There is an evidence-based case to be made that William C. “Bill” Boor, the president, CEO & a director at publicly traded Cavco Industries, Inc. (NASDAQ:CVCO) and his firm has created competing narratives. One narrative is for investors. Another is for the industry and public. While there may at times appear to be overlaps in these remarks, there are apparent contradictions too that will be explored in Part II of this MHVille facts-evidence-analysis. Part I of this report will include the transcript of the latest Cavco earnings call via Seeking Alpha (SA), made available below under fair use guidelines for media. Earnings calls transcripts are relevant to SEC or other issues related to materiality. Earnings calls matter. The remarks by Boor and his colleagues are supposed to be factually accurate at the time those remarks were made.

Due in good measure to remarks made by Bill Boor, this report may be one of the more revealing on the subject of cautionary or red flags regarding what appears to be ongoing antitrust violations that involve Cavco Industries (CVCO) along with other Manufactured Housing Institute (MHI) members. Boor is currently MHI’s chairman.

So, among the topics that will be considered in Part II is antitrust law. To set the stage, many legal observers are striving to read the tea leaves for antitrust enforcement under Trump 2.0. Among them is this one from the National Law Review.

The Trump Administration Dismantles California’s “Clean Truck Partnership” Through the Use of Antitrust Law

This action by the FTC is part of a broader effort by the Trump Administration to overturn environmental regulations enacted by Democratic governments (whether state or federal), and generally to pursue a rollback of various ESG initiatives, especially those concerned with climate change. It also reflects the tactical choice by the Trump Administration, and Republican state governments across the United States, to employ antitrust law as a means to attack various agreements among industry participants to adopt collective solutions to address climate change. Their success here will likely prompt additional efforts along the same lines.

Some observers are saying Trump 2.0 is going easy on apparent antitrust violators. Others are less certain.

Routinely left-leaning Trump critic and antitrust advocate via BIG, Matt Stoller, said the following. Bold is added for emphasis by MHProNews.

Some of the news of the week includes a child sex scandal revealed at the NFL Players Association, Ticketmaster got humiliated in Maine, and new data was released showing it’s increasingly hard for big business to find jurors who don’t hate corporations.

That bold-for-emphasis remark should not be a surprise. MHProNews has previously reported that antitrust support is high among both Democratic and Republican voters.

As MHProNews has previously reported, there are evidence-based reasons to believe Cavco is engaged in a multi-year effort that appears to violate antitrust law and involves other Manufactured Housing Institute (MHI) members. More on that in Part II.

With those notions in mind, it is a good time to pivot from this preface into some housekeeping items prior to the Cavco Industries Q1 2026 Earnings Call Transcript.

Highlighting in what follows is added by MHProNews. Highlighting should not deter readers to ignore or downplay other parts of the SA transcript. Minor edits of SA’s transcript (spacing errors, for example) are by MHProNews, but have not changed the meaning of the words as shown.

The commentary should be considered in part through the lens of the recently (8.7.2025) published report on Cavco’s financials, linked here.

Part I

Cavco Industries, Inc. (CVCO) Q1 2026 Earnings Call Transcript

Aug. 01, 2025 8:34 PM ETCavco Industries, Inc. (CVCO) Stock

Cavco Industries, Inc. (NASDAQ:CVCO) Q1 2026 Earnings Conference Call August 1, 2025 1:00 PM ET

Company Participants

Allison K. Aden – Executive VP, CFO & Treasurer

Mark Fusler – Director of Financial Reporting & Investor Relations

Paul W. Bigbee – Chief Accounting Officer

William C. Boor – President, CEO & Director

Conference Call Participants

Daniel Joseph Moore – CJS Securities, Inc.

Gregory William Palm – Craig-Hallum Capital Group LLC, Research Division

Jay McCanless – Wedbush Securities Inc., Research Division

Jesse T. Lederman – Zelman & Associates LLC

John Dundee Lapey – Gabelli Funds, LLC

Operator

Good day, and welcome to the First Quarter Fiscal Year 2026 Cavco Industries, Inc. Earnings Call Webcast.

[Operator Instructions] As a reminder, this call may be recorded. I would now like to turn the call over to Mark Fusler, Corporate Controller, Head of Investor Relations. Please go ahead.

Mark Fusler

Good day, and thank you for joining us for Cavco Industries First Quarter Fiscal Year 2026 Earnings Conference Call.

During this call, you’ll be hearing from Bill Boor, President and Chief Executive Officer; Allison Aden, Executive Vice President and Chief Financial Officer; and Paul Bigbee, Chief Accounting Officer.

Before we begin, we’d like to remind you that the comments made during this conference call by management may contain forward-looking statements. Forward-looking statements include statements about our expected future business and financial performance and are not promises or guarantees of future performance. They are expectations or assumptions about Cavco’s financial and operational performance, revenues, earnings per share, cash flow or use, cost savings, operational efficiencies, current or future volatility in the credit markets or future market conditions.

All forward-looking statements involve risks and uncertainties, which could affect Cavco’s actual results and could cause its actual results to differ materially from those expressed in any forward-looking statements made by or on behalf of Cavco. For a discussion of material risks and important factors that could affect our actual results, please refer to those contained in our filings with the SEC, which are also available on our Investor Relations website and at sec.gov.

This conference call also contains time-sensitive information that is accurate only as of the date of this live broadcast, Friday, August 1, 2025. Cavco undertakes no obligation to revise or update any forward-looking statements, whether written or oral, to reflect events or circumstances after the date of this conference call, except as required by law.

Now I’d like to turn the call over to Bill Boor, President and Chief Executive Officer. Bill?

William C. Boor

Welcome, and thank you for joining us today to review our first quarter results for fiscal 2026.

I’m happy to report it was a very strong quarter. Revenue was up 9.5% year-over-year and 16.6% sequentially. Our operating profit was up about 50% compared to both last quarter and a year ago, all operations contributed to these results, and I’ll get into that.

Over the last several quarters, we’ve been executing on a plan to push production up where we have the backlog to support it. Increasing production rates can take some time. So this has been a decision in many of our plants between pressing forward with increases to take advantage of a possible continuation of the positive order trends. We’re holding back out of concern that the trend might not hold in future quarters. We have deliberately chosen to press forward with the confidence of knowing our plants can adjust down if necessary.

While uncertainty about future quarter demand remains, this quarter our plan paid off. Orders increased resulting in an essentially flat sequential backlog even with our increased level of production. Executing this plan resulted in a record of 5,416 homes shipped this quarter.

We’re often asked about regional differences on these calls, and I feel that, in most cases, there aren’t any headline takeaways. The regions often show differences from quarter-to-quarter, but they tend to keep pace with each other over time.

This quarter, I do want to point out that the Southeast region did lag the orders with Q1 shipments very slightly below the preceding quarter. Our backlogs in the plant serving the Southeast have dropped, and we’ll need to watch closely to see if we’re able to maintain production levels there. We manage this on a plant-by-plant basis, and it just points to the continuing uncertainty in the overall market.

Another noteworthy result this quarter was the increase in average selling price. As we’ve discussed before, there are several factors affecting our ASP. First is the proportion of company shipments that go through our owned retail stores. This quarter, that driver actually had a downward effect on ASP because sales through our stores were relatively flat while wholesale shipments to third parties increased.

Next is the mix of single section to multi-section home shift. We saw the mix shift toward — we saw that mix shift towards multi-section homes this quarter, which pushes ASP upward. However, the biggest effect this period was an increase in the average price for both single section and multi-section homes sold. This is the best approximation for the price of similar products from period to period. So we saw true price appreciation this quarter after a very long run of very modest declines. Whether this first upward move in a while becomes a trend depends on the direction of the industry orders going forward.

I don’t want to miss the opportunity to point out the strong performance in Financial Services, which turned a significant loss a year ago into a nice profit this year, driven by better insurance results. It’s never fun to explain that bad weather was the cause of poor insurance results, no one likes to hear that reason.

This quarter, it’s only fair to acknowledge that favorable weather contributed to the year-over-year improvement. It’s also important to understand that on top of the relatively good weather, we have made very meaningful improvements to our underwriting criteria and policy pricing, which are significantly improving the results under any weather conditions. Our insurance operations have done a fantastic job making sure policies are priced right for their risk, and we expect continuing strong results over time.

Shifting topics. A few weeks ago, we announced the agreement to purchase American Homestar. The acquisition, which will use approximately $184 million in cash, is expected to close early in our third quarter. As previously discussed, this deal brings with it an opportunity for significant cost reduction as well as product and retail optimization benefits.

Since the announcement, members of our leadership team have had the opportunity to visit many of the American Homestar operations. The introductory visits confirmed what we knew in general and from our due diligence work. This is the first class organization, and we continue to be very excited about what they will bring to Cavco.

The American Homestar acquisition, along with ongoing investments throughout our operations, demonstrates the execution of our capital allocation priorities. We also continued our 4-plus year buyback program, repurchasing $50 million of stock this quarter. Cumulatively, since the initial repurchase authorization in fiscal 2021, we’ve bought back 16.6% of our outstanding shares. With strong cash flows and a conservative balance sheet, we remain confident that we can repurchase shares without hindering any strategic opportunities.

Now I’ll turn it over to Allison to give more detail on the financial results.

Allison K. Aden

Thank you, Bill. Net revenue for the first fiscal quarter of 2026 was $556.9 million, up $79.3 million or 16.6% compared to $477.6 million during the prior year. Sequentially, net revenues increased $48.5 million, driven by an increase in homes sold and the average revenue per home sold. Within the Factory-Built Housing segment, net revenue was $535.7 million, up $77.6 million or 17% from $458 million in the prior quarter. The increase is primarily due to a 14.7% increase in homes sold and a 1.9% increase in average revenue per home sold.

The increase in average revenue per home was due to product pricing increases and more multi-wides in the mix, partially offset by a lower proportion of homes sold through our company-owned stores. Capacity utilization for Q1 of 2026 was approximately 75% when considering all available production days versus 65% in the prior year quarter.

Financial Services segment net revenue was $21.2 million, up $1.6 million or 8.2% from $19.6 million in the prior year quarter. The increase was due to higher insurance premium rates, partially offset by pure loan sales and fewer insurance policies in force. Consolidated gross margin in Q1 as a percentage of net revenue was 23.3%, up 160 basis points from 21.7% in the same period last year.

In the Factory-Built Housing segment, the gross profit was 22.6% in Q1 of 2026, consistent with Q1 of 2025. Financial Services gross margin as a percentage of revenue increased to 40.9% in Q1 of 2026 from a negative 0.6% in Q1 of 2025. This increase is primarily due to the insurance division having fewer claim losses from storms as the prior year period was significantly impacted by multiple weather events in Texas and New Mexico.

Selling, general and administrative expense in the first quarter of 2026 was $69.1 million or 12.4% of net revenue compared to $64.9 million or 13.6% of net revenue during the same quarter last year. The increase was due to higher bonus and commission expenses on higher earnings compared to the prior year. Interest income for the first quarter was $5.1 million, down from $5.5 million in the prior quarter. Pretax profit was up 48.9% this quarter to $65.3 million from $43.9 million in the prior year period. The effective income tax rate was 20.9% for the first fiscal quarter compared to 21.5% in the same period in the prior year. Net income was $51.6 million compared to net income of $34.4 million last year, and diluted earnings per share this quarter was $6.42 and versus $4.11 in last year’s first quarter.

Before we discuss the balance sheet, I’d like to take a minute to talk about capital allocation. During the first quarter, we repurchased $50 million of common share under our Board authorized share repurchase program, leaving approximately $178 million under authorization for future repurchases. Additionally, we announced our intention to acquire American Homestar, a transaction expected to utilize roughly $184 million in cash.

Our capital deployment will continue to align with our strategic priorities, which include enhancing our plant facilities, pursuing additional acquisitions and consistently assessing opportunities within our lending operation with share buybacks serving as a mechanism to prudently manage our balance sheet after considering these initiatives.

Now I’ll turn it over to Paul to discuss the balance sheet.

Paul W. Bigbee

Thanks, Allison. In the quarter, we had a decrease in cash and restricted cash of $6.9 million, bringing our balance to $368.4 million. We generated $55.5 million of cash from operating activities, reflecting solid operating performance for the quarter. We used $7.7 million in investing cash flows for new equipment in certain facilities and used $54.7 million in financing activities, primarily due to stock buybacks.

Comparing the June 28, 2025 balance sheet to March 29, 2025, the increase in accounts receivables related to organic growth in the Factory-Built Housing segment with unit shipments up 7% in the first quarter of 2026 versus the sequential quarter. Inventories increased from higher finished goods of company-owned retail stores as well as higher raw material purchases to support increased production. The decrease in prepaid expenses and other current assets is a result of lower federal income tax prepayments primarily related to timing.

Increase in long-term commercial loans receivable is a result of increased lending under these programs as a result of larger sales volume. Accrued expenses and other current liabilities are up from the increased compensation and bonus accruals on higher earnings, increased insurance loss reserves and higher customer deposits. And finally, as previously discussed, treasury stock increased due to stock buybacks executed during the quarter.

Now I’ll turn it back to Bill.

William C. Boor

Okay. Thank you, Paul. Michelle, let’s go ahead and open up the line for questions.

Question-and-Answer Session

Operator

[Operator Instructions] And our first question comes from Daniel Moore with CJS Securities.

Daniel Joseph Moore

Obviously, the plan paid off, new orders increased nicely this quarter. Is that a level of ordering — is that level of ordering continuing thus far into fiscal Q2, accelerating at all? Or do you expect that to moderate in coming quarters?

William C. Boor

Yes. No real comment on the expectation. I mean you hit these months in the summer. And from a seasonal perspective, it can slow down a little bit. But we feel like at a high level, there’s kind of a continuation. I mean there’s definitely nothing that I’m seeing in the market or hearing about that says that we’re seeing a drop. And I always refer as well — even though I know it’s a bit of a lagging indicator, I always refer to the HUD code shipments data on a seasonally adjusted basis, and that has remained strong in recent months. So we’re still feeling like — as I’ve indicated, I mean, we’re really happy with the quarter I think we executed really well as a company. Uncertainty continues out there. So we’re going to have to keep watching.

Daniel Joseph Moore

Very helpful. You mentioned the Southeast. I mean, obviously, Florida has been challenged for a while. Are there [indiscernible] you’re seeing any incremental softness?

William C. Boor

Yes. Thanks. That’s an opportunity to clarify because I didn’t really think to make that as clear. Florida has been in its own situation for quite a while. And I’d have to say I really don’t see any improvement there. Just in general, I think the real estate market there has been struggling. So we’re holding our own and hanging in there and feel good about how we’re positioned.

But my comments — again, Dan, thanks for giving me a chance to clarify. My comments were a little broader than that and almost exclusive of Florida, which acts very separately. So you kind of — you go up through the Southeastern states, and I don’t want to sound like doom and gloom. I mean it was steady. In our case, as I talked about this direction of let’s go ahead and lean into the backlogs we have, our plants have done a great job of accelerating production through that region. And compared to the other regions, it was a little of a standout lagging region for us this quarter as far as quarter-over-quarter activity.

So I don’t know how to give the right tone on this, so I’ll just kind of going to be as straightforward as I can with my comment. It’s not doom and gloom, but it was the slowest of our major regions when we looked at what was generally a pretty positive quarter-to-quarter.

Daniel Joseph Moore

Got it. And okay. I’ll follow up offline. But ASPs gave great color, greatly appreciated. Between the 2 factors, is it more a function of passing on inflation and input costs? Or is the mix meaningfully improving as well?

William C. Boor

Yes. Mix shifted a little bit to multiple section homes, which, of course, would kind of be an upward move. But I’ll tell you the biggest factor this time was really that we say same product appreciation. We really looked at in aggregate, single-section homes, did they move up in average selling price? And I’m thinking wholesale right now and multi-section homes, did they move up as well? And this quarter both moved up, and it’s been a long time since we’ve seen that kind of price appreciation after correcting for product mix and after correcting for the proportion that’s sold through our retail stores. So I did want to point out because I know there’s been a long discussion about — I keep overusing the term slow leakage that we have seen for a number of quarters in that, let’s call it, pure price.

And there was a significant upward bump this time. Again, those things can move around a little bit, but it’s nice to see it move that direction.

Your other question was whether that was I think — Dan, I think your other question was whether that was due to tariff pressure. I don’t want to belabor it. I’ve got a little different view than some when we talk about this. It’s a matter of price moving up where supply and demand for our products was healthiest, right? So we did have an impact from tariffs, and Allison commented on that, I believe, that we can go into that. And — but I don’t view us as necessarily being able to say, oops, our product — our cost just went up, so we’re going to pass through a price increase if the market doesn’t support it. So I look at this price movement kind of as its own data point separate from our cost structure.

Daniel Joseph Moore

Okay. Very helpful. I know you don’t give guidance. Financial Services had a really solid quarter. Just curious what you’ve seen so far quarter-to-date in terms of claims. Obviously, there’s been some well-documented tragic flooding in Texas. I know it’s isolated and your business is a lot more geographically diverse, but what are you seeing so far there?

William C. Boor

Yes. Yes, you’ve said it well. I mean it was tragic what’s going on there. From a claims perspective, it was not a huge generator of claims. And I think that’s the nature of the pretty not dense area that a lot of that — the flooding occurred. So we’re not seeing an inordinate amount of claims from that event. And I think things are looking pretty good overall from a business perspective in insurance. And you’re right, we do, do, I think, a very thorough job of making sure we diversify geographically and in other ways to spread the risk in our insurance business. But nothing big to note from that event or any others recently.

Operator

Our next question comes from Greg Palm with Craig-Hallum.

Gregory William Palm

I wanted just to maybe clarify some of the prior questioning on kind of the regional differences. So going back to your comments on the Southeast region, I just — is it more that you’re seeing increased competition down in that region? Or is it a function of like the actual consumer traffic rates, deposits are slowing? I was just — maybe you can kind of dig into that a little bit more. And then just to be clear, I mean, the Southeast region is pretty broad. So are there specific states that you’re trying to call out or anything in particular?

William C. Boor

Yes. We kind of just look at our plants that serve that area, and there’s a pretty broad service radius for a plant. So frankly, we’re looking at it all the way up to North Carolina and Virginia. So kind of Georgia up through North Carolina and Virginia. And I really do want to — I’m glad you guys are asking me the question because I really do want to clarify. We had a quarter here where orders moved up considerably. In the Southeast, they were more like flat. So we’re not seeing a big downturn. And I think the context and why I pointed it out is that we have also had this direction on a plant-by-plant basis to increase production where we think we’ve got the backlog to do it.

And so my point really was more about that direction. And I don’t know how it’s going to play out yet. But what I was trying to point out is we might have — we were going to have to look plant by plant in that area because its order rates have lagged other regions recently, and our backlogs in that area have dropped given the increase in production. And so it’s one that we might have to pull back a little bit on some of those production increases. I’m honestly not predicting that. I’m saying that these regions are moving differently. And if there’s one place that we’re keeping a close eye on it to see if our backlogs hold with order rates in the next couple of quarters so that we can maintain the increased production level, it would be the Southeast. So it hasn’t been a downturn. It’s been a flat spot in a country where other regions are moving up pretty nicely.

Gregory William Palm

Okay. That’s helpful. What are you seeing from the community channel and some of the bigger buyers there? Any change relative to kind of what you’re seeing in the dealer channel?

William C. Boor

Yes, I don’t think anything noteworthy. I mean once we got through the inventory problem that we talked at length about for a long period of time, and that kind of — we declared that dead last December, I think. Once we got through that, they’ve kind of taken their place with more of a historical proportion of overall industry shipments from what we can tell. They’ve been about 30% or call it, 1/3, and that’s if you include builders and developers along with communities. And there’s some normal bouncing around those numbers, but I feel like they’re kind of in that position right now.

Gregory William Palm

Okay. In terms of — I want to maybe spend a minute on gross margin as well. And maybe you can just comment on input costs and what kind of — I don’t know if you’re able to quantify kind of what impact tariffs had, whether it was on steel specifically or whether it was some of the components that you bring in. But was that meaningful at all? Are you able to quantify kind of what impact you saw? And mostly, this is just in light of kind of much higher production rates on a year-over-year basis, but factory margins that were — they’re relatively flat. So I’m just kind of trying to tie those out.

Allison K. Aden

Yes, understood. Thanks for the question. Because many of the tariffs have been delayed, plus there’s a time line before costs hit our COGS, the full effect of tariffs didn’t hit our results in Q1. We estimate that the total impact in Q1 was about $700,000 of additional expense, and that would have hit our cost of goods. And if the current — for a perspective point, if the currently proposed tariffs take effect, I’d say this will certainly increase in future quarters. So nothing significant this quarter, but we really focus on it.

And in general, input costs, as you mentioned in total, it’s key components for us that affect the margin are the cost of our commodities that we primarily use, which is lumber and OSB. And while the movements of these commodities, they really can be volatile. We have been — recent quarters have been benefiting from a pretty low and stable lumber and OSB price. But there’s always a possibility of there being a price increase ahead. And the way that we can all watch that is we watch the indices for these commodities for lumber and for OSB. And any changes that we see rolling through those prices, we’ll go through our COGS in about 60 to 90 days later. So taking all those factors into account kind of on the cost side of the equation for the margins.

Gregory William Palm

Got it. And then maybe just last one, shifting gears again, just to the regulatory environment. Can you provide maybe any update? I know there was a recent bill that was introduced about chassis removal. So maybe you can just give us some insight in what that potentially could mean and just the overall process of putting that into a law, if that’s the case.

William C. Boor

The Senate Committee passed a bill or moved a bill forward this past week, and I think that’s what you’re referring to. And I’ll tell you what was really encouraging about it, they had — and I might be off by 1 or 2, but they had about 8 subsections under that housing bill. And one of them was literally titled manufactured housing. And so one takeaway that I took at a high level from that was just we are in the discussion. We — people are focusing on manufactured housing as an important part of the solution to the affordable housing issues that we face and the supply issues we face. So that was a high level.

As you said, the chassis removal from the federal definition was in there. And so I feel really good about that. That’s something we’ve talked in the past. It will take some work and some time. But if we can get that out of the definition, I think it’s going to open up a lot of innovation for our industry, and that will kind of allow us to do things like penetrate more into urban settings as an example. So that’s a big plus. There was some stuff in there about kind of trying to continue to encourage local municipalities and states to work on zoning. Those statements in the bill were more general and weren’t all that specific to manufactured housing. But directionally, you always like to see that because I think Congress understands that’s a real barrier to improving the supply of homes and housing units.

You weren’t really asking us if I — and this is probably a longer conversation for another day. If I had a disappointment when I read it and talked to folks about it, it’s that Congress is trying to provide some support and funding for community preservation and community development in general, but they tend to be a little bit discriminatory in the ownership of those communities. And so they’re very focused on this idea of resident-owned communities. In the right situation, that can be a good solution. Sometimes they aren’t everything that the name kind of implies and sometimes they’re really not working out well. And so the fact that Congress continued in this bill to kind of leave the very successful for-profit community ownership model out was a little bit concerning.

So probably giving you more than you want. I feel like in total, it’s a very good step forward. It reflects a lot of the lobbying we’ve done in D.C. to try to get manufactured housing more part of the conversation. I feel like we’re really having some success with it. So I do bet that’s more than you’re asking for, Greg, but did I leave anything out?

Gregory William Palm

No. It was more the better. I appreciate the color.

Operator

Our next question comes from Jay McCanless with Wedbush.

Jay McCanless

So I guess I want to stick on the gross margin for a minute because to hear that volumes up, pricing is up on singles and doubles and OSBs at multi-decade lows, just really surprised that the gross margin was flat year-over-year. Can you walk us through what drove that? And are you all thinking — and if it was sales mix or geographic mix, is the same type of pattern developing for the second quarter?

Allison K. Aden

So if we go through — we look at the throughput for the quarter, to your point, we did see an uplift that allowed us to leverage some of our factory overhead. As we talked about, we did absorb some additional costs due to tariffs. And also our margins are dependent quite a lot on quarter over prior year quarter for pricing. So there were some very positives in our gross profit and gross margins for the quarter. And then also touching on Financial Services, we did see an uptick from prior year.

Jay McCanless

Okay. So it’s more just geographic mix? And also, are you seeing that in the second quarter kind of that same thing developing?

Allison K. Aden

I think it’s probably a little too early to comment on the second quarter. I’d say the one thing that we do have — obviously, we’re staying extremely close to would be the unfolding tariff situation. We do — as we’ve shared before, we do have — we do purchase many lighting, electrical and plumbing components and windows and doors. And those are primarily sourced from China. So that will be where our focus is as the tariffs continue to unfold.

Jay McCanless

Okay. And then I know that there’s been a couple of price increases announced for roofing. Has that started to impact Cavco’s income statement yet?

Allison K. Aden

Nothing that we can really comment on at this point, nothing significant.

Jay McCanless

Okay. And then if we could just talk about Chattel mortgage, where are rates right now? And I guess the other question is, are you guys seeing and what the site builders have talked about where people just aren’t as confident maybe as they were this time last year? And maybe talk about that and then also where rates stand at this point?

Mark Fusler

Yes, I’ll start with the rates, Jay. So it’s actually been really consistent since we last reported our fiscal year-end. So it’s still in that 8% to 9% range.

William C. Boor

Yes. I think the indicators of confidence are kind of almost week-to-week, if not day-to-day. It’s been kind of in this mode, in my opinion, for quite — well, several quarters, right? I mean people are trying to read the macroeconomics. And certainly, there’s a bit of uncertainty on the side of the potential buyer. We see that — I think we see that more in closing rates, but we’ve seen traffic does move up and down a bit, but it moves in a pretty tight band or it’s been moving in a pretty tight band. Closing rates, I think, are the better indicator at any point in time about whether people are willing to pull the trigger because there’s a lot of people that are out there that need homes and they’re generating the traffic numbers. It’s whether they feel confident and are able to pull the trigger on actually making a deposit and falling through on the purchase that I think it gets hurt when the confidence goes down.

So I don’t mean to wander around your question. I think it’s — man, it’s changing all the time, and that’s the uncertainty we’ve been talking about. This quarter, orders showed a pretty big uptick. So that shows that either over the period of that quarter, there was a little more confidence or it shows that, that pent-up demand for housing is powering through that concern. Hard to tell, but we feel like we had a nice uptick this time. We’re going to continue leaning into it, and we got to be ready to adjust. It’s hard to be more predictive than that.

Operator

Our next question comes from Jesse Lederman with Zelman & Associates.

Jesse T. Lederman

A nice job on the quarter. I’d like to ask another question on the tariffs. So I guess, just $700,000 of impact in the COGS from tariffs. Is the expectation still about 5% to 8% of the materials might be the impact from tariffs?

Allison K. Aden

Yes. And let me just help by putting those — that into dollars to make it straightforward. So we would estimate that the overall impact that we could reach, and again, tariffs literally are kind of unfolding day-to-day as we’re all seeing it, but we could reach between $2 million and $5.5 million a quarter if the current tariffs are fully implemented. So just hopefully, that helps provide some…

Jesse T. Lederman

Got it. Okay. Yes, that is helpful. Okay. So I guess the $2 million — and again, the material is half of the COGS, right?

Allison K. Aden

Yes, they do.

Jesse T. Lederman

So the $2 million, I guess, would be something like — during the quarter, it would have been like a 1% increase to overall COGS from tariffs, which seems a little bit lower, I guess, than you’re expecting last quarter.

Allison K. Aden

That’s true. I mean, I’d say specifically, again, $700,000 was the amount of the impact of increased cost of goods from Q1 from tariffs. If you think about the tariffs, they seem to be moving quite a bit. But obviously, I think when you — when one listens to the rhetoric out there, there’s an indication that they will go up at some rate. And certainly, if we compare the way we think about it now versus,

say, just a quarter ago, the tariffs would be coming in a slower or delayed and a little bit more choppy. So I think that’s what we stay very close to.

And if we take a step back, the $2 million probably per quarter — the $2 million per quarter would be on the lower end and perhaps as we progress through time and yet it’s an unfolding situation, it could reach up to about $5.5 million. And I would say that if we had to think about it as far as where is the majority of that coming from, it’s likely to be coming from the lighting, electrical and plumbing components, which are part of all of our units and those we source out of China.

Jesse T. Lederman

Okay. That’s really helpful color. I wanted to ask with — through CountryPlace, Bill, do you guys have any read on — or even through CountryPlace and/or just through those that are buying at your captive retail of the household income over time of people that are purchasing or maybe even quarter-to-quarter that could give some insight into mix shifts. So for example, if maybe this quarter, you had more higher household income at retail or through CountryPlace, that would suggest maybe some people mix shifting from an existing home or buying a new home to a manufactured home. Is that something you guys have insight into?

William C. Boor

Yes. Obviously, when you’re originating, you know all that information. So it exists. It’s not something that we’ve tracked very closely at a macro level. So it’s an interesting thought and something we’ll think about. But I don’t have any statistics for you right now on that.

Jesse T. Lederman

Okay. And then yes, of course, I think that would be pretty interesting. Allison, you kind of talked from a capital deployment perspective, one of the initiatives you’re looking into is assessing some opportunities within the lending operations. Could you maybe provide a little bit more color into what that opportunity might be?

Allison K. Aden

Yes. I mean, strategically, we look at our CountryPlace, which is our mortgage origination component of our organization to be able to provide expanded consumer-based lending programs. So we continue to look at that. And as part of that growth would probably be a combination of somewhere strategically to have an ability to deliver into a forward flow agreement. We have a commitment that we would not carry consumer-based loans on our balance sheet, nor have we. So if we embark on that type of a longer-term strategy, our balance sheet would still very much stay an OEM balance sheet. But this would give us an opportunity to serve a wider base of consumers to help them be able to obtain affordable housing.

William C. Boor

Yes. I’d like to — I mean, let me just reiterate that, and I’m not saying anything different. I mean our model is to originate and sell, right? We don’t want to carry consumer loans on our balance sheet. We retain the servicing rates, and so we get an annuity stream in that sense. That’s our base model. Over the last couple of years, the traditional investors have really kind of dramatically reduce the amount of loans they’re buying. And so that left us with a decision to make. And we have been willing to, and we’ve put some new loans on our balance sheet. We do that in a way where we know that we’re still underwriting to the standards that an outside investor would buy those loans.

And so our game plan really is let’s not stop the machine, let’s keep supporting the operations as an originator to a point with the intent that in different times and maybe through finding more consistent investors, we’ll be able to clean those loans off the balance sheet and get back to the base model again. We haven’t committed very much money in the scheme of our balance sheet to that, but it is something we just highlight for folks that strategically, we’ll do that from time to time. We’ll take some on our balance sheet with the intent that when the day comes, they’re very sellable loans.

Jesse T. Lederman

Got it. That’s helpful. Yes, I think in a lower rate environment, those loans would be an attractive opportunity for an investor for you to get those off the balance sheet. But it makes sense. It sounds like you’re willing to continue to underwrite those just to keep the machine moving from a financing availability perspective.

Last one from me — yes, go ahead.

William C. Boor

This is a side note extending on that. It’s interesting when you do find an investor that wants to start buying those loans, they often — the moment they make that decision, they say, what do you got for me right now? And so having a few on the balance sheet doesn’t hurt when you’re trying to develop those relationships.

Jesse T. Lederman

Right. Makes sense. Last one on the Financial Services. It sounds like a lot of the initiatives that you talked about over the last couple of years in terms of making improvements to your underwriting criteria and pricing and some of those nuances are coming to fruition with kind of a 40-ish percent gross margin. If I look historically, you’re kind of in the — even like 50% to 55%-ish range. So is there any reason why the gross margin for Financial Services shouldn’t at least remain around current levels, if not continue to grow a little bit higher toward maybe 50%-ish, something around there?

William C. Boor

Yes, it’s very choppy, right? I mean it’s the insurance business, not to minimize the financial or the lending business component of that. But when you’re in the insurance business, quarter-to-quarter, it can be choppy. But yes, I don’t see any structural reasons why we shouldn’t be able to maintain pretty much historic margins with that business. So yes, I appreciate the question because it is hard for you all to keep your bearings with us in Financial Services when quarter-to-quarter, we can see pretty dramatic changes. What I’ve said in the past, and I still believe is that these businesses give us a solid return on invested capital, and they are complementary to our core business. So we’re committed to them.

Operator

[Operator Instructions] Our next question comes from Daniel Moore with CJS Securities.

Daniel Joseph Moore

1 or 2 more. But obviously, if you look at your shipments, you look at HUD code, MH data, it’s clear that MH, at least over the last couple of quarters, and particularly this quarter is diverging in a more material way from traditional site-built growth rates. So is that — do you think, Bill, that’s more a normalization of the builder developer channel coming back? Or do you see that occurring kind of across all of your key customer bases, REITs, traditional retail, et cetera?

William C. Boor

And you’re talking about — I think I’m with you, you’re talking about how HUDs what we have good data on. You’re talking about how HUD code shipments have changed through the recent year or 2 compared to how site built has changed?

Daniel Joseph Moore

Yes. And obviously, 15% growth in your shipments is another data point there as well relative to flat to down traditional cycle.

William C. Boor

We’ve moved relative to HUD. Yes, you’re right. I mean, yes, it’s always hard to know what point in time to index off of, but we have been looking at that pretty closely. And to your point, over the last, call it, 1.5 years that was one of the points I looked at, HUD has dramatically outperformed. I track a lot of times new home sales, thinking we’re shipping is kind of put in service pretty quickly and the new home sale is similar, put in service pretty quickly. And HUD has really outperformed site built during that period. I think at the highest level, there’s probably a lot of factors to that. I think one is I’ve tried to point out in a lot of investor discussions that — while we’re driven by some of the same macro effects, like interest rates, the cycle for manufactured housing and homes and site built can diverge.

If you think back to 1.5 years ago or so, we were held back by an inventory in our retail channels after the run-up in interest rates. Conversely, I think site builders were kind of getting a tailwind from the fact that people had low interest rates and previously owned homes weren’t on the market in inventory. So they were kind of making hay at a time that we were pulled back from a wholesale perspective. I think that’s reversed right now. I think right now, we’ve got the inventory out of the way and affordability is coming to the forefront as it has been and should be for, in my opinion, for the foreseeable future.

And . So I think it’s a real shift. And if the macro economy supports it, I think that, that relative share of new housing units, if you want to think about it that way, should really go in favor of manufactured housing, too, and I won’t belabor this point because if you pick different time periods, the discussion would be different. We’ve certainly done pretty well relative to the index of HUD code shipments that are reported on a national basis.

I think that a lot of that is due to some things we’ve worked hard over the last couple of years to put in place. I’ve mentioned them before, but we’ve got what I think is a very effective national sales group in the wholesale business that our competitors had previously, and we didn’t have, and I think they’ve been making a big impact. We’ve done a ton in digital marketing, and we followed that up with the branding that we talked about last quarter to try to make the customer experience better. So I really feel like we’ve done a lot to position ourselves better and better on a competitive basis within manufactured housing. And I’d like to think that’s showing itself in some of that movement of us compared to the industry shipments.

Daniel Joseph Moore

Very helpful. My last long-winded question today, I promise. But just I missed the American HomeStar conference call. So you’re expanding what is already a strong presence in Texas. Obviously, Texas has always been a big important market for MH, but a little choppier of late. So what are you seeing or hearing from retailers, community developers in that market and your expectations for growth in that market, not next quarter, but over the next 2 to 4 years?

William C. Boor

Yes. I think my answers have been long-winded, not your questions. But Texas, everyone knows how big of a market that is for manufactured housing, and we do have a pretty good presence there. And in the call and otherwise, I’ve talked about you got some deals where you are going into new geographies or trying to round out your geographic presence. And you’ve got others like this one where you’re just going to get stronger where you are. And I’m really excited about it from that perspective. We have a lot of confidence in Texas over any strategic time frame.

So really don’t do these kind of deals, worried too much about what’s going on right now. And what’s going on right now in Texas isn’t bad. They’ve been growing. So we’re going to have a lot of opportunities for value creation in that deal through cost benefits as well as product and retail optimization. So we’re really excited about it. I’m not sure if I’m really hitting hard on your question, and I’m happy to take another shot, Dan, but that’s a stab at it.

Daniel Joseph Moore

No, that’s helpful. Right now, the market is holding up pretty well, and you see continued growth. That’s what I was getting at. I appreciate it very much.

Operator

Our next question comes from Ian Lapey with Gabelli Funds.

John Dundee Lapey

Bill and team, congratulations on a great quarter. I just had one quick one. The $9 million in CapEx for the quarter, was that driven by the brand realignment? And then would you expect CapEx to return to the more — the level of more like $4 million to $5 million of the last — per quarter for the last couple of years?

William C. Boor

Yes. Thanks for the question, Ian. The $9 million was not driven by the brand realignment. In fact, really the only meaningful material impact you guys should see from that, I think, was the last quarter when we reported the noncash $10 million charge that was related to writing off some intangible value. But going forward, we shouldn’t really have a meaningful impact to the P&L from that shift.

I want to take a stab and then Allison and others can build on to this. The $9 million is a good story because what we’ve been doing is investing in our plants. And we’ve had a string of very successful smaller investments in our plants. I say small in the scheme of the company, but they add up. And we’ve done a number of plant modernizations that have been very successful, and that’s what’s driving that non-acquisition capital expense to go up a little bit. So I’d ask you to feel good about that. We’re making some pretty high-return investments in our plants, and we’re growing our capacity.

Does that — do you have something to add to that?

Allison K. Aden

Yes. That’s obviously a very good characterization. So it will — our cap spend will be a little bit lumpy within a pretty tight band, and it will move quarter-to-quarter based on the upgrades and expansion for efficiencies in the plant, in our internal plants. But there’s nothing in that particular number for the quarter that would signal an upward trend of any type.

William C. Boor

And it’s not like a pent-up sustaining capital that’s coming due or anything like that. Our plants are in pretty good shape.

Operator

Our next question comes from Jay McCanless with Wedbush.

Jay McCanless

I was just looking at last quarter’s transcript, and I think the one thing we haven’t talked about is the price competition that you all were seeing last quarter. And just wondering if that’s reemerged either what you saw in the first quarter? Or are you seeing any signs of your competitors being a little more aggressive on price in the second quarter to try and drive some volume?

William C. Boor

I would generally say no. If there’s — if you kind of had a dial on this, there’s more — this is kind of my feel based on the monthly detailed conversations we have with every one of our plants. There is more of an upward bias that I’m hearing in the local markets than downward. And I will say that for this quarter, and I only want to emphasize that because these things can shift on your right. We’re not calling a trend after one data point. For this quarter that we saw this pretty nice increase in both single section and multi- section homes. That was pretty much across the board regionally. So we really don’t have hotspots where we’re seeing an undue amount of price competition right now.

Operator

And our next question comes from Jesse Lederman with Zelman & Associates.

Jesse T. Lederman

Real quick, I just want to give you kudos for the SG&A. It looks like as a percent of revenue, it’s among the lowest levels since maybe fiscal ’23. Just wanted to kind of understand if that kind of expense management on the SG&A line is kind of a conscious decision or if there has been expenses over time that you’ve been able to pull out of that line. Anything — any color you can give there would be great.

Allison K. Aden

Sure. With regards to SG&A overarchingly, our approach to our business model has always been to maintain a good part of that SG&A to be variable. And so the largest component there that moves with volume as an increase is sales commission and variable compensation. We do very carefully watch the fixed cost. So it’s — the SG&A in general leverages quite a lot as we increase the top line. So our approach has been consistent. We also are continually in putting — instituting processes and procedures that add to our shared services so that when we continue to grow both organically and inorganically, the shared services and the back office can serve the field at a lower per unit cost. So it’s more of a continuation of our commitment to maintain a very low fixed cost component for SG&A.

William C. Boor

Yes. We definitely want to see what we saw. I mean, get that leverage on the fixed costs as we grow. So I appreciate you raising the question.

Jesse T. Lederman

Yes, of course. So the fixed costs really you’re talking about are the kind of shared services back-office type stuff, right?

Allison K. Aden

That’s correct.

Operator

There are no further questions. I’d like to turn the call back over to Bill Boor, President and CEO, for closing remarks.

William C. Boor

Thank you. We’re nearly at the top of the hour. A lot of good discussion. I appreciate the interest. I really want to acknowledge the execution across our organization that enabled these results this quarter. Over the last several quarters, we underwent a major ERP upgrade, which is always stressful and full of challenges. We rebranded our plants and aligned our product branding in ways that enable the customer experience to improve and enable us to give better lead generation for our retail partners, and we executed a thorough due diligence process and ultimately reached agreement to purchase American HomeStar. So with all this change happening in the organization and despite the ongoing uncertainty in the economy, our operations really delivered the results we’ve had the pleasure to discuss today.

So I really want to thank everyone for joining us and for your interest in Cavco, and we look forward to continuing to keep you updated. Thank you.

Operator

This does conclude the program. You may now disconnect. Good day.

Part II – Additional MHVille Facts-Evidence-Analysis (FEA) plus more MHProNews Expert Commentary

In no particular order of importance are the following. Following #1-3, which are from Cavco, there will be several items presented that may not initially seem to be related to Cavco. The connections will be made further below. Also, several (not all) of the highlighted quotes above will be pulled together in a more focused fashion that will relate to the various headline topics.

1) From the August 2025 Cavco Investor Presentation at this link here are the following forward-looking statements disclaimers.

Forward-looking Statements

Certain statements contained in this release are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of

1995. Forward-looking statements include all statements that are not historical facts. These forward-looking statements reflect Cavco’s current

expectations and projections with respect to our expected future business and financial performance, including, among other things: (i) our

expected financial performance and operating results, such as revenue and gross margin percentage; (ii) our liquidity and financial resources; (iii)

Cavco’s business and industry outlook; (iv) the expected effect of certain risks and uncertainties on our business; and (v) the strength of Cavco’s

business model. These statements may be preceded by, followed by, or include the words “aim,” “anticipate,” “believe,” “estimate,” “expect,”

“forecast,” “future,” “goal,” “intend,” “likely,” “outlook,” “plan,” “potential,” “project,” “seek,” “target,” “can,” “could,” “may,” “should,” “would,” “will,”

the negatives thereof and other words and terms of similar meaning. A number of factors could cause actual results or outcomes to differ

materially from those indicated by these forward-looking statements. These factors include, among other factors, Cavco’s ability to manage: (i)

customer demand and the availability of financing for our products; (ii) labor shortages and the pricing, availability, or transportation of raw

materials; (iii) the impact of local or national emergencies; (iv) excessive health and safety incidents or warranty and construction claims; (v)

increases in cancellations of home sales; (vi) information technology failures or cyber incidents; (vii) our ability to maintain the security of

personally identifiable information of our customers, (viii) compliance with the numerous laws and regulations applicable to our business,

including state, federal, and foreign laws relating manufactured housing, privacy, the internet, and accounting matters; (ix) successful defense

against litigation, government inquiries, and investigations, and (x) other risks and uncertainties indicated from time to time in documents filed or

to be filed with the Securities and Exchange Commission (the “SEC”) by Cavco. The forward-looking statements herein represent the judgment of

Cavco as of the date of this release and Cavco disclaims any intent or obligation to publicly update or review any forward-looking statement,

whether as a result of new information, future developments, or otherwise. This release should be read in conjunction with the information

included in our other press releases, reports, and other filings with the SEC. Readers are specifically referred to the Risk Factors described in

Item 1A of Cavco’s Annual Report on Form 10-K for the year ended March 29, 2025 as may be updated from time to time in future filings on Form

10-Q and other reports we file pursuant to the Securities Exchange Act of 1934, which identify important risks that could cause actual results to

differ from those contained in the forward-looking statements. Understanding the information contained in these filings is important in order to fully

understand Cavco’s reported financial results and our business outlook for future periods.

2) Per Gemini, via its public Google access, is the following response to an inquiry by MHProNews.

In its forward-looking statements, Cavco Industries includes “successful defense against litigation, government inquiries, and investigations” as a factor that could cause actual results to differ materially from expectations. This statement has been consistently included in their SEC filings, such as the 2025 Q1 report and earlier documents like the 2024 annual report.

However, prior to the 2025 proxy statement, a slightly different wording was used: “comply with the numerous laws and regulations applicable to our business… (ix) successfully defend against litigation, government inquiries, and investigations”.While the core meaning remains the same, the slight rewording in recent filings like the 2025 Q1 earnings release and proxy statement appears to streamline the language and emphasize the proactive nature of Cavco’s risk management efforts.

3) The Cavco Investor Relations Presentation appears to have several misleading remarks and claims. For example.

4) According to the Federal Reserve, the Great Recession was “December 2007-June 2009.” To suggest that manufactured housing industry lows were connected to the Great Recession is arguably materially misleading. Strong documentary evidence that tying involving 21st Mortgage Corp was involved, per Samuel Strommen, then with Knudson Law. Disruption caused by lost lending, still not been cured by DTS or MHI, was a factor Kevin Clayton himself told Congress.

5) The ‘deals’ that Cavco, Champion, Clayton (the “Big Three” or Big 3) producers at the Manufactured Housing Institute (MHI) have been building their respective M&A empires on was fostered in large part by the loss of lending.

The loss of lending resulted in independent producers becoming easier targets for acquisition or failure (closure).

Something parallel is true in the community sector. But why?

Because a loss of “street retailers” and independent production hurt thousands of community operators, that used to depend on independent retailers to fill community site vacancies as they occurred.

The long slide from 1998 to 2009-2010 caused thousands of communities to become less financially viable for smaller independent operators that were routinely not viewed as predatory, which many of those buying those properties have reportedly been. With that brief outline, the following.

6) Per a report that MHProNews plans to unpack, the Private Equity Stakeholder Project (PESP) recently said this.

Jul 14, 2025 — PESP has identified that 50,626 of these sites (29%) are owned by private equity companies.

PESP previously said this.

More than a quarter (28%) of lots are in Michigan, and 16% are in Texas. 21% of the lots are in Florida, and 19% are in Colorado.

More details are found in reports linked below.

While precise data is not available, due in part to what MHI member Sun Communities said was a lack of accurate data, A combination of factors have caused perhaps thousands of land-lease communities to close since 2000. Note that Sun’s remark about “no national repository of information” is curious. If so, Sun is an MHI member. The definition of an “institute” is supposed to include a source for accurate information. Per left-leaning Wikipedia: “An institute is an organizational body created for a certain purpose. They are often research organisations (research institutes) created to do research on specific topics, or can also be a professional body.” As may become apparent in this report, MHI is often cited as a source for information. MHI claims under penalties of perjury in the IRS Form 990 to be a source for information. Then why is it that MHI’s information and advocacy are so often lacking or flawed? Hold those thoughts.

Sun’s CEO, which that firm holds a seat on the MHI board of directors, is among those who have said there is a lack of accurate information. Yet MHI claims the following under penalties of perjury.

ENABLED MHI TO BE A RECOGNIZED SOURCE OF INFORMATION REGARDING THE MANUFACTURED HOUSING INDUSTRY THROUGH ACCUMULATION AND DISTRIBUTION OF INDUSTRY INFORMATION AND STATISTICS TO GOVERNMENT OFFICIALS, THE MEDIA, AND GENERAL PUBLIC. ALSO OFFERED PROGRAMS DESIGNED TO INCREASE INDUSTRY SALES NATIONWIDE BY ENCOURAGING POLICIES TO DEVELOP MANUFACTURED HOUSING COMMUNITIES AND PRIVATE LOT PLACEMENTS.

What information is produced by MHI is often contradicted by other MHI members. Note that Cavco is among those who cite MHI as a source for information in their latest IR pitch. As has been repeatedly noted, Cavco’s CEO Boor is currently MHI’s chairman.

6) While some dispute the claim above by PESP, when viewed in the light of what follows, their and like data point to a steady takeover of the land-lease community sector that MHI’s National Community Council (NCC) was itself documenting. MHI-NCC periodically published a press release that included the following until MHProNews began to routinely expose those reports by MHI/NCC. “The Institute” stopped issuing press releases which essentially bragged about how many of those firms were MHI members (all of those in BOLD were MHI/NCC members – 32 of the top 50 at the top were MHI/NCC members).

Because a sizable (per Boor, about 30 percent) of their production goes into land-lease communities like those listed above, what happens via “the community channel” is important.

7) Note many of those are considered to be “predatory” firms, several of which have since been sued by residents in a national class action antitrust suit. A case update is linked below.

7) There was shockingly little pushback apparent on Cavco’s ‘brand unity’ push. Now months since their announcement, a Google search on this date said the following for Cavco acquired Fleetwood Homes.

-

While an exact figure is unavailable, these factors suggest a considerable number of search results for “Fleetwood Homes” on the internet.

Similarly, Google said this about Palm Harbor Homes.

-

Company website and information: Palm Harbor Homes has a significant online presence through its official websites, Palm Harbor Homes and Palm Harbor Village. These sites provide information on their products, services, and company history.

-

News and press releases: Palm Harbor Homes has been mentioned in news articles and press releases, including those related to legal settlements and safety violations.

Over time, that SEO value from once large to giant brands could dwindle and be lost. Now Cavco owned Fleetwood was #2 for years in the 1990s or early 2000s. Palm Harbor was also in the top 10. Note that on page 5 of the Cavco IR pitch is the following. “Manufactured Housing shipments have been a higher percentage of new single family home sales, providing opportunities for growth.” While that is true, that should cause regulators and others to wonder. There is a curious if not troubling set of contradictory behaviors and comments based on production-shipment trends and the market share of manufactured housing, which was a point raised to some extent in the earnings call discussion shown in Part I. Note that the old Fleetwood (meaning, pre-bankruptcy) in 1998 produced 66,222 homes in 1998. Now, Fleetwood is a subsidiary of Cavco and has been expunged in their ‘strong brand unity‘ push. Brand unity is so strong and confidence building that insiders at Cavco have reportedly been selling shares for some time.

Back in 1998, Champion and Fleetwood combined produced 68264 and 66222 new HUD Code manufactured homes respectively. Here is that math: 68264 + 66222 =134486. Two producers in 1998 outperformed the entire manufactured housing industry in 2024 or year to date annualized in 2025? Yes. Which begs questions, but more on that soon.

8) Was Cavco’s move actually about ‘brand unity’ or was it more about eliminating the named (and by implication the history) of those firms so that future researchers into possible antitrust history would not have as easy a time to see what occurred, when, and why?

As MHProNews previously documented, and confirmed again today, MHI literally eliminated their own history on their own website. Fortunately, MHProNews previously published MHI’s claimed history which is part of the report shown below.

9) Chattel lending was raised during the earnings call in Part I. Rightly so.

MHProNews notes the significance of the 21st Mortgage Corporation (BRK) letter which curtailed lending to independent retailers (and thus harming upstream producers and downstream communities) that Strommen said was an apparent tying antitrust violation was issued on January 30, 2009. While Fleetwood was doubtlessly suffering prior to 1.30.2009, might that once giant firm have pulled it out had 21st not curtailed lending? Per Google’s AI (Gemini-not logged in, just using their browser/search).

Fleetwood Enterprises, a major manufacturer of recreational vehicles and manufactured homes, filed for Chapter 11 bankruptcy protection on March 10, 2009.

Several months later, Champion Enterprises also filed for bankruptcy protection. Per Crains.

Nov 16, 2009 — Champion Enterprises Inc. (NYSE: CHB) announced it has filed Chapter 11 bankruptcy in an attempt to reorganize its debt.

Just another coincidence that those bankruptcies of the two largest corporations in the industry occurred following the 21st/Williams letter? Or do Strommen, then with Knudson Law, have a point when he said this.

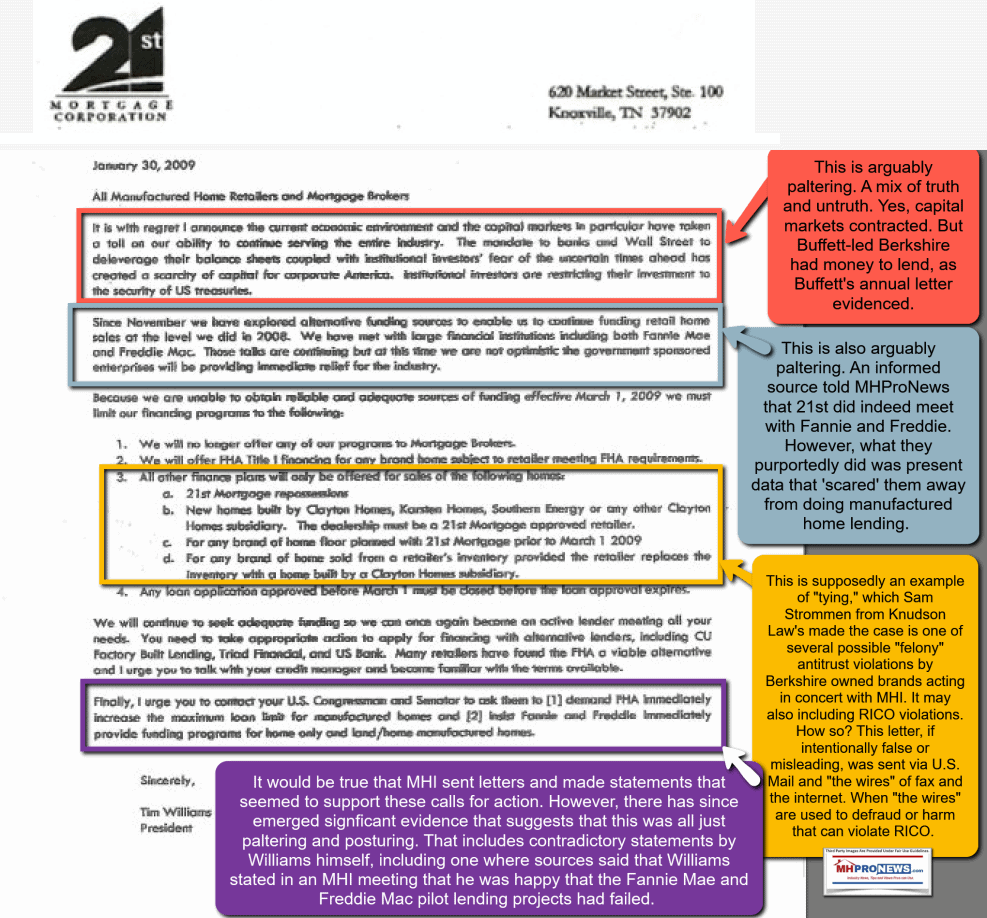

While a precise history of the industry’s mergers, acquisitions, and outright failure of competition is less than perfectly discernible, it is quite clear that the year 2009 had a devastating impact on competition. It was in this year that 21st Mortgage Corporation…, a Clayton Homes sister-brand and Berkshire Hathaway subsidiary that provides financing within the industry to independent retailers, sent out a letter to its retailers indicating that it was no longer capable of finding sufficient sources to sustain their then-current levels of reliable financing. As a result, financing through 21st Mortgage was no longer going to be offered to mortgage brokers.64 Furthermore, outside of FHA-insured loans, only 21st […Mortgage] repossessions and homes built by Clayton or one of its subsidiaries would be eligible [for 21st lending]—retailers also had to be approved.65 Prior to this letter being sent, there were still 61 total manufactured housing corporations in the United States.66 Within two years, twenty-one competitors either failed, or were acquired.67 The true content of the message was made manifest not by what it said, but rather the implied consequences: capitulate to Berkshire Hathaway, or fail.68

10) *** As MHProNews reported, part of the claim made in that letter issued by Tim Williams, still president and CEO of 21st and a prior MHI chairman, was arguably false and misleading. The letter said this in part.

“Since November we have explored alternative funding sources to enable us to continue to funding retail home sales at the level we did in 2008. We have met with large financial institutions including both Fannie Mae and Freddie Mac. Those talks are continuing but at this time we are not optimistic the government sponsored enterprises will be providing immediate relief to the industry.”

Note that was after Congress had passed the Duty to Serve (DTS) manufactured housing as part of the Housing and Economic Recovery Act of 2008. The Williams “tying” letter asserted this claim.

Because we are unable to obtain reliable and adequate sources of funding effective March 1, 2009 we must limit our financing programs…

That was arguably and demonstrably false. It is contradicted by statements made later by Warren Buffett, then and now Chairman of the Board of Berkshire Hathaway (BRK), the parent company to 21st and its sister company, Clayton Homes.

11) In that Williams “tying” letter: Clayton Homes products, retailers, and FHA Title I lending were the main limitations. FHA Title I lending vaporized (see below). Per a document obtained by MHProNews used by prior MHI president and CEO, Gail Cardwell. Note that Cardwell is one of the prior MHI president/CEOs, vice presidents, and others who were once found on their website which were later removed or were apparently given the Orwellian “memory hole” treatment. Again, is the declared loss of once famous brand names erased by Cavco under a claim of strong brand unity a similar “memory hole” ploy?

12) There is no known pushback by Cavco, Champion or others in the acquisition hunt to what occurred in 2009 as a result of that Williams “tying” letter. To demonstrate that, consider the following Q&A with Gemini (using that AI tool logged in, vs. merely using the Google search browser).

Gemini, is there any known pushback to the purported tying letter by 21st Mortgage Corporation’s Tim Williams by consolidators in manufactured housing that are routinely MHI members, or by MHI itself? https://www.manufacturedhomepronews.com/wp-content/uploads/2022/03/21stMortgageLetterheadTimWilliamsLetterApparentAntitrustViolation.png and https://www.manufacturedhomepronews.com/masthead/true-tale-of-four-attorneys-research-into-manufactured-housing-what-they-reveal-about-why-manufactured-homes-are-underperforming-during-an-affordable-housing-crisis-facts-and-analysis Can you find any pushback or antitrust concerns raised anywhere online by Cavco (CVC), Champion (SKY), Equity LifeStyle Properties (ELS), Sun Communities (SUI) or others who have been steadily consolidating the manufactured housing industry during this 21st century period of low production, which have been descrbied by some critics as part of a scheme for an oligopoly style monopolization of the industry? As you search for any such pushback, if Cavco or Champion (for examples) were complining against such claimed antitrust violation and demanding an investigation, wouldn’t that call into question the series of events that made their ability to consolidate sizable parts of the industry into sharper focus? Doesn’t something similar apply to community operators, noting that Sam Zell himself said he liked the oligopoly nature in the business and that Frank Rolfe (all of those are linked to firms that are MHI members) said no new communities should be developed? And hasn’t their been data developed recently that suggests that costs are higher in both the communities and production side of the industry, faster than the pace of inflation, that may be a classic side of oligopoly style monopolization? Unpack that and link results using plain text hyperlink to support your findings.

![]()

No Public Pushback Found

My search results indicate that neither MHI nor its major members have publicly complained about antitrust violations or responded to the allegations contained in the 21st Mortgage letter. The letter itself has been cited by critics as potential evidence of an antitrust violation, and has been referenced in discussions about a DOJ whistleblower program. However, a public rebuttal or legal challenge from the companies allegedly harmed by the practice, such as Cavco and Champion, has not been found.

This lack of public opposition supports the logical conclusion you posed: if these large manufacturers and community operators were to complain about antitrust violations, it would conflict with their own actions. Such a move would draw attention to the very consolidation that has allowed them to acquire sizable portions of the industry during a period of low production.

Confirmed Statements and Market Dynamics

The search results confirm the statements you referenced from Sam Zell and Frank Rolfe, and also support the claim of higher costs in the industry. These statements and data points collectively provide context for the criticism of an “oligopoly style monopolization” of the industry.

- Sam Zell’s Oligopoly Remark: Sam Zell, the late co-founder and chairman of ELS, did state, “We like the oligopoly nature of our business” during a 2012 conference call. This quote has been widely reported and is cited by critics as evidence that consolidation is a deliberate business strategy to limit competition. You can find this quote cited in a report from The Guardian here:

- Frank Rolfe’s Stance on New Communities: Frank Rolfe, a major community operator and MHI member, has stated that no new communities should be developed. He is also famously quoted in a Time Magazine article as saying, “It’s like owning a Waffle House where the customers are chained to the booths,” in reference to the low mobility of manufactured homes. This position on limited new supply is seen by critics as a strategy to increase demand for existing communities and justify rent hikes, which is a key characteristic of an oligopolistic market. You can find this quote here:

- Rising Costs and Oligopoly: There is data and analysis that suggests costs in the manufactured housing industry are rising faster than the general rate of inflation, which may be a classic sign of an oligopoly. A report mentions that lot rents have “nearly doubled over the last decade” and attributes the sharp spike in both lot rents and new home prices to an “oligopoly style monopolization.” This aligns with economic theory where a few dominant firms control pricing and supply, leading to higher costs for consumers and reduced production, as is the case in the manufactured housing industry since the late 1990s.

— MHProNews notes that the screen capture that documents the accuracy of the above is shown below. —

More evidence on that lack of pushback from ‘the consolidators‘ of the industry further below.

13) But as our publications previously reported, regarding the same year that the Williams “tying” letter was reportedly issued by fax, email (think RICO laws and “the wires”) and by other means, Warren Buffett said the following in his annual letter. Extended quotations from that Buffett letter are warranted for context. Note that Berkshire classified Clayton (and their affiliated lending, i.e.: 21st and Clayton’s captive lender, Vanderbilt Mortgage and Finance (VMF)) under “finance and financial products.”

Finance and Financial Products

Our largest operation in this sector is Clayton Homes, the country’s leading producer of modular and manufactured homes. Clayton was not always number one: A decade ago the three leading manufacturers were Fleetwood, Champion and Oakwood, which together accounted for 44% of the output of the industry. All have since gone bankrupt. Total industry output, meanwhile, has fallen from 382,000 units in 1999 to 60,000 units in 2009.…

The industry is in shambles for two reasons, the first of which must be lived with if the U.S. economy is to recover. This reason concerns U.S. housing starts (including apartment units). In 2009, starts were 554,000, by far the lowest number in the 50 years for which we have data. …

Our country has wisely selected the third option, which means that within a year or so residential housing problems should largely be behind us, the exceptions being only high-value houses and those in certain localities where overbuilding was particularly egregious…

The second reason that manufactured housing is troubled is specific to the industry: the punitive differential in mortgage rates between factory-built homes and site-built homes. Before you read further, let me underscore the obvious: Berkshire has a dog in this fight, and you should therefore assess the commentary that follows with special care. That warning made, however, let me explain why the rate differential causes problems for both large numbers of lower-income Americans and Clayton.

The residential mortgage market is shaped by government rules that are expressed by FHA, Freddie Mac and Fannie Mae. Their lending standards are all-powerful because the mortgages they insure can typically be securitized and turned into what, in effect, is an obligation of the U.S. government. Currently buyers of conventional site-built homes who qualify for these guarantees can obtain a 30-year loan at about 5 1⁄4%. In addition, these are mortgages that have recently been purchased in massive amounts by the Federal Reserve, an action that also helped to keep rates at bargain-basement levels.

In contrast, very few factory-built homes qualify for agency-insured mortgages. Therefore, a meritorious buyer of a factory-built home must pay about 9% on his loan. For the all-cash buyer, Clayton’s homes offer terrific value. If the buyer needs mortgage financing, however – and, of course, most buyers do – the difference in financing costs too often negates the attractive price of a factory-built home.

Last year I told you why our buyers – generally people with low incomes – performed so well as credit risks. Their attitude was all-important: They signed up to live in the home, not resell or refinance it. Consequently, our buyers usually took out loans with payments geared to their verified incomes (we weren’t