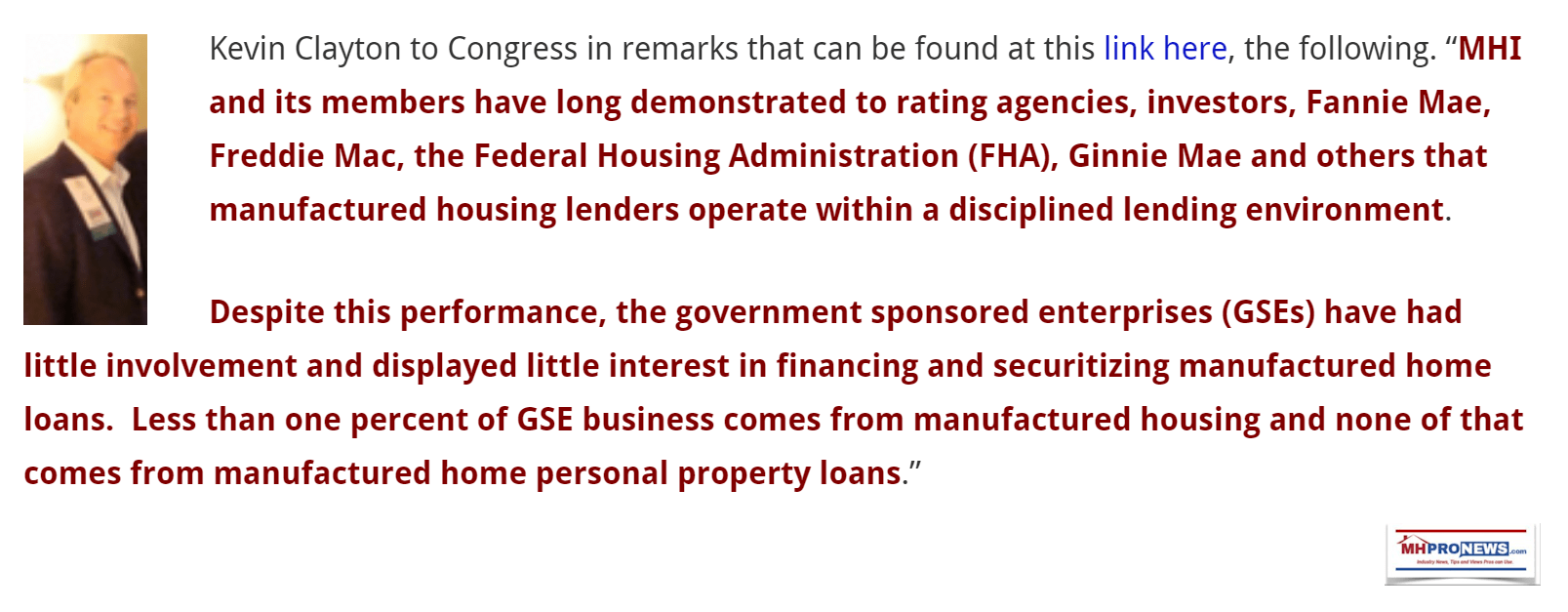

- Evidence vs. claims regarding CrossMod That includes statements to MHProNews by those who are MHI members who say that the program made no sense, because most HUD Code producers already built actual modular homes.

- That Clayton and MHI oddly and routinely continue to push CrossModTM in federal and other testimony, even though it is an apparent market failure.

- How MHI’s hyped claims about CrossMod – that they made based upon research they commissioned as well as by focus-groups.

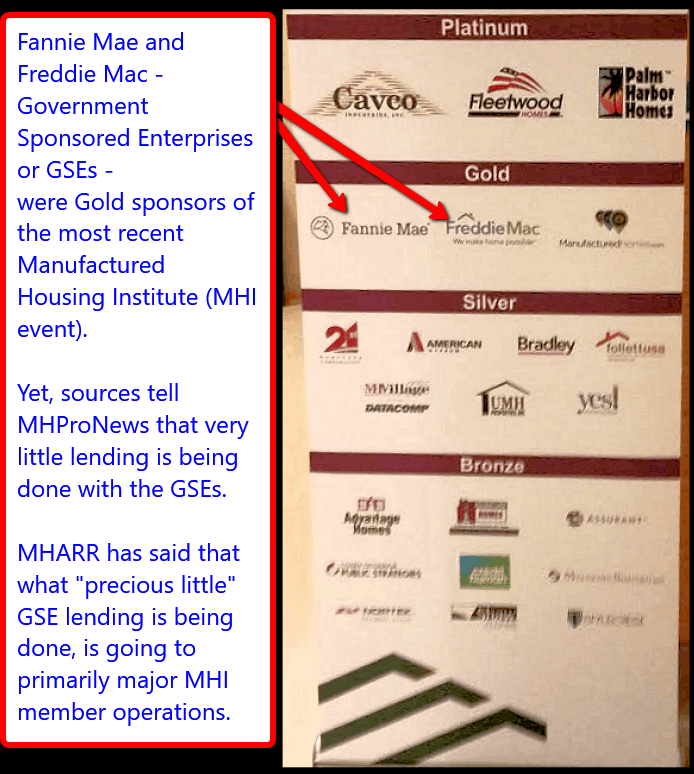

- That Clayton-backed MHI has successfully managed to get special financing on CrossMods by the GSEs, even though the Clayton-MHI essentially admits that they have not managed to get Duty To Serve support for mainstream manufactured homes.

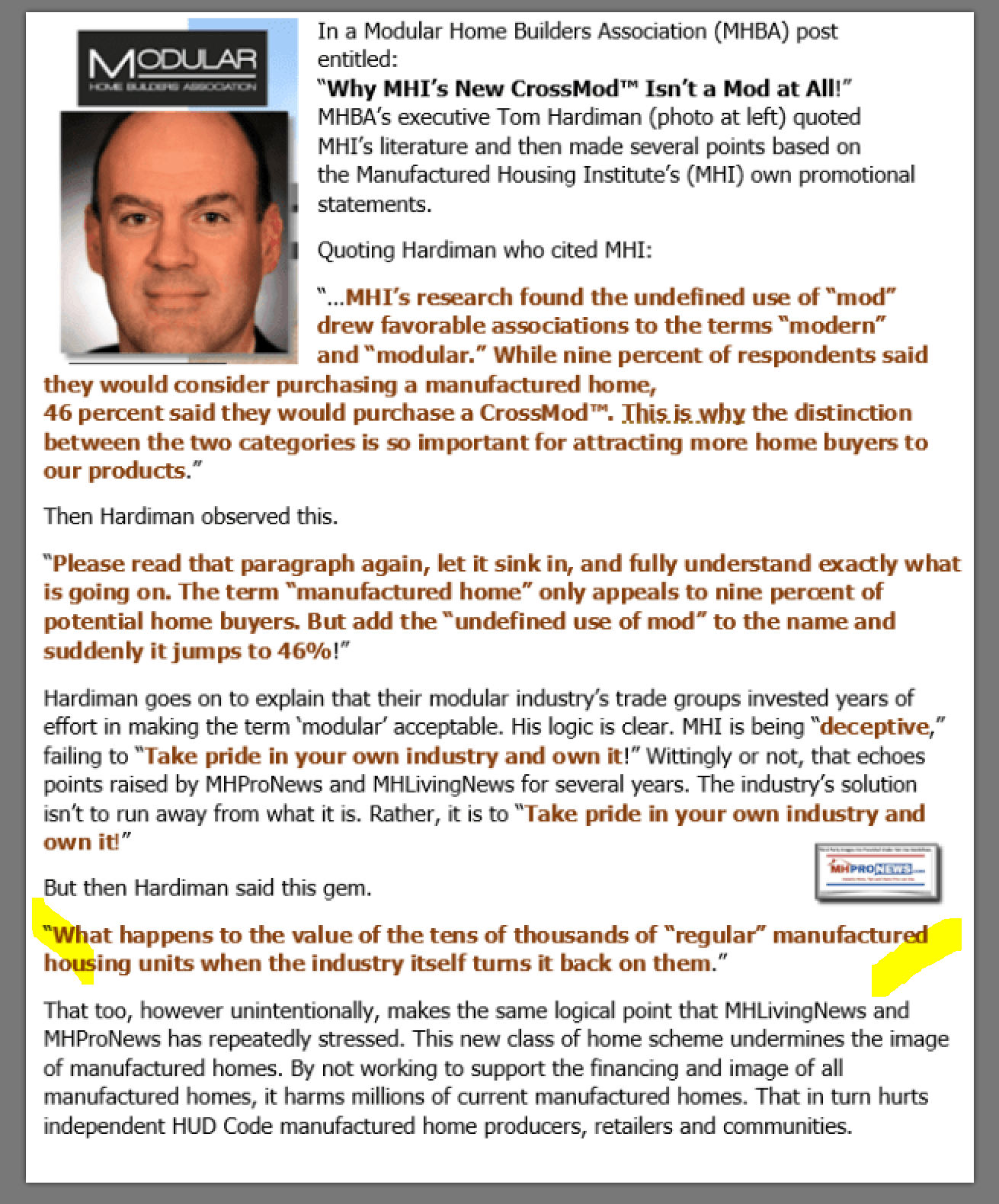

- The rip of MHI’s CrossMods by the Modular Home Builders Association (MHBA) Tom Hardiman, as well as Biden-backed initiatives on housing that they claim are political payoffs.

Preview Part II. That segment of this report and analysis will provide the comments submitted by MHI CEO Lesli Gooch, Ph.D., which may – on the surface – appear to be one of her strongest pitches yet.

- However, what Gooch did not mention, as reflected by prior statements by Kevin Clayton, Doug Ryan, Mark Weiss, and MHI itself are going to reveal what could be a case study in paltering within the manufactured housing industry.

Preview Part III. Close with Solomon’s comments on a distinctive issue apart from manufactured housing as it relates to agenda-driven reporting. While it is not directly manufactured housing connected, Solomon’s statements are still of interest as politics are certainly influencing our industry and the economy at large. Obliquely, Solomon’s contention fits concerns raised by MHBA and the Manufactured Housing Association for Regulatory Reform (MHARR), and other industry voices – including several inside MHI.

With that preface and plan, let’s begin Part I of this report and analysis.

Part I. Engagement with the Texas Real Estate Center report in their Tierra Grande publication on MHI branded CrossModTM type manufactured homes.

The following message was part of a longer message thread between MHProNews and specific media relations contacts at Texas A&M University. This extended quotation is from MHProNews to Texas A&M are the following regarding their Tierra Grande report that is shown further below in its entirety.

“…That said, while there is no specific error with this article, from a professional perspective, it misses the mark. I’ve contacted the TMHA first about our concerns. That’s a separate but related topic.

“…That said, while there is no specific error with this article, from a professional perspective, it misses the mark. I’ve contacted the TMHA first about our concerns. That’s a separate but related topic.

So what’s missing? Here are some examples.

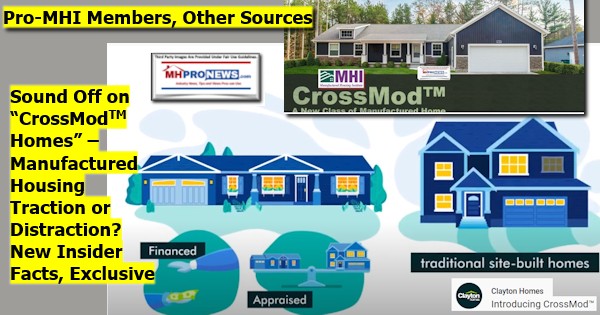

- The entire CrossModTMmove, and its GSE alter-ego names MHAdvantage® and CHOICEhome® are a highly charged topic in our industry.

- The two major national trade associations MHI and MHARR – see this product in entirely different ways. Let’s set that aside, because that’s not entirely uncommon.

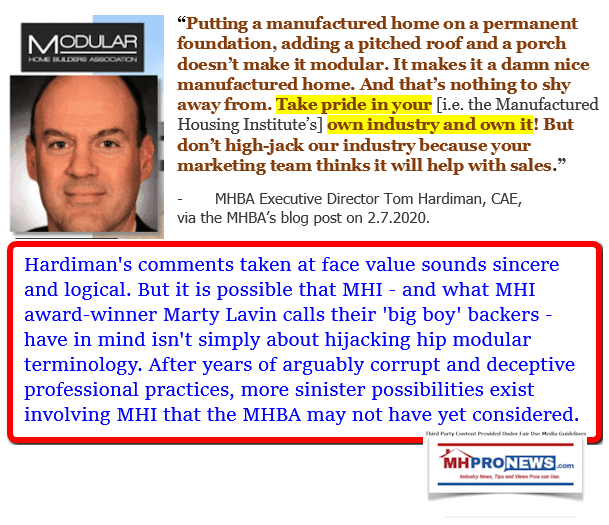

- The Modular Home Builders Association (MHBA) executive director Tom Hardiman normally stays out of manufactured housing industry politics. He publicly ripped MHI and CrossModTM by name. He called it ‘deceptive’ and aptly noted – in our professional view, correctly – that this undermines millions of existing manufactured homes in several respects. Hardiman never told me he did so based on any of our analysis, so I presume he did that all on his own.

- The only reason, MHBA sources tell MHProNews, that Hardiman isn’t still rattling MHI’s cage over CrossModTM is because the product is a market failure. It’s a joke statistically.

- Clayton Homes and MHI have been tight lipped about the data. That said, there is GSE data per the FHFA.

- Who says? GSE data, which reports that in 2 years, they have financed something less than 3 dozen total nationally. The specific data point is on the FHFA website.

- For 2½ years after this program was proclaimed as “momentum” for manufactured housing, industry sales slipped. That did not reverse until the March data, when mainstream housing was so screaming hot, that even the fiasco of CrossModTM could not slow down the surge of mainstream manufactured homes.

- I’ve communicated with Dustin Arp several times. I’m confident your report cited him correctly. But in the light of the above, re-read what was published. Because the sales are knuckles on the ground low.

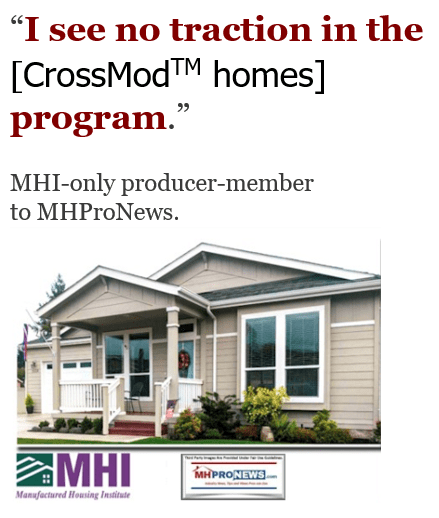

- It gets really political, industry inside baseball, that several MHI member producers have told MHProNews that the product makes no sense, and that there is no traction in the marketplace.

There is more, but that is enough to make this point. If would be hard to have picked a topic that would have been more controversial than this. As noted, your organization’s report is okay, as far as it goes. But it is lacking all of the granular insights above. As numbers of our readers are Texans, I can assure you that numbers are not going to be impressed. That said, those that carry water for MHI and/or Clayton will be fine with this.

Before I take the next steps, I’m keen to get your thoughts on the above. It can be off the record, unless you say otherwise.

You are welcome to share that, or not, with Harold. Please tell him hi for me. This isn’t personal. It is about professionalism and an accurate depiction for our readers of the content.

Last for now. Again, off the record is fine. I’m guessing that no one at MHI or Clayton corporate said anything about this, right or wrong? Because it fits their narrative.

Please do feel free to be candid. Thank you.

Respectfully,

Tony

PS: There is more…” ##

##

A contact at Texas A&M’s media relations said the following in response.

Tony:

I really appreciate the background. I was not aware of any of this. We have a research approval process that is supposed to red flag manuscripts with problems, questions, or in need of more outside comments. Once it clears those hurdles, the communications staff’s job is to present it to our stakeholders. We rarely are involved in the “research methodology.”

Manufactured housing is a topic we have only recently (last few years) dabbled in. Our monthly survey with TMHA is an effort to learn more about this aspect of real estate.

I am sending your note to Harold. He needs to be aware of the background.

When you refer to “the next step on our end,” what’s that in reference to?

I guess our desire to learn more about manufactured housing is on the fast track.

Again, I appreciate the heads-up and candidness.” ##

That same source in media relations reported that Clayton and MHI said nothing in response to the “It’s Real” report by the Tierra Grande article published by RECenter.TAMU.edu. That report is as shown below the second image.

It’s Real

Seguin Welcomes Texas’ First CrossMod Manufactured Housing Development

Harold D. Hunt (Jun 4, 2021)

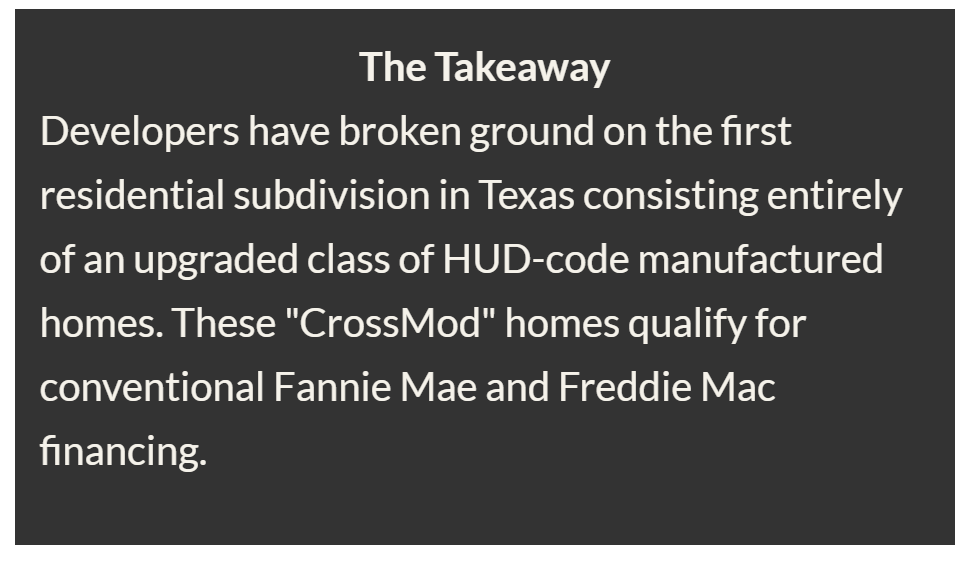

The first residential subdivision in Texas exclusively offering “CrossMod” manufactured homes is currently under development about four miles outside Seguin. CrossMod is the Manufactured Housing Institute’s trademarked name for an upgraded class of national HUD-code manufactured homes (MH). It should not be confused with “modular” homes built to meet a specific local building code.

“The goal for this development is to provide someone with a nice home that they are proud to own in a lower price range than starter homes in a traditional densely developed subdivision,” said Dustin Arp, president of New Braunfels-based Spark Homes LLC, the subdivision’s developer.

traditional densely developed subdivision,” said Dustin Arp, president of New Braunfels-based Spark Homes LLC, the subdivision’s developer.

CrossMods, which are only sold with land as real property, are eligible for financing under the same conventional loan terms as site-built, single-family homes through Fannie Mae and Freddie Mac. The two government-sponsored enterprises (GSEs) teamed up with the manufactured housing industry to develop and finance factory-built housing of similar quality to site-built starter homes but at a more affordable price point. While Fannie Mae has named its mortgage program MH Advantage, Freddie Mac has chosen the name CHOICEHome.

“The GSE loan programs offer a rare opportunity for the MH industry to grow from representing only 9 percent of all new home sales annually,” said Dave Busche, director of business development central region at Skyline Champion Homes. “MH finally has the chance to enter into mainstream homebuilding and really participate in the affordable housing solution.”

“You also need a mix of FHA (Federal Housing Administration) and VA (Veterans Affairs) loan products along with the conventional loans being financed by Fannie and Freddie,” said Arp. “You can’t just offer conventional financing in a development like this. A CrossMod that qualifies under the MH Advantage or CHOICEHome programs can qualify for an FHA or VA loan. It is just less likely to make value on an appraisal, and the interest rate would be higher when compared with site-built homes. But the real difference is about $2,000 to $3,000 in added closing costs from cost surcharges such as points.”

Arp’s least expensive floor plan starts at $185,000 with no options or upgrades. The majority of homes in the development will be priced between $200,000 and $230,000. Lot size is one acre while home sizes range from 1,113 to 1,789 square feet.

“Developers choosing a subdivision model similar to production homebuilding on a typical 1/8-acre lot could probably reduce these prices by about $15,000 to $18,000,” Arp said.

Development Challenges

Demand for factory-built housing in Texas is currently quite strong.

“MH manufacturers are experiencing exceptional backlogs,” said Busche. “If the backlogs continue, the only way to achieve real growth in CrossMod projects is to expand production through new manufacturing plants. But construction of new facilities will be no small task.”

“A big challenge to widespread adoption of CrossMods is going to be sufficient inventory,” Arp said. “If the houses aren’t out there on the ground, consumer acceptance is going to be slow.”

“Two other delay influencers besides backlogs are development timeframes as well as restrictive zoning—’not in my backyard’ issues,” said Busche. “We have four business development managers at Skyline Champion. Each of us is engaged with multiple CrossMod prospects/projects, some for well over a year. Most new projects are just not ready to accept delivery of homes yet.”

Although Texas does not have county zoning ordinances, allowable zoning for all MH, including CrossMods, inside metropolitan areas remains a challenge.

“Acceptance by municipalities is a key topic in every convention I’ve been to,” said Arp. “Most cities start with a base of codes provided to them by consultants that they can adopt and make small changes to. If we could create a new zoning category for CrossMod that cities would accept, that would be a major breakthrough.” To that end, Arp makes it a point to drive as many local city and county officials through the subdivision as possible.

Busche states that only four large MH manufacturers in Texas are currently offering CrossMod homes. Skyline Champion’s Athens, Texas, factory, which is providing the CrossMods for Arp’s development, is one of them. Each of Skyline Champion’s four Texas facilities produces a different mix of factory-built homes, with the Athens factory building modular-coded product as well.

Arp also believes real estate agents have to be made more aware of the existence of CrossMods.

“Most agents don’t know that potential homeowners can obtain an attractive home and lot size by purchasing a CrossMod. Unfortunately, it’s hard for them to get involved until the homes are actually out there and available to show,” he said. “If there were sufficient CrossMod developers, I believe we could provide manufacturers with loads of CrossMod sales.”

Appraisals present another challenge. In December 2020, FHA issued a mortgagee letter recognizing a difference between CrossMod and traditional MH for appraisal purposes. As a result, FHA appraisers may include site-built comparables if fewer than two comparable MH Advantage or CHOICEHome sales are available. This appraisal allowance was already acceptable for conventional GSE financing.

“But just because that mortgagee letter is out there doesn’t mean that an appraiser is aware of it,” Arp said.

Based on his banking experience, Arp uses accepted appraisal adjustments to piece together a comparative market analysis for appraisers. He spends considerable time making sure comparable sales support the required sales price he is targeting.

“If they don’t have the knowledge of how to appraise a CrossMod, then no one can buy these products,” he said.

Developer Skills Affect Affordability

Arp thinks developers who have a more diverse background and skillset will be much more adept at producing the most affordable CrossMod product.

“It’s difficult for any MH developer to be diversified,” he said. “All MH purchases require a retailer’s license, but a retailer generally can’t do the land development. A licensed installer, or a subcontractor working under one, is then responsible for installing the foundation, septic system, and so forth.

“I also believe that if the developer pursues a production homebuilder sales model, with a model home and inventory to show, the product will explain itself. The lower collateral risk that allows Fannie and Freddie to remove cost surcharges such as points stems from the increased marketability of CrossMods. That increased marketability results in higher product acceptance from consumers. I don’t think the industry will ever be successful trying to pursue a scattered-site development model where the home is shown at a MH dealership and sold to be put on a homeowner’s vacant lot. It needs to be shown in the environment in which it will be placed as a finished product.”

Counties also have subdivision regulations that developers must be familiar with.

“An example is sewer treatment,” Arp said. “Unless you want to build a treatment facility, which is a lengthy process with the Texas Commission on Environmental Quality, you will need to be familiar with the state requirement for septic tanks.”

A civil engineer must also be involved in the project to address issues such as drainage and watersheds. Drainage requirements will come from the area’s floodplain administrator who will require an inundation study examining watersheds crossing the property. The civil engineer must come up with a plan to show impact on adjoining neighbors and homeowners.

Arp thinks there doesn’t have to be as much homebuyer education if the product is on the ground to view in person.

“The home will speak for itself,” he said. “If you follow the guidelines, especially frontal elevation to make it look more like a site-built home, product adoption is immediate. The reality is a developer must find the right piece of land in the right configuration at the right price with the right utilities to the site.”

In a 50-mile radius, he might find one piece of land that fits all those requirements.

“It could easily be a year to 18 months from the beginning of this process to selling the first house,” Arp said.

Arp also drew up his own homeowners’ association rules as well as a 60-page builder’s contract.

“We are taking three separate components and, at the time of closing, putting them all together: a garage that is constructed on site, the CrossMod house, and the land,” he said.

Arp notes there are separate disclosures and warranties to be considered.

“The garage technically has a separate warranty from the house,” he said. “The CrossMod manufacturer will warranty the actual house. The foundation has a totally separate warranty as well.”

Not for All Developers

Developing CrossMods won’t be for everyone. Arp summed it up well in a February 25, 2021, podcast for ManufacturedHomes.com.

“Developers are going to want to see my books,” he said. “They have all done their own proformas, modeling, and market research. However, unless they identify some of the key efficiencies not currently being exploited by MH retailers pursuing a scattered-site model, CrossMod just won’t make sense.

“The key here is to build a product that is visually competitive with an entry level site-built house that remains as affordable as possible. When you exit the affordable segment, you lose that market share where MH could triple the size of the industry in the next six or seven years with enough market participants. You can’t be a horizontal developer/land man who wants to outsource everything and then participate in the affordable sector.”

Arp believes developers will have to get creative to develop the right efficiencies.

“Some of the savings have to be passed on to the consumer,” he said. “We will probably have to offer the buyer an 8 to 10 percent savings over the site-built homes being offered by production homebuilders to initially gain wide acceptance of CrossMods.” ##

Their article closes with this brief bio that says that Dr. Hunt “is a research economist with the Texas Real Estate Research Center at Texas A&M University.”

##

MHProNews Analysis & Commentary

Dr. Hunt’s report has several interesting and useful revelations. In no particular order of importance:

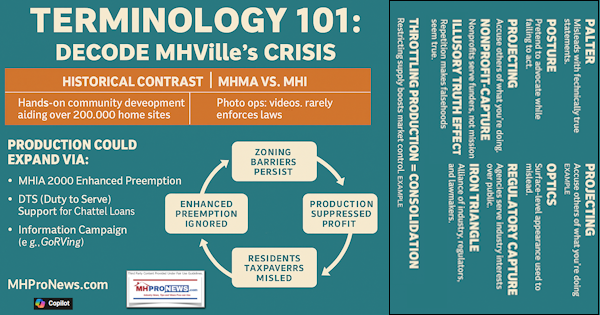

- What is not stated is that CrossModTM has been pitched by MHI as a product that is supposed to be able to penetrate the zoning/placement barriers encountered by mainstream HUD Code manufactured homes. Additionally, the financing advantages that MHI and its CrossMods backers claims is shown to be illusory. Let’s examine these concerns in more detail.

- Arp’s development is not urban. Rather, it is a more rural location.

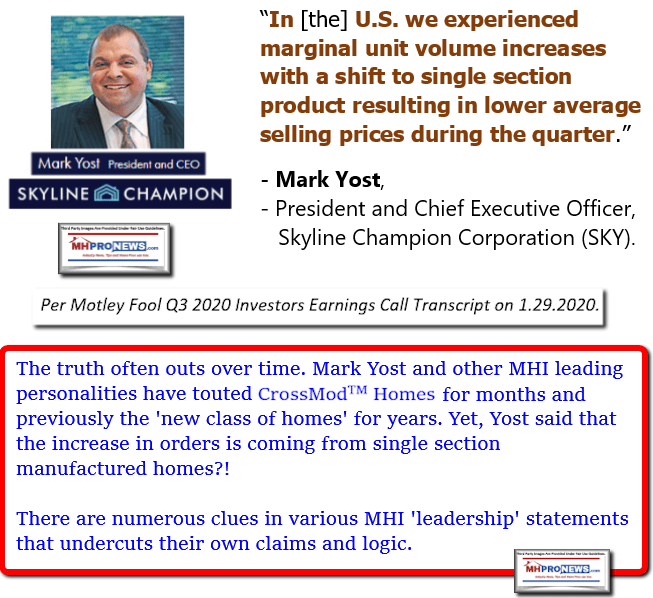

- While the report gives no data on unit sales – how many (or few) of these ‘new class of manufactured homes’ that are being sold, it does suggest that the sales are low. While framing it differently, Arp has said as much to MHProNews. This has not yet proven to be be a high-volume or ‘production’ type of product. Rather, it has been a low-volume seller.

- Ironically, Dr. Hunt’s report quotes Arp in a manner that arguably debunks much of the supposed logic for this ‘new class of manufactured homes’ later rebranded as CrossMods.

- Quoting: “You also need a mix of FHA (Federal Housing Administration) and VA (Veterans Affairs) loan products along with the conventional loans being financed by Fannie and Freddie,” said Arp. “You can’t just offer conventional financing in a development like this. A CrossMod that qualifies under the MH Advantage or CHOICEHome programs can qualify for an FHA or VA loan. It is just less likely to make value on an appraisal, and the interest rate would be higher when compared with site-built homes…”

- It must be stressed, as numbers of retailers know, that mainstream HUD Code manufactured homes have long ago qualified for FHA Title I (home-only) and Title II (land-home) financing that Arp mentioned. Additionally, mainstream HUD Code manufactured homes already qualified for VA and USDA/Rural Development financing on land-home packages.

- Rephrased, some of the very claims made by MHI and their backers – per Arp and Hunt – have been debunked in an article that is supposed to tout the “It’s Real” hype.

- It is troubling that reportedly no one at TMHA, MHI, or Clayton revealed any of the controversies to Hunt, per informed sources that produced the Tierra Grade report for their university.

- The low-volume nature of this product reveals just how misleading and errant MHI’s claims have been.

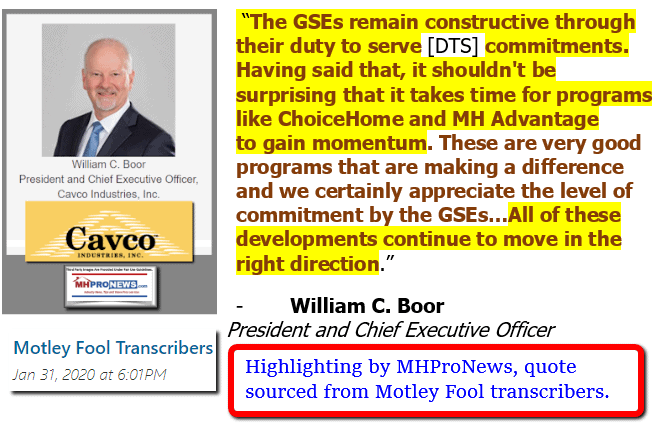

- That low volume is apparently so low that a DTS comment on the FHFA website by a professional advocate – that is being explored for accuracy – claims that the GSEs are dropping the product. If so, there is no other such known indication at this time.

- That comment is by George McCarthy with the Lincoln Institute of Land Policy. McCarthy stated: “Activities that were highly touted over the last three years – including the MH Advantage and MH Choice products, as well as chattel pilots – have been dropped with little or no explanation.”

- Note that McCarthy should have said CHOICEhome®, which is the Fannie Mae branded version of CrossModTM. Fannie’s version is dubbed MHAdvantage®. Typos aside, McCarthy’s point with respect to chattel pilots is quite apt. Indeed, Pew Research DTS comments note that there is a lack of transparency in the process. Quite so. Phil Schulte, in his DTS comments, made a similar point. See that as part of the deep dive report linked below.

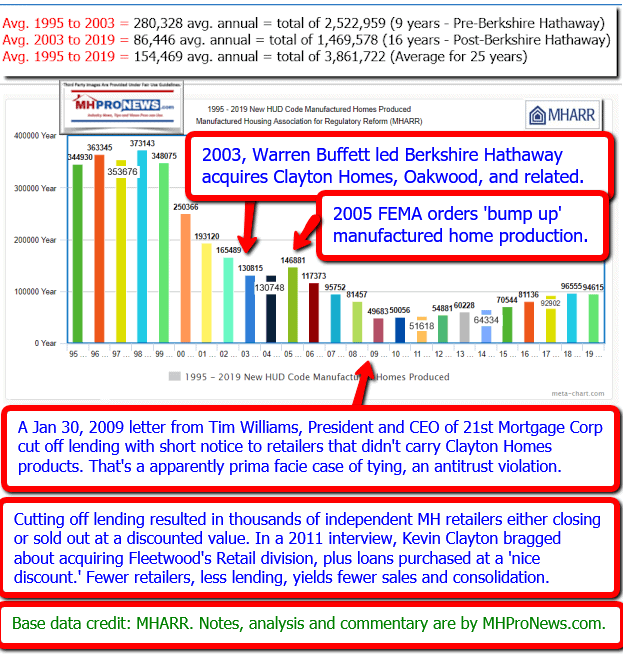

- During most of the 2½ years following MHI’s declaration of “momentum” that accompanied what McCarthy quite rightly called “highly touted products over the last three years” – instead turned out to be a well documented slide in new HUD Code manufactured home sales.

- Rephrased, instead of growing sales, this CrossMods product line has factually associated with a decline in sales during an affordable housing crisis.

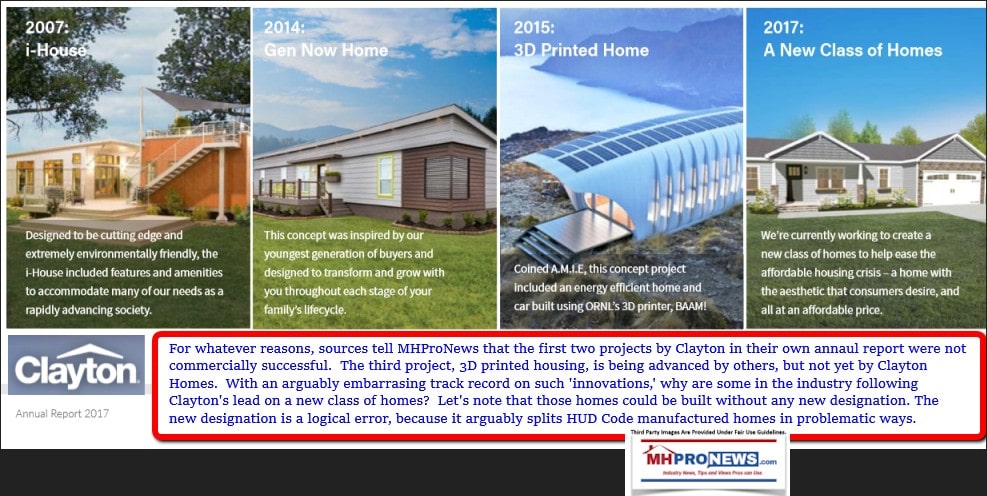

- Almost unmentioned by MHI, Clayton, or others beside MHProNews is that Clayton has had previously tested more expensive models before. They were each pulled from their production line-up for lack of sales, per sources inside Clayton to The CrossModTM/”new class of manufactured homes” appears headed in that direction.

- Also largely ignored is a point that MHProNews, MHLivingNews and Pew Research – via a footnoted reference – has repeatedly made. Namely, that HUD research during the Obama-Biden Administration revealed that manufactured homes cited in neighborhoods along side conventional housing revealed that both appreciated side-by-side. Given the far greater savings with such products, why were CrossMods launched at all?

- Indeed, there are years of more upscale HUD Code manufactured homes long before CrossMods. Because they had far more market success, why didn’t MHI press harder for DTS credits on those? Along with all other HUD Code manufactured homes?

- Not to be overlooked is an analysis by an MHI member producer that told MHProNews that CrossMods ‘do not pencil out.’ That source said that when the added costs for CrossMods are considered, the savings in finance rates does not offset the added costs associated with the product and its financing. If so, that’s a major oversight that may shed light on why the sales have been so low.

- The real takeaway from this? Thanks to Dr. Hunt’s report, coupled with the additional factual information and evidence noted and linked, the folly of CrossMods have been completely exposed. Hunt + MHBA + MHARR + MHProNews/MHLivingNews research yields the full range of reasons why this product does not merit any more time or attention by MHI. Rather, MHI should be putting its efforts into supporting mainstream manufactured homes. That fits what Kevin Clayton said at an MHI gathering, ‘you dance with the one that brought you,’ namely, affordable manufactured homes. Anything else fits the argument by for “sabotaging monopolies” – see that by Minneapolis Federal Reserve and other economic researchers, plus more – in the reports links below.

- As noted, further insights on this topic can be found in the quotes and reports linked below. But the bottom line is this. As MHProNews reported in 2018 and several times since, the logic and much ballyhooed claims about CrossMods have never materialized. That helps explain why other trade media that are in the MHI ‘amen’ corner have not called this out for what it appears to be. A Trojan Horse that Clayton and a few big brands can afford to have as a diversion, but that arguably harms the bulk of mainstream manufactured homes.

Part II.

This segment provides the comments submitted by MHI CEO Lesli Gooch, Ph.D., to the FHFA which may – on the surface – appear to be one of her strongest yet.

- However, what Gooch did not mention, as reflected by prior statements by Kevin Clayton, Doug Ryan, Mark Weiss, and MHI itself are going to reveal what could be a case study in paltering within the manufactured housing industry. More on that in our analysis that follows her comments.

July 16, 2021

Ms. Sandra Thompson

Acting Director

Federal Housing Finance Agency

400 7th Street SW

Washington, D.C. 20219

Re: Request for Input – Fannie Mae and Freddie Mac Proposed 2022-2024 Duty to Serve Plans

Dear Acting Director Thompson:

The Manufactured Housing Institute (MHI) is pleased to provide comments in response to the Federal Housing Finance Agency’s (FHFA) request for input about the proposed 2022-2024 Duty to Serve Plans of Fannie Mae and Freddie Mac (the “Enterprises”).

The essence of the statutory Duty to Serve (DTS) requirements on Fannie Mae or Freddie Mac is not plans, reports, or listening sessions, however informative or well-intentioned. The essence of DTS is performance – as measured by the purchase of loans, innovations in product developments, and outreach to qualified seller-servicers. It is in that context, with three years of uneven manufactured home DTS performance to date, that MHI requests that Fannie Mae and Freddie Mac substantially beef up their proposed 2022-2024 DTS Manufactured Housing Plans, to include objectives and commitments to:

- Expeditiously develop a flow program for the purchase and securitization of chattel loans and begin purchase of chattel loans under such a flow program.

- Increase numerical targets for purchase of manufactured home real estate loans, based on a four percent annual increase over the most recent appropriate baseline year.

- Continue to develop innovative programs, such as loans for CrossMod homes.

About the Manufactured Housing Institute

The Manufactured Housing Institute (MHI) is the only national trade association that represents every segment of the factory-built housing industry. Our members include home builders, suppliers, retail sellers, lenders, installers, community owners, community operators, and others who serve the industry, as well as 48 affiliated state organizations. In 2020, our industry produced nearly 95,000 homes, accounting for approximately nine percent of new single-family home starts. These homes are produced by 33 U.S. corporations in 133 plants located across the country. MHI’s members are responsible for close to 85 percent of the manufactured homes produced each year.

Manufactured housing is the largest form of unsubsidized affordable housing in the U.S. and the only type of housing built to a federal construction and safety standard. It is also the only type of housing that Congress recognizes as having a vital role in meeting America’s housing needs as a significant source for affordable homeownership accessible to all Americans. Today, 22 million people live in manufactured housing.

Real Property Manufactured Housing Loans

Purchases of real property manufactured home loans continue to represent the major source of the Enterprises’ mortgage access to credit for manufactured housing.

Fannie Mae’s 2022-2044 DTS Plans include targets to purchase:

- 8,595 real property manufactured home loans in 2022. 9,025 real property manufactured home loans in 2023.

- 9,471 real property manufactured home loans in 2024.

Fannie Mae’s DTS Plan characterizes these levels as a steady five percent a year increase – but only by comparing these levels to an artificially low baseline of the three-year 2018-2020 average. In fact, the 2022 numerical target of 8,595 loans is 2.3 percent below the 2020 level of 8,798.

Therefore, MHI recommends that Fannie Mae revise these targets upward. Using a lower four percent annual increase but basing this off of the 2020 levels as a baseline, the targets would be:

- 9,516 real property manufactured home loans in 2022.

- 9,897 real property manufactured home loans in 2023.

- 10,293 real property manufactured home loans in 2024.

Freddie Mac’s 2022-2044 DTS Plans include targets to purchase:

- 4,300 to 4,800 real property manufactured home loans in 2022. 4,400 to 4,900 real property manufactured home loans in 2023.

- 4,500 to 5,000 real property manufactured home loans in 2024.

Freddie Mac’s 2020 total of 6,634 is a significant jump from its 2019 level of 4,390. Under a more conservative approach using the 2019 level as a baseline, with a similar methodology of an annual increase of four percent, MHI recommends the following targets for Freddie Mac:

- 4,938 real property manufactured home loans in 2022. 5,136 real property manufactured home loans in 2023.

- 5,341 real property manufactured home loans in 2024.

Product Innovation and Lender Outreach

Both Fannie Mae’s and Freddie Mac’s 2018-2020 DTS Plans promised to develop more flexible, innovative loan products for real property loans, and we believe on balance that they succeeded in this objective over the last 3+ years. MHI is particularly pleased that both Enterprises have introduced new programs that provide conventional financing for manufactured homes with site-built features. Qualifying home features for the MH Advantage® and CHOICEHome® programs align closely with the industry’s new CrossMod homes, with higher roof pitches, permanent and lower profile foundations, garages or carports, and porches. CrossMod homes are indistinguishable from site-built housing at a fraction of the cost due to the efficiencies of factory- built construction.

CrossMod homes are a point of entry for home buyers who are currently priced out of homeownership because traditional site-built housing is not produced below $200,000. CrossMod homes will serve this gap in the market and have the potential to reach areas of the country where manufactured housing has, in the past, been zoned out by discriminatory land use regulations at the state and local level. MHI commends the Enterprises for their leadership in this area, which we hope will be a model for similar actions for the FHA Title II loan program to serve CrossMod homes.

MHI encourages Fannie Mae and Freddie Mac to continue these efforts and improve outreach regarding appraisals to ensure appraisers actually know about and follow the new appraisal guidelines for homes that qualify for MH Advantage® and CHOICEHome®. The Enterprises could also develop a functional solution that seamlessly fits into the lender and underwriting process, such as a form that provides appraisers with very specific instructions and guidelines. Such actions would be pursuant to the Duty to Serve statutory requirement for the Enterprises to conduct “outreach to qualified loan sellers and other market participants.”

Finally, MHI also urges the Enterprises to provide further support on certain challenges the industry has seen in developing this new product, specifically with respect to zoning, appraisal, and engagement issues. For example, we encourage the Enterprises to create a strategy for overcoming local zoning and land use barriers to the placement of this new type of home. Such a strategy could include the development of materials for zoning presentations, educational materials, and relationship building with local governments and entities.

Loans to Manufactured Home Communities

Finally, there has been much discussion about the Enterprises’ support for the purchase of land-lease communities, both within and outside of the DTS. Land-lease communities offer more than affordable housing. They offer a sense of neighborhood and often feature a range of amenities. MHI conducted a national survey of people living in manufactured housing, which showed that 87 percent of residents in all-age communities are satisfied with their homes.

MHI understands some parties have raised concerns about some bad actors raising rents excessively and otherwise acting in bad faith. Raising rents and evicting tenants is counter to the prevailing business model of every professional land-lease community owner-operator who relies upon stable rent and high occupancy. Recently, MHI completed a robust, independent analysis of the professionally owned manufactured home community industry to move away from anecdotal cases and understand the real operating conditions, investment/maintenance activities and typical outcomes of residents in these communities. An independent consulting firm was hired and completed a comprehensive research and analytical study across well over 700 respondent residents and over 1,000 professionally managed community’s operation data.

The independent research affirms the following:

- Residents in professionally managed communities’ value their community management and its extensive offering of amenities and ongoing investment.

- Professionally managed communities consistently improve and routinely make investments in their communities each year – enhancing near-term and long-term value of the community.

- Lease rates are competitive, and rent increases are at par or lower than other housing alternatives.

Going back many years, MHI worked with consumer groups and proposed standards for consumer lease protections through the DTS process. Our intent was for such protections to accompany secondary market support for the financing of homes within land-lease communities (chattel financing) as opposed to the commercial financing of the communities themselves, which is how the protections were ultimately adopted within DTS. We have consistently argued that the DTS credit should be specifically targeted to supporting financing for the consumer and we encourage FHFA to move the Enterprises back to a consumer focus when it comes to their activities under DTS. While we appreciate the Enterprises’ support for land-lease manufactured housing communities and hope such support will continue, within DTS we strongly encourage a concerted focus on creating a secondary market for chattel financing so that residents in the land-lease communities can be supported.

In conclusion, MHI appreciates the efforts by FHFA, Fannie Mae and Freddie Mac with respect to manufactured housing. MHI is committed to working with FHFA and the Enterprises to expand the supply of affordable manufactured housing in a responsible manner. We believe that these recommendations will bring to the manufactured housing consumer many of the same benefits available to consumers with conventional mortgages, namely greater access to credit with potentially more affordable financing, more lenders in the market, and the ability to refinance as market conditions change. We welcome the opportunity to address any questions or concerns you might have, and stand ready to continue to work with the Enterprises and the FHFA in helping to implement a successful and impactful Duty to Serve program for manufactured housing.

Thank you for consideration of these recommendations.

Sincerely,

Lesli Gooch, Ph.D.

Chief Executive Officer ##

###

More Information, MHProNews Analysis, and Commentary

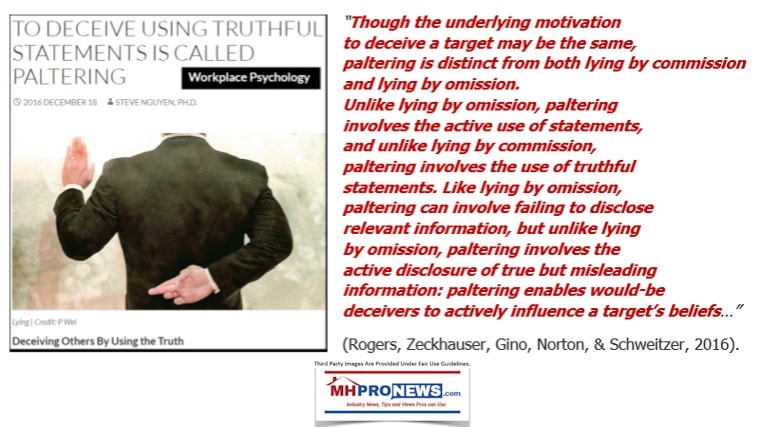

There are statements that on the surface may be true, but when they omit other relevant facts, can be deceptive. That is described by some as “paltering.” The Capital Research Center has referred to what they call “deception and misdirection.” One could write a chapter on what is missing in emphasis, importance, and information from Gooch’s missive above. But we will do so more expeditiously by linking up several documents, and use a series of bullets to reveal in rapid fire manner just how woefully lacking Gooch’s comments are.

In no particular order of importance are the following.

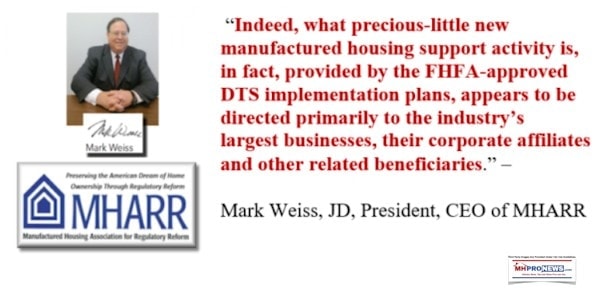

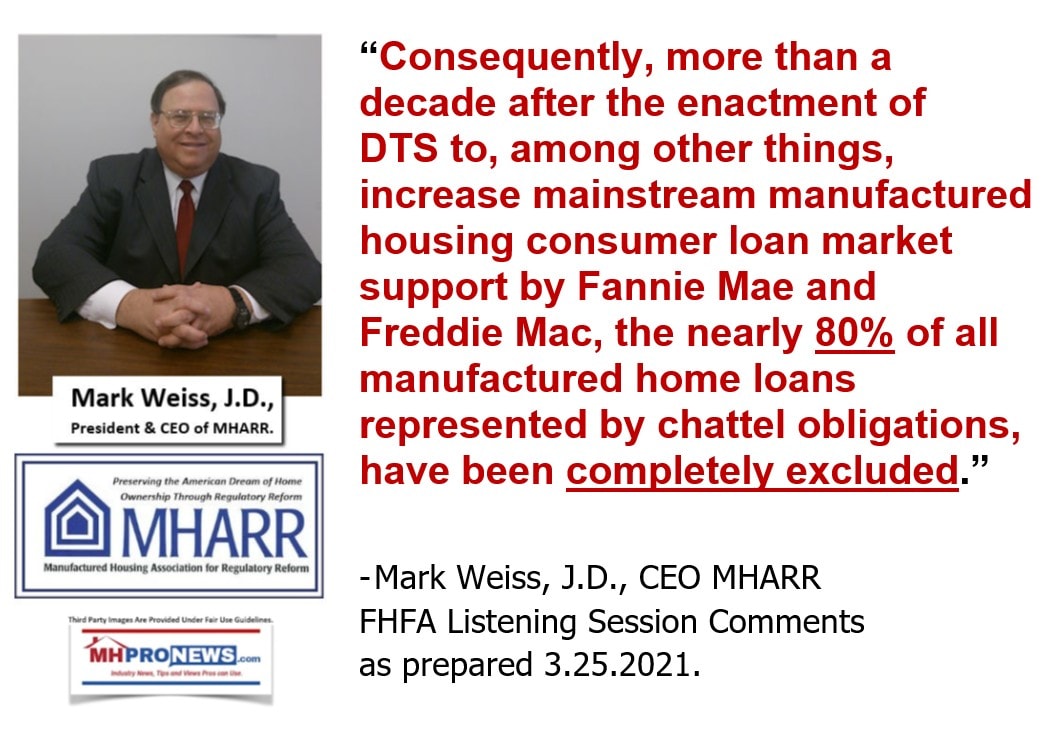

A) It goes almost without saying that the Manufactured Housing Association for Regulatory Reform (MHARR) has early and often ripped this misdirection of the Duty to Serve away from mainstream manufactured homes. For example, MHARR’s President and CEO Mark Weiss pointed out the obvious. Fannie and Freddie were embracing a product that had no track record, vs. supporting the multiple decades of experiencing for mainstream manufactured homes.

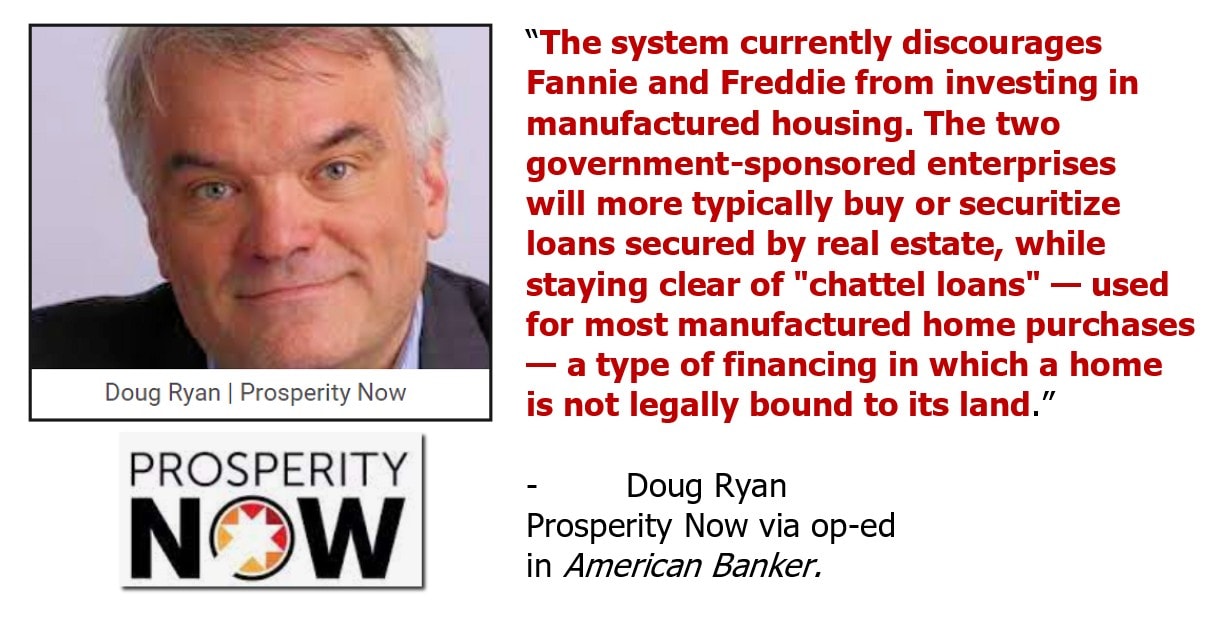

B) But some who are wrongly tempted to discount Weiss, for whatever reason, then can’t ignore an array of other voices outside of MHARR. For instance, Prosperity Now’s Doug Ryan slammed MHI and Clayton for undermining the process of providing chattel lending support for mainstream HUD Code manufactured homes.

Doug Ryan with Prosperity Now in his DTS comments letter uploaded to the FHFA on 7.17.2021 said the following.

“Chattel Loans

Chattel loans account for most loans for manufactured home buyers. We are disappointed, but not surprised, that the enterprises do not, and for 2021, will not, have chattel products. While community development financial institutions and a handful of state HFAs do great work in the chattel space, the GSEs’ entry into this market is the one viable way to reduce homeowner expenses, improve consumer protections and advance asset building.”

Ryan added, “The 2019 reports on chattel products for both enterprises noted that they were on track in product development. Events in 2020, as detailed in their plans for 2021, suggest this is no longer the case. Both the enterprises and their regulator must detail the challenges in product development, including any market opposition, and their plans to advance such products.”

That appears to be an oblique reference to Ryan’s comments cited above and below.

C) What Gooch completely ignored are powerful statements like the ones below that reveal that there are no excuses for not providing lending on all HUD Code manufactured homes via DTS, including chattel (home only) loans.

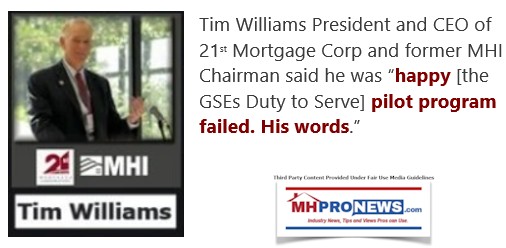

Additionally, and to the concerns raised by Weiss, Ryan, and others cited and linked herein, Good entirely failed to mention the celebratory mood of former MHI chairman, and still MHI board member, Tim Williams. Williams is the President and CEO of 21st Mortgage Corporation, a Berkshire Hathaway owned brand that is a sister company to Clayton Homes.

D) Reports linked below unpack the issue from an array of perspectives.

The bottom line is that MHI has been demonstrably posturing on DTS – and other issues, such as zoning and placement – without doing much that is measurable. Some of their affiliates and members have at various times made observations that support such concerns, as a few examples below and in linked reports illustrate. But that does not mean that silently or subtlety, some MHI affiliates and members are quietly calling out what is and has been occurring.

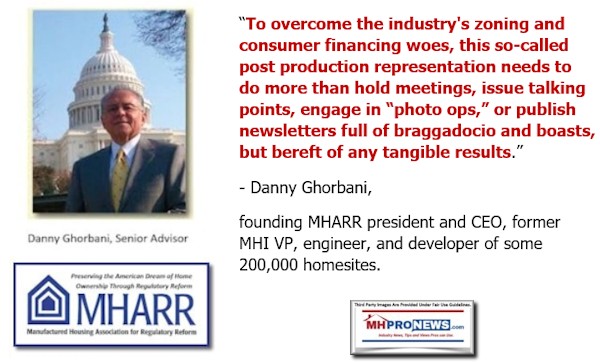

MHARR’s Danny Ghorbani summed much of that up with these stinging but apt words.

Examples of relevant reports on financing related topics and/or issues that illustrate the harmful impact of a lack of more competitive lending that routinely connect to the Duty to Serve and purported MHI failures are linked below.

No Title

No Description

Part III. Weaponized Information and Agenda-Driven Reporting – Illustrated by Comments from Journalists, Academics, Federal, and Communications Professionals

From the political left and right there is a growing number of voices that have spoken out about what Edelman called an “infodemic.” On the one hand, this is hardly ‘new.’ So-called yellow journalism period, per history.state.gov was from 1866-1898. “Yellow journalism was a style of newspaper reporting that emphasized sensationalism over facts.” That period in American history is worth a a brief segue in order to learn the lesson and then return to this topic at hand.

In an article on the federal website entitled “U.S. Diplomacy and Yellow Journalism, 1895–1898” the article states that “During its heyday in the late 19th century it was one of many factors that helped push the United States and Spain into war in Cuba and the Philippines, leading to the acquisition of overseas territory by the United States.”

Students of history should peer into the Spanish-American War in order to better understand what occurred in the run-up of U.S. involvement in conflicts such as World War I, World War II, Vietnam, and the U.S. conflicts in the Middle East under Presidents George H.W. Bush, George W. Bush, and Barack Obama. Because even though history doesn’t precisely repeat, as the saying goes, it does rhyme.

Or more aptly, whatever has happened before can happen again.

Per the history.state.gov website: “On the night of February 15, an explosion tore through the ship’s hull, and the Maine went down. Sober observers and an initial report by the colonial government of Cuba concluded that the explosion had occurred on board, but Hearst and Pulitzer, who had for several years been selling papers by fanning anti-Spanish public opinion in the United States, published rumors of plots to sink the ship. When a U.S. naval investigation later stated that the explosion had come from a mine in the harbor, the proponents of yellow journalism seized upon it and called for war. By early May, the Spanish-American War had begun.”

“The rise of yellow journalism helped to create a climate conducive to the outbreak of international conflict and the expansion of U.S. influence overseas, but it did not by itself cause the war. In spite of Hearst’s often quoted statement—“You furnish the pictures, I’ll provide the war!”—other factors played a greater role in leading to the outbreak of war. The papers did not create anti-Spanish sentiments out of thin air, nor did the publishers fabricate the events to which the U.S. public and politicians reacted so strongly. Moreover, influential figures such as Theodore Roosevelt led a drive for U.S. overseas expansion that had been gaining strength since the 1880s. Nevertheless, yellow journalism of this period is significant to the history of U.S. foreign relations in that its centrality to the history of the Spanish American War shows that the press had the power to capture the attention of a large readership and to influence public reaction to international events. The dramatic style of yellow journalism contributed to creating public support for the Spanish-American War, a war that would ultimately expand the global reach of the United States.” What where the other factors that history.state.gov does not mention? Conflicts often produce to certain benefits that routine go to big business interests. That is undoubtedly a factor in the Spanish-American War and other conflicts too. So it is interesting that the State Department makes such an admission.

With that historic lesson in mind, fast forward to today.

In response to this question from Newsmax on 7.16.2921 at about the 4:39 mark: “Why Is no one but John Solomon reporting on this? If this was Trump, it would be everyone. And yet you have now a top FBI agent basically saying unequivocally, yes. Where’s the rest of the press corps?”

The question itself reflects hype, as Solomon is hardly alone on this. That noted, to reframe that – it is an important inquiry – why have so few reporters dug into obvious issues related to Hunter Biden and other Biden-family connected scandals?

This was award winning journalist John Solomon’s reply.

“Well, they’ve [much of mainstream media] been AWOL for five or six years… let’s be honest about it…I think we grew up an entire new generation of journalists and have become causal journalists. They don’t look at the facts… [They] try to come up with the story and then fit the facts into it…It is a phenomenon that deeply troubles me. I was attacked, relentlessly smeared after a 30 year stellar career. We’re having won almost every journalism [award]…you can think of. [I] was smeared relentlessly for…reporting on Hunter, Biden, and Burisma. Every fact that i reported not only has stood the test of time it’s been confirmed by lawsuits and revelations and the information on this. [Much of] American media have decided not one question.”

There is not much hubris or hyperbole in Solomon’s statement.

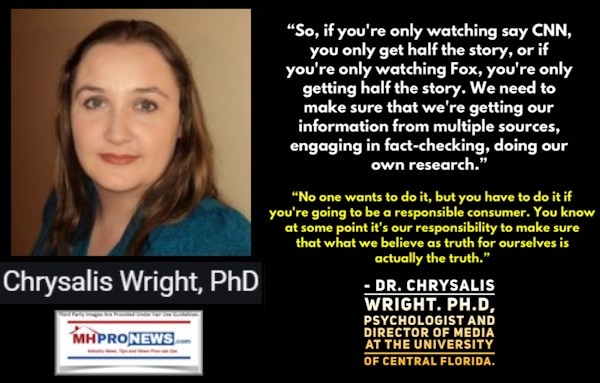

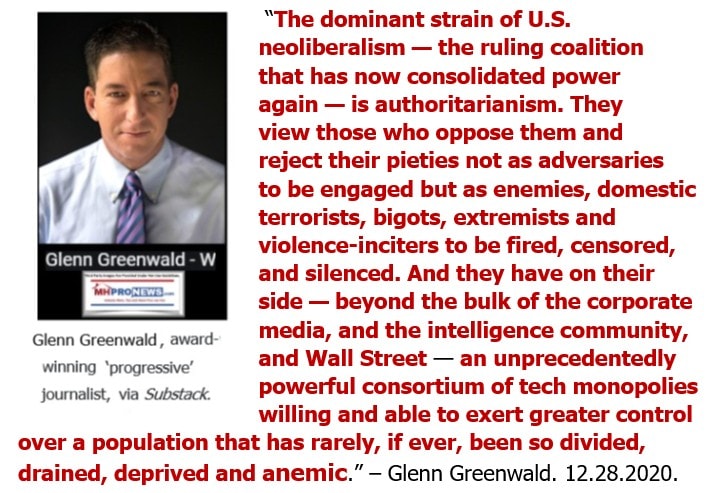

Dr. Wright, referenced above, shed light on that in a discussion on modern media where she said the follow.

Voices from the mainstream media, often from the political left, have called out the attempts to muzzle or sideline the truth because it is inconvenient.

When someone wonders why our industry could be suffering such low levels of sales during an affordable housing crisis, several factors are involved. Access to competitive financing is one of them, and that is the focus of this report. Certainly zoning/placement, mentioned in passing above, is another one. But a third element is the what Edelman aptly called an Infodemic. More appropriately perhaps was Danny Glover’s repeatedly referenced by this publication’s statement that there is a monopoly on information and capital access.

Glover is not only a well-known actor. He has also sat for some time on one of the Buffett nonprofit boards. He has doubtlessly seen up close the impact of information, entertainment, and capital access in the process of the steady monopolizing of the U.S.A.

That such monopolization is occurring is hardly debatable. Joe Biden has spoken of the threat himself, though he argument is posturing too. But if Biden meant what he said, then DTS and more would be a reality on chattel lending. Instead, it is likely to be largely an illusion that will routinely benefit Biden backers. It may not be a shock of the FHFA nudged the GSEs into a few tweaks on their announced plan. But tweaks aren’t what is needed. It is a robust implementation of the law that is required.

There is a quilt-work of issues that interconnect that have brought manufactured housing to its current low point. Our industry is hardly alone on this pattern of monopolization. That said, as a manufactured home industry trade publication, we need to look at the big picture as well as the more industry specific ways that big picture is playing out.

While it is true that the manufactured home industry has ‘recovered’ from its 2009 and 2010 bottom, it is perhaps operating at only 30 percent of its prior high. Without looking carefully into these issues – finance, the history of who said and did what, and the manipulation or ignoring of various laws – it is simply not possible to truly understand the current state of the industry.

It is not always easy to get someone to read a longer article once, much less twice or three times. But experience has shown that absent such an effort – when sound factual and evidence-based information are available – truly understanding what has and is occurring in affordable housing and manufactured housing more specifically will prove to be elusive. Indeed, many do not want to know what has gone wrong. Because some believe that they are benefiting from the status quo.

Nevertheless, this is why Attkisson’s adage of “check your facts” and “follow the money” trail make so much sense. Cui bono? Who benefits? That has been any serious investigator’s question for seeking and finding the truth of a topic. When paltering and spin are often used, sorting out facts from mere spin is necessary.

The reality is that the lack of clarity and accuracy in reporting by most on this subject is a contributing factor to the status quo. If the truth was widely known and well understood, then the stubborn way the FHFA, GSEs, and their beneficiaries would not have been able to get away with ignoring and twisting the law for so long.

Just as disinformation artists continue to spin and palter, truth tellers must do the same. Those who are sincere about giving those with lower incomes or who otherwise want more affordable housing have to get granular in order to see what becomes almost self-evident with several readings of such reports.

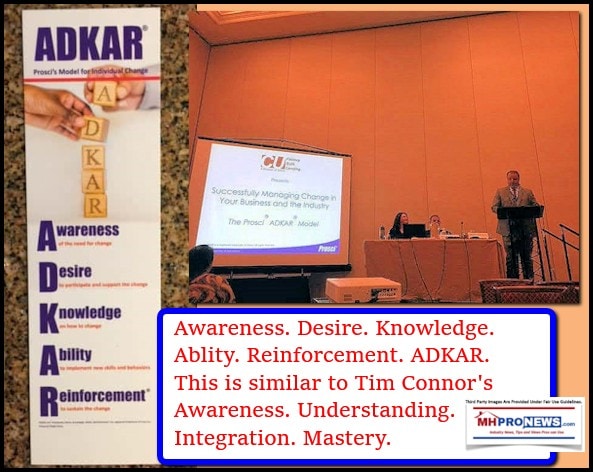

There are levels of understanding and knowledge. ADKAR describes that process. Tim Connor’s 4 levels of learning does too.

Without a sound understanding of the truth of these issues their proper resolution will be illusory. Some want that Infodemic. It is only those who sincerely want to benefit the greatest number of Americans from all walks of life that will be willing to probe, consider, and the read and re-read these topics until the bright light of truth is shining. Only the truth and good will can set the captives free. ##

[cp_popup display=”inline” style_id=”139941″ step_id = “1”][/cp_popup]

Notice to MHI members. Follow up emails to several MHI linked attorneys – not one disputed the claim by the law firm cited in the report below. MHI has demonstrably created an ‘amen corner,’ an echo chamber that parrots their talking points. MHI and those involved have not denied that evidence-based allegation. But as, or perhaps more important, is this below. For those MHI members who are aware of what is occurring, but who fail to stand up or speak up in some form or fashion, legal experts say that it could make those members vulnerable to legal action, just as MHI is. To learn more, see the related report linked below.

The evidence routinely points one way. No wonder why MHI, their major brands, and even their outside attorneys all went silent when it comes to engaging with MHProNews on these troubling trends and growing evidence.

Stay tuned for more of what is ‘behind the curtains’ as well as what is obvious and in your face reports. It is all here, at the runaway largest and most-read source for authentic manufactured home “News through the lens of manufactured homes and factory-built housing” © where “We Provide, You Decide.” © ## (Affordable housing, manufactured homes, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.) (See Related Reports, further below. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHProNews.com.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing.

For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com.

This article reflects the LLC’s and/or the writer’s position, and may or may not reflect the views of sponsors or supporters.

Connect on LinkedIn: http://www.linkedin.com/in/latonykovach

Related References:

The text/image boxes below are linked to other reports, which can be accessed by clicking on them.

{kind=link}