Mark Weiss, J.D., President and CEO of the Manufactured Housing Association for Regulatory Reform (MHARR) provided this advanced copy of a report they will release to their mailing list on 1.24.2022. It is part of Weiss’ “Issues and Perspectives” series and is on the topic of “Where is the ‘Equity’ for Manufactured Homes and Consumers Of Affordable Housing?” This will be followed by some related information, MHProNews analysis and commentary in brief.

MHARR – ISSUES AND PERSPECTIVES

BY MARK WEISS

JANUARY 2022

“WHERE IS THE ‘EQUITY’ FOR MANUFACTURED HOMES AND CONSUMERS OF AFFORDABLE HOUSING?”

The Biden Administration, this month, marks its first full year in office. As one of his initial steps, President Biden announced that the concept of “equity” – economic equity and, most especially, racial equity – would be a bedrock foundation for his Administration’s policies and programs. In Executive Order 13985 (“Advancing Racial Equity and Support for Underserved Communities Through the Federal Government”), issued on January 20, 2021, “equity” is defined as “the consistent and systematic fair, just and impartial treatment of all individuals, including individuals who belong to underserved communities that have been denied such treatment … persons who live in rural areas; and persons otherwise adversely affected by persistent poverty or inequality.” (Emphasis added). That such “equity” principles, under the Biden Administration, can and do apply to all aspects of housing, is made clear by a follow-up presidential memorandum issued just days later, on January 26, 2021. That document states, in part: “racial inequality still permeates land-use patterns … and virtually all aspects of the housing markets.” (Emphasis added). As a result, the memorandum directs federal agencies to “eliminate racial bias and other forms of discrimination in all stages of home-buying and renting … and secure equal access to housing opportunity for all.” (Emphasis added).

A key issue for the HUD Code industry following a full year of the Biden Administration, then, is where do manufactured homes and manufactured housing consumers stand with respect to the concept of “equity” and the application of “equity” principles? The short and unacceptable answer (for now), is “nowhere.” Sadly, and despite two outstanding laws that should have ended structural discrimination against manufactured homes, manufactured homebuyers and manufactured homeowners years ago, the Administration’s “equity” policies have yet to be applied by federal agencies and Biden Administration officials within the manufactured housing market. The result is not only an absence of “equity” for those affected, but a continuing severe shortage in the supply and availability of affordable housing and, more specifically, affordable manufactured housing, accessible to Americans of “all” races at “all” income levels, in direct violation of President Biden’s stated policies and objectives.

How and where, then, do equity principles need to be applied to benefit Americans seeking (and needing) access to affordable manufactured housing that is comprehensively regulated by the federal government? As industry members and consumers of affordable housing are all too aware, despite modest signs of recovery, the manufactured housing market has been suppressed far below historic production levels for well over a decade and continues to lag behind the broader single-family housing market, which has seen substantial growth in recent years. As MHARR has repeatedly emphasized, the primary reasons for this utilization and growth gap between manufactured housing and other types of single-family housing, are both rooted in the continuing failure of the industry’s post-production sector. Those factors, as confirmed by a 2018 Urban Institute study authored by former HUD Principal Deputy Assistant Secretary Edward Golding and newly-installed Ginnie Mae President Alanna McCargo, are: (1) continuing and ongoing discrimination against manufactured housing consumers at the federal level with respect to home purchase financing; and (2) continuing and ongoing discrimination against manufactured housing homeowners with respect to zoning and home placement.

Interestingly, the conclusions of these housing experts — Mr. Golding and Ms. McCargo — correspond with, and (again) confirm, initial MHARR research and analysis for its upcoming White Paper seeking answers and solutions relating to the exploitation of federal housing funding and assistance for purely public relations purposes by ostensible representatives of the industry’s post-production sector. This White Paper will provide long-needed answers as to why so many federal housing programs which nominally include HUD Code manufactured housing by name, are rarely if ever funded and used to support and promote manufactured housing in the field. More on this, though, when the final White Paper is completed and published soon.

For present purposes, the factors cited by Mr. Golding and Ms. McCargo – actually, policy failures – have worked to exclude millions of lower and moderate-income Americans, including large minority populations, from not only the manufactured housing market, but from homeownership altogether, as mainstream manufactured housing continues to be the nation’s most affordable source of non-subsidized housing and home ownership. And while both of these matters fall squarely within the scope of President Biden’s “equity” agenda pertaining to housing and the housing markets, there has been, thus far, no meaningful improvement or change in direction regarding either at the federal level.

Focusing first on the application of equity principles within the manufactured home consumer financing market (zoning discrimination and equity will be addressed in a future column as well as in MHARR’s detailed White Paper), the failure to infuse equity considerations and policies within the implementation of the Duty to Serve Underserved Markets (DTS) provision of the Housing and Economic Recovery Act of 2008 (HERA) is a major policy failure that continues to harm minorities and lower-income populations within the manufactured housing market, as confirmed by the most recent data and analysis published by the Consumer Financial Protection Bureau (CFPB).

DTS, of course, directs Fannie Mae and Freddie Mac to provide securitization and a secondary market support for certain historically underserved markets, including HUD Code manufactured housing and the personal property/chattel loans which finance the vast bulk of manufactured housing purchases. If fully implemented on a market-significant basis, DTS would result in lower interest rates on manufactured home consumer loans. By securitizing and providing a secondary market for those loans, Fannie Mae and Freddie Mac would lower the degree of risk borne by loan originators and holders, and simultaneously draw new lenders into the manufactured housing consumer finance market. Lower risk coupled with increased competition would invariably lead to lower interest rates than are charged today. This, in itself, would result in a greater number of qualified and approved borrowers, a larger number of manufactured home loans actually made, and a greater number of manufactured homes sold and available to address the nation’s affordable housing crisis.

Conversely, in the absence of DTS-based market-significant securitization and secondary market support for manufactured housing consumer loans – and the absence of any DTS support whatsoever for the personal property loans that comprise nearly 80% of the manufactured housing purchase financing market – manufactured homebuyers in general and minority-group manufactured homebuyers in particular, are harmed in multiple ways as corroborated by CFPB data and analysis.

- First, the absence of broad securitization and secondary market support within the manufactured home consumer lending sector needlessly limits the number of lenders operating within that sector, rendering the entire sector less competitive with respect to interest rates than would be the case in a fully-competitive market.

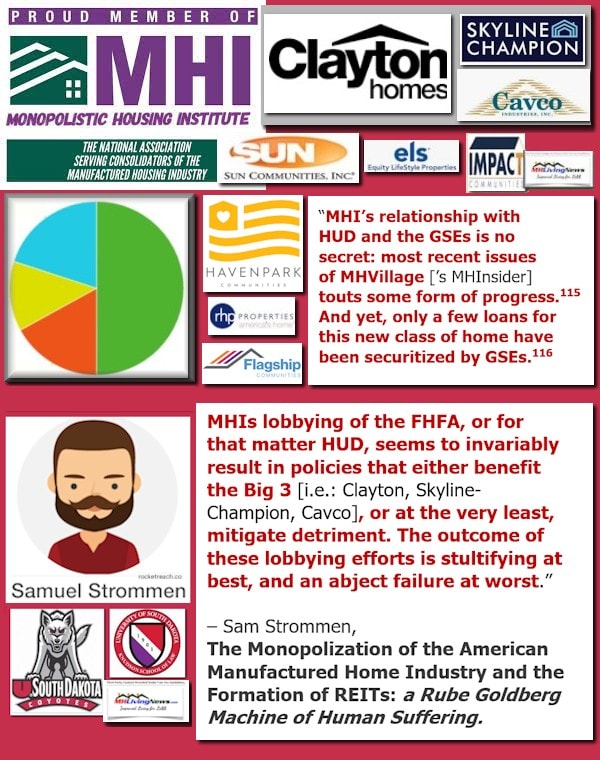

This is confirmed by a May 2021 CFPB report specifically documenting the concentration of manufactured home consumer lending within a very small number of market-dominant lenders. The report thus notes that the two most dominant manufactured housing lenders, “21st Mortgage and Vanderbilt [Mortgage Corporation] … both subsidiaries of Clayton Homes,” control a “combined 30 percent of the manufactured housing market, including 56 percent of chattel lending….” (Emphasis added).

- Second, higher-than-necessary interest rates for manufactured home purchase loans in the absence of DTS support and a less-than-fully-competitive lending market, particularly within the personal property/chattel sector, needlessly exclude significant numbers of borrowers who might otherwise qualify for purchase financing if interest rates and corresponding monthly payments were lower.

This is again confirmed by the May 2021 CFPB report, which shows that only a small “minority (27 percent) of consumers who applied for a loan to buy a manufactured home succeeded in obtaining financing.” By contrast, “an estimated 42 percent of all manufactured home purchase applications were denied, including 50 percent of chattel applications….” (Emphasis added). This compares with a denial rate of “only 7 percent” for site-built home purchase loan applications.

- Third, such market exclusion and higher interest rates, particularly for HUD Code personal property loans, disproportionately impact and harm minority purchasers.

The May 2021 CFPB report specifically states that: “Hispanic white, Black and African American, and American Indian and Alaska Native borrowers make up larger shares of chattel loan borrowers than … among site-built loan borrowers” and that “Black and African American borrowers are … over-represented in chattel lending….” Combining this with the other datapoints and conclusions noted above, the CFPB analysis proves that African Americans and other minorities, under existing Fannie Mae and Freddie Mac policies concerning the implementation of DTS (as approved thus far by the Federal Housing Finance Agency-FHFA), are – and continue to be — disproportionately harmed.

Nor is this harm confined to the policies of FHFA, Fannie Mae and Freddie Mac with regard to private loans. In addition to DTS, federal law – i.e., the Title I Federal Housing Administration (FHA) manufactured home loan program — mandates federal government support for manufactured home personal property loans. Years ago, this program supported the origination of tens-of-thousands of manufactured home purchase loans – securitized by the Government National Mortgage Association (Ginnie Mae) – annually. In 2010, though, Ginnie Mae adopted its egregious “10-10” rule regarding qualifications for Title I lenders, and the bottom fell out of Title I originations which, today, are virtually non-existent. Effectively, then, there is no federal government support for manufactured home lending – either public or private – leaving potential homebuyers with virtually nowhere to go except the market-dominant higher-rate lenders, if they can qualify for any loan at all.

Ultimately, then, the failure of FHFA, Fannie Mae and Freddie Mac to implement DTS with respect to manufactured housing chattel loans, together with the parallel failure of FHA and Ginnie Mae to fully implement the Title I manufactured housing program, has allowed an economically-distorted, less-than-fully-competitive, systemically-discriminatory structure within the manufactured housing personal property lending market — with identifiable and quantifiable adverse impacts on racial minorities and other disadvantaged Americans — to remain in place, with no real effort, thus far, from the Biden Administration (assuming it is even aware of these issues due to the ongoing deficient representation of the post-production sector in Washington, D.C.) to remedy that failure through the application of equity principles and concepts.

There may be reason for hope going forward, given the recent elevation of Sandra Thompson and Alanna McCargo to serve as the Director of FHFA and President of Ginnie Mae respectively. MHARR has had – and continues to have — a positive dialogue with Ms. Thompson regarding the need for chattel loan DTS support. When Ms. Thompson served as FHFA Assistant Director, she spent a significant time meeting with MHARR and MHARR member manufacturers to understand the damage to the industry and consumers resulting from Fannie Mae and Freddie Mac’s failure to provide robust, market significant securitization and secondary market support under DTS for manufactured home consumer loans. And, as previously noted, Ms. McCargo is on record as acknowledging the destructive impact of financing discrimination on the availability of affordable, non-subsidized manufactured housing. Perhaps such leaders, with specific previous knowledge of the manufactured housing industry and effective pressure from the industry, can produce real change.

As the old saying goes, however, “hope” is not a strategy. The industry faces serious challenges within its post-production sector. Nothing will change, though, unless and until the industry decides that it is serious about change – and that ultimately means aggressive, independent national representation for the post-production sector in Washington, D.C. in order to correct these (and other) deficiencies that have harmed both the industry and American consumers of affordable housing. ##

Mark Weiss

MHARR is a Washington, D.C.-based national trade association representing the views and interests of independent producers of federally-regulated manufactured housing.

###

Additional Information, More MHProNews Analysis and Commentary

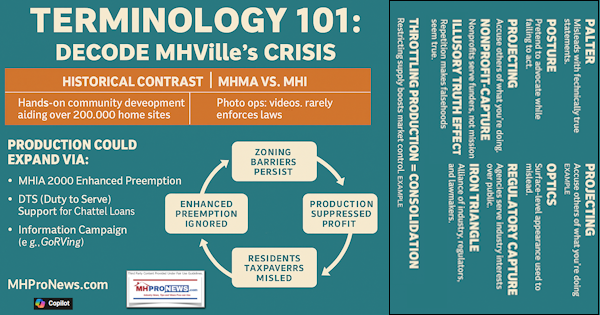

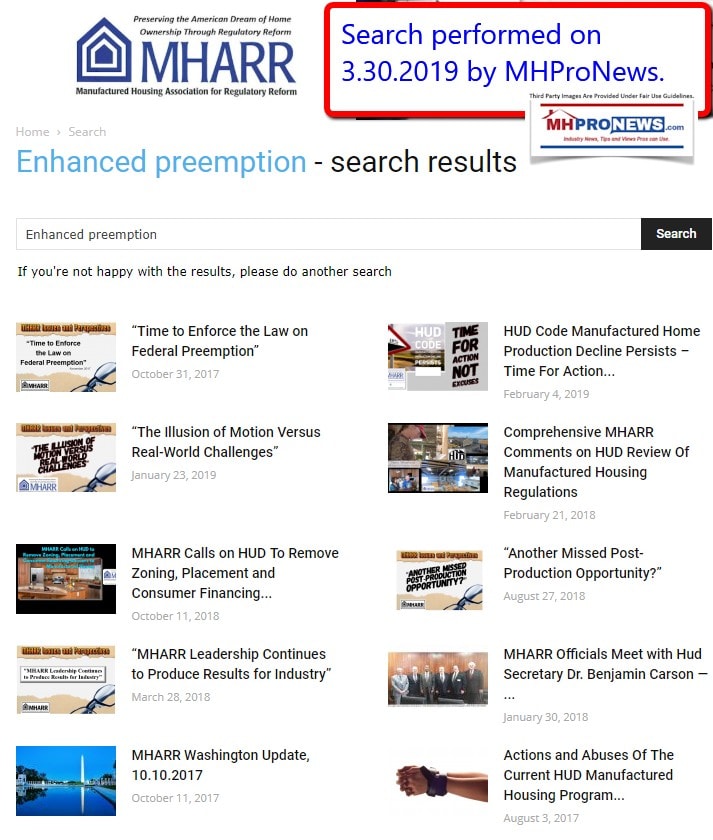

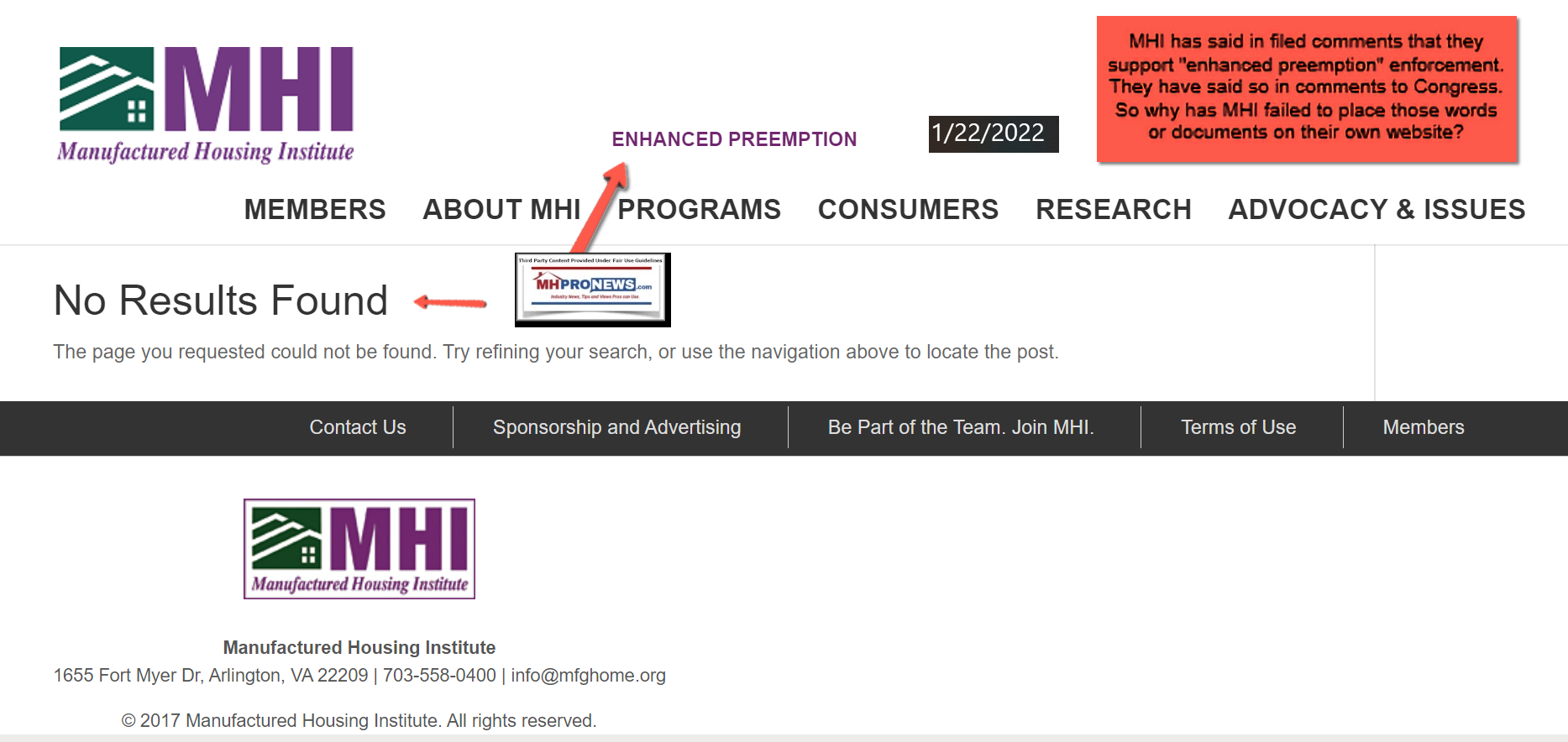

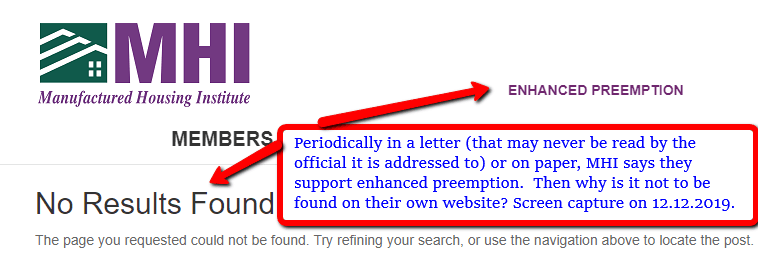

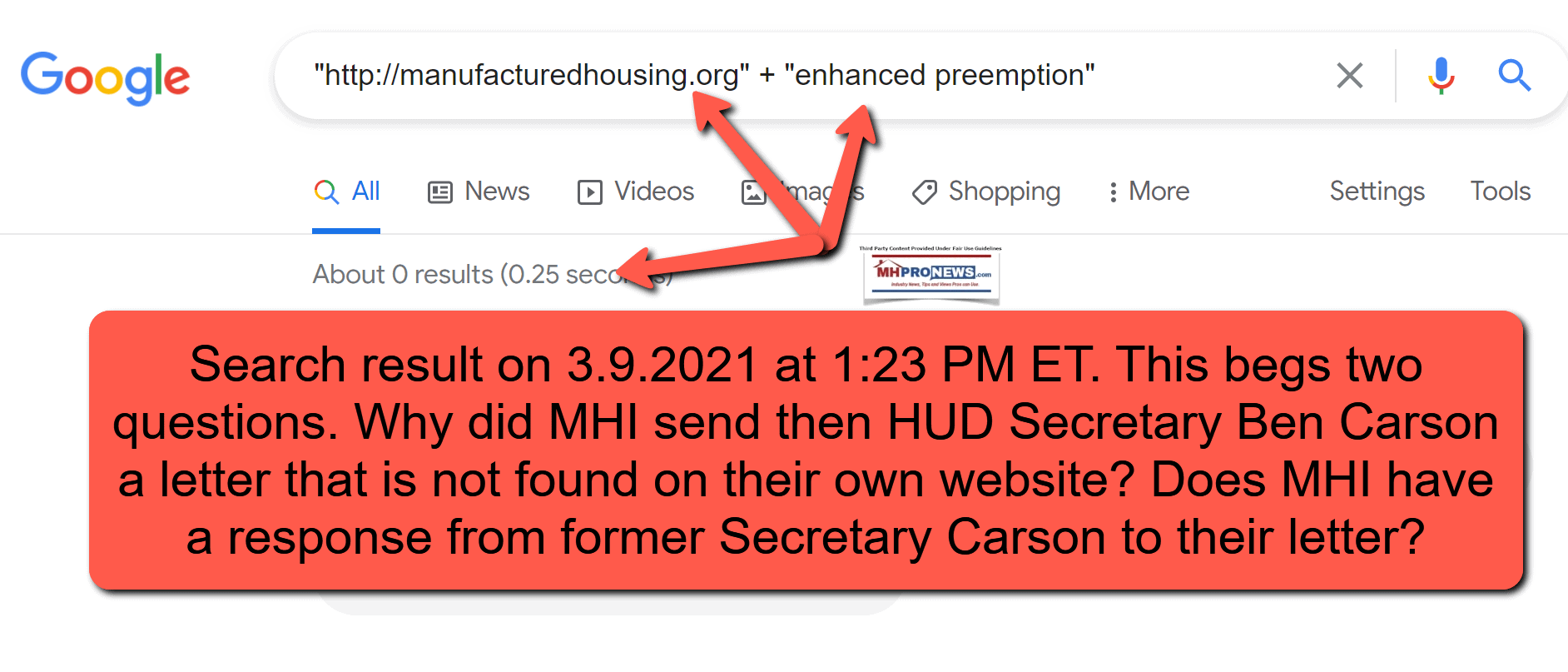

No article is entirely compete – ours or anyone else’s – for several reasons. One is the time/length/benefit equation. A 2000-word article, such as Weiss’, can and does cover a lot of ground. He referenced by implication the Manufactured Housing Improvement Act of 2000 (MHIA and/or 2000 Reform Law), without explicitly identifying it and the so-called “enhanced preemption” provision in it. That said, compared to the Manufactured Housing Institute (MHI), MHARR is head and shoulders ahead of MHI in its use of the terminology on their own website and in other writing too.

This visual evidence snapshots and related quotes tells that tale.

On this date (1.23.2022) there are 16 specific articles that uses the phrase – “enhanced preemption” – on the MHARR website, per the MHARR website search tool.

By contrast, the MHI website – backed by a staff and budget that is many times that of MHARR – has NO, zero, zip, nada – mention of the phrase “enhanced preemption.” This despite the fact that MHI has been online perhaps 4+ times longer than MHARR.

Indeed, the case can be made that MHARR launched their website due to what Weiss alluded to about MHI’s lack of delivery on issues they claim to support: “rooted in the continuing failure of the industry’s post-production sector.” As a side note, the MHARR website will turn 5 in a few months.

- Perhaps out of politeness or for the sake of length, etc., Weiss doesn’t mention Lesli Gooch’s missive on equity and manufactured housing which MHProNews What Gooch hasn’t said is that when she and MHI were asked to weigh in on the issues of black Rev. Ivory Mewborn, Mayor Pro-Tem of Ayden, N.C., MHI didn’t even bother to respond. By contrast, MHARR’s Mark Weiss – on an issue that is a post-production, not a production related issue – confirmed for Ayden officials the concerns raised by this writer on behalf of Mewborn and the Taft family. Restated, Weiss acted. Gooch and MHI postured, and per local sources, didn’t act. Weiss cites the CFPB and Clayton Homes, which MHProNews and MHLivingNews unpacked in reports such as the one linked here. Racial equity was part of our platforms’ analysis then too.

- While MHI is sending out two or three sentence length on a given MHI ‘news and updates’ topic – vs. far longer pitches for MHI profit centers (meetings, etc.) – MHARR provides in depth reports to anyone that signs up for their emails. MHARR also makes republishing their content reasonably easy. Not so MHI. Those facts and evidence speak volumes.

- There are several additional examples possible. Certainly, the issues raised by Samuel “Sam” Strommen at Knudson Law should be mentioned. Or the fact that numbers of publicly traded firms in manufactured housing – which are often MHI members – openly state in investor relations presentations that their goal is to “consolidate” a “fragmented” manufactured home industry through “mergers and acquisitions.” An exception to this is MHI member Legacy Housing. But generally, others have been quite clear in words and deeds. So, how then does someone explain the notion that MHI postures efforts at growth, but has failed to accomplish their own stated goals for some 13+ to 21+ years? When someone looks at the MHI board of directors, it often has some of those very consolidating firms on it. Ironically, MHI’s new chairman – Leo Poggione – is a retailer who has been partially acquired by Cavco Industries. The balance of his Craftsman Homes business is per the SEC website scheduled to become Cavco’s in the coming years. Logically, if the industry was growing in a robust fashion, would ‘consolidation’ of a growing industry be as easily accomplished and as such a relatively low price as when the industry is underperforming? Underperformance, in other words, benefits consolidators. The day may come when they take their collective foot of the break peddle slowing manufactured housing down. Or, given Clayton’s and Berkshire Hathaway’s apparent stakes in conventional housing, they might leave the HUD Code entirely behind in favor of modular, 3D printing, or something else in the way of prefab/”off-site built homes.” They could pivot in a range of possible directions, when it suits them. The links below provide the evidence for those concerns. Nor has Berkshire, Clayton, MHI, or others in the mix denied such claims when asked.

England has announced they are rescinding several of the mandates that have been in effect. The ‘pandemic’ is possibly shifting to the ‘endemic’ stage, more like the common flu. Meaning, the population simply accepts it as part of everyday life and will live with it. America, along with other nations, has witnessed during the perhaps fading COVID19 pandemic a sharp rise in the wealth and clout of big brands and leading billionaires. It is often the same groups that are profiting that have clear corporate and/or financial ties with major media and big tech companies. That need not be conspiratorial in the ordinary sense. It can be as simple as fellow travelers who happen to think alike, a point raised by former Secretary of the Interior, James Watt. But regardless if it is happenstance or a sly scheme hatched years ago, as some allege, the effect could be what is being witnessed.

The U.S. Chamber of Commerce went through its own cathartic phase when smaller businesses recognized that “the Chamber” was being dominated by the larger ones. Ex-Chamber executive Dr. Richard Rahn, Ph.D., has said as much. The National Federation of Independent Business (NFIB), the Jobs Creators Network (JCN) and others exist as counterweights to the U.S. Chamber. MHARR – a production focused trade groups – exists as a counterweight to MHI. MHARR has for well over a decade been calling on the ever-shrinking numbers of post-production independents to forge a new post-production trade group.

What is coming in their White Paper is not yet known. But MHARR’s in depth studies on topics such as the DOE energy rule and in favor of a post-production trade group have been deeply considered reflections of reality. In the wake of their post-production report, the National Association of Manufactured Housing Community Owners (NAMHCO) came into being. While it was arguably neutralized in part by NAMHCO hiring an ex-MHI VP and then inexplicably (to some) partnering with MHI after ripping them is not inconsequential but is best seen as an effort by MHI to keep such a group from gaining traction. NAMHCO validates the concept and provides lessons of what not to do. That’s not a slam on NAMHCO’s leaders, it is an evidence-based and objectively supported conclusion. NAMHCO showed it can be done. They are to be applauded for that, not minimized.

MHARR breathes much of the same rare air that is Washington, D.C. that MHI does from the opposite bank of the Potomac River. They get insights that some outside of that “Washington Beltway” do not normally have.

It is for an array of reasons that modest in size but mighty in effort MHARR merits ongoing attention. They are the primary nonprofit at this time pressing for growth in common sense ways. Unlike some that want to play gatekeeper, MHARR has long invited others to rise up and work with them. It is in some ways David (MHARR) vs. Goliath (MHI). That said, all analogies limp at some point. Note that MHARR has not called for MHI’s abolition. Rather, they have de facto called on MHI to pivot toward their stated mission by suing to get enforcement on the laws that MHARR and MHI jointly shepherded into existence.

In the battle for equity is in good measure a racial issue. It is also a justice issue for numbers of others, minority or not, that are employed in America or have a smaller business in the U.S. The late Martin Luther King Jr. wanted to foster a coalition that was multi-ethnic, including all of those who are disadvantaged, not just blacks or Hispanics. King wanted whites too, who were a key part of his civil rights efforts.

When examining how MHI has looked in recent years, it is worth noting that the MHARR office is far more diverse than MHI has ever been. If MHI is serious about their claims, MHARR seems to say, it is time for them to step up to the plate and do their job. MHI has to walk the talk. Otherwise, talk is not only cheap, but it is also harmful to those who are being left behind by the status quo that benefits a few at great harm to the many. ##

###

[cp_popup display=”inline” style_id=”139941″ step_id = “1”][/cp_popup]

Stay tuned for more of what is ‘behind the curtains’ as well as what is obvious and in your face reporting that are not found anywhere else in MHVille. It is all here, which may explain why this is the runaway largest and most-read source for authentic manufactured home “News through the lens of manufactured homes and factory-built housing” © where “We Provide, You Decide.” © ## (Affordable housing, manufactured homes, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.) (See Related Reports, further below. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHProNews.com.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing.

For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com.

This article reflects the LLC’s and/or the writer’s position, and may or may not reflect the views of sponsors or supporters.

Connect on LinkedIn: http://www.linkedin.com/in/latonykovach

Related References:

The text/image boxes below are linked to other reports, which can be accessed by clicking on them.