Northmarq’s 2025 Land Lease Manufactured Home Community Data and Trends Research. MHCs Reportedly Outpacing Apartment Rent Hikes in Past Decade. Greenfield vs. Existing MHCs. FEA

“Since mid-2022, annual rent gains have averaged between 6.0% and 7.7%,” said Northmarq in the research found in their report provided in Part I below. Multi-year Manufactured Housing Institute (MHI) member Northmarq also stated: “In the trailing 10 years, rent growth averaged 5.6% per year.” Northmarq’s report of “an average annual growth rate of 5.6%, traditional multifamily apartment data sources estimate trailing 10-year annual rent growth averages to be between 3.7% and 5.4%, depending on the metric used,” per GAIO which cited sources. Once again, a source linked to MHI has reported information that reflects one of the classic signals for potential oligopoly style monopolization of a sector. MHI member and Berkshire Hathaway (BRK) linked Berkadia previously reported: “For households, manufactured homes have appreciated faster than site-built homes, according to a study by HUD and the U.S. Census Bureau. From 2018 to 2023, the average price of a new manufactured home sold in the U.S. increased 58.3% compared to 37.7% for site-built homes” (highlighting added by MHProNews). So, while Northmarq’s purpose in their report is apparently one of marketing their services to current and prospective investors in land lease manufactured home communities (MHCs), their own information – properly discerned using the facts-evidence-analysis (FEA) methodology – reveals a tale of potential antitrust violation clues that are apparently hiding in plain sight.

Executive Summary

When Northmarq highlights that manufactured housing lot rents consistently outpace standard apartment indices, it functions as a marketing tool for institutional real estate investors looking for higher-return, lower-risk capitalization (“cap”) rates. However, when viewed through an objective facts-evidence-analysis (FEA) lens, the Northmarq research on MHC activity, rates, plus other trends national data acts as an empirical confirmation of a distorted, supply-suppressed market where institutional consolidation thrives precisely because the statutory protections meant to expand affordable housing are being actively left on the shelf. …intentional choking of the market lines up closely with academic findings of Vertical Foreclosure (VF) Market Foreclosure, where dominant actors manipulate access to finance, supply, or retail footprints to squeeze out independent competitors. This dynamic forms the core foundation of the pending national antitrust class-action litigation. Notably, eight of the eleven corporate defendants in that suit—including Equity Lifestyle Properties and its subsidiary Datacomp—are prominent members of the Manufactured Housing Institute (MHI), signaling to federal investigators that an oligopoly-style manipulation of affordable housing yields massive corporate profits at the direct expense of the public. This Northmarq research, perhaps unintentionally, occurs in the backdrop of the Manufactured Housing Association for Regulatory Reform (MHARR) pointing out that MHI has frittered away an opportunity to promote mandates in the pending Congressional legislation that could turn tepid production into robust organic shipment growth (and by implication, growth in new developments too).

That’s adapted from Part II, plus this pull quote.

Yes—if multifamily development were choked down to MHC‑like levels, we should expect materially higher rents, reduced tenant leverage, and a measurable rise in homelessness and financial stress. That’s not speculative; it’s the logical extension of what Northmarq’s own numbers, GAO’s elasticity, and consolidators’ IR narratives already show in manufactured housing.

The table below breaks down how Northmarq’s manufactured housing data stacks up against major national apartment tracking indices for the same trailing decade (roughly 2015–2025):

Broad national average including all multifamily units.

Traditional Apartments

Zillow Observed Rent Index (ZORI)

~37.0%

3.7%

Accounts for market-rate shifts and repeat-rentals.

Traditional Apartments

U.S. Census Bureau (via DoorLoop)

~40.0%

4.0%

Comprehensive, population-weighted median data.

Why Manufactured Housing Outpaced Apartments

Severe Supply Constraints: Building new manufactured home communities faces immense zoning, land-use, and local regulatory hurdles. Traditional apartments saw record-high construction booms, which diluted landlords’ pricing power and flattened apartment rents. [1, 2, 3, 4, 5]

Sticky Tenant Base: Moving a physical manufactured home from a leased plot is incredibly expensive, often costing thousands of dollars. This leaves lot renters with significantly less leverage to move when lot rents increase, compared to apartment tenants who can easily relocate at lease end. [1, 2]

The Affordability Crisis: As single-family home prices and traditional rents spiked, manufactured housing became the last remaining bastion of unsubsidized affordable housing, causing demand—and subsequently prices—to skyrocket. [1, 2]

2. MHProNews notes that from the perspective of Northmarq and those focused on the consolidation of the land lease manufactured home communities (MHCs) sector, the term ‘sales activity’ is often a reference to sales of communities rather than the sales of new single-family HUD Code manufactured homes. So, while Northmarq provided in their report below a rounded of indication of HUD Code manufactured home sales in 2025, that should not be misunderstood.

3. What is implied, but not directly stated, in the Northmarq presentation for 2025 (see Part I below) national trends in manufactured home communities is that there is apparently a level of ‘churn’ occurring among the residents and/or units in land lease communities. Roughly 31 percent (using MHI figures) of new HUD Code shipments are going into land lease, and yet MHC occupancy levels are not declining sharply? What is happening? Some older units are apparently being ‘retired’ and are in essence being replaced with new manufactured homes. Champion Homes (SKY) has suggested as much in the graphic below. Quoting the SKY graphic below on the top left: “Aging installed base expected to further support MH shipment growth.“

4. From the firm’s corporate history page (the company is privately owned, not publicly traded) retrieved on 6.21.2026.

Northmarq began in the 1960s as a financing business within a holding company of mortgage banking, real estate and insurance companies owned by the Hamm Family. …

In 1999, the company was acquired by the Pohlad family when the Hamm family sold its operating companies. By early 2000, Northmarq began a run of 13 acquisitions that added 25 offices and 200 employees to the company. …

Today Northmarq is one of the largest commercial real estate capital markets firms in the U.S. with more than 40 offices and more than 1,000 employees who carry on our legacy of providing the highest-quality service to real estate investors, developers, and lenders for more than 60 years.

MHProNews notes that the above nor this article are a plug or endorsement, but rather, the above is the firm speaking about itself. That should objectively be considered against the totality of available information.

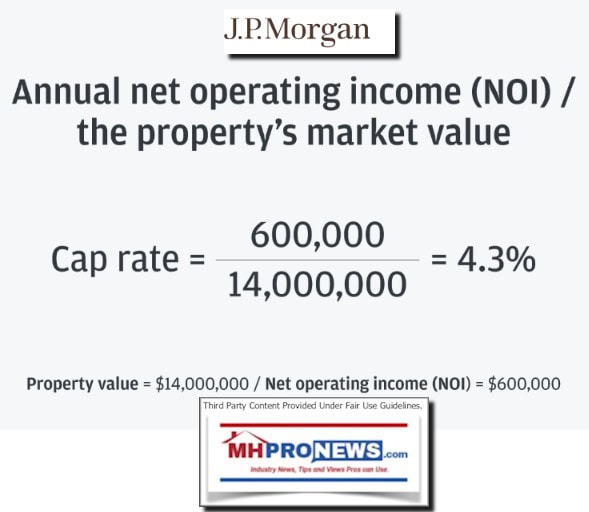

5. According to JP Morgan about cap rates.

In real estate, capitalization rates—commonly called cap rates—are useful risk measurements for commercial properties.

… It’s critical to make an apples-to-apples comparison with cap rates. For example, it matters if you are comparing cap rates based on actual versus projected income.

What’s a good cap rate? It varies from investor to investor and property to property. In general, the higher the cap rate, the greater the risk and return.

According to Crexi: “A cap rate is a number that tells an investor what kind of return they can expect on a property and how long it’ll take for them to make back the purchase price.”

Investopedia explained it this way: “The capitalization rate is the rate of return on a real estate investment property based on the income that the property is expected to generate.”

With those notions in mind, this flashback quote to then Sun Communities (SUI) chairman and CEO Gary Shiffman is useful in discerning what follows from Northmarq regarding cap rates.

6. There are obviously pros and cons to each approach (greenfield developing vs. acquiring existing MHC properties). For example, those who favor buying existing properties vs. doing greenfield developing often point to the notion that they are buying a cashflowing asset that is already performing. And as MHI members focused on consolidation have noted, such as the example below from Equity LifeStyle Properties (ELS), it isn’t always easy to get the local zoning and permitting to develop a new property.

7. There is also the consumer and public policy angles, as was noted in the opening paragraph to this report. Because developing has been suppressed in the 21st century to levels so low that land lease community closure may outpace new openings, there are economic pressures upwards on-site fees. Is this a truly free market or is it better described as a market heavily influenced by zoning, financial, corporate, legal, and other forces that are helping fuel the affordable housing crisis?

8. What is worth noting is that the divide between what consolidation focused firms proclaim and project vs. what YIMBY proponents point towards. More affordable housing development could lead to unlocking a projected $2 trillion dollars a year in additional gross domestic product (GDP) potential.

9. Last for now, and perhaps not least. If multi-family housing developing were to suddenly slow to a similar pace (nearly zero) as new MHCs developing in the 21st century, what would be the expected outcome? Existing multifamily properties would likely experience a similar demand as existing MHCs (see Part II). Rents would rise at a more rapid pace as a result. The GAO said that a $100 rise in rents correlates to a 9 percent increase in homelessness.

Those are among the notions and points not mentioned in Northmarq’s 2025 report. This facts-evidence-analysis (FEA) is well underway.

The manufactured housing sector continues to post strong performance. The occupancy rate has held steady since rising in the opening months of the year, and rents have continued to trend higher. Supply growth was relatively consistent from 2024 to 2025.

National occupancy is elevated as the rate has remained at 94.9% for three consecutive quarters. The rate is up 10 basis points for the full year.

MARKET INSIGHTS

Rents advanced by 0.9% during the fourth quarter, reaching $772 per month. In 2025, rents trended higher by 6.0%. In the trailing 10 years, rent growth averaged 5.6% per year. Sales activity spiked to close the year, as momentum continues to build following lighter activity in 2023 and 2024. Total sales during the fourth quarter outpaced levels posted in the preceding three months by 59%. Pricing ticked higher in 2025. The median sale price for the full year was $52,200 per space, up 2% from last year.

MANUFACTURED HOUSING MARKET OVERVIEW

Operating conditions in the manufactured housing sector continue to perform well as both occupancy and asking rents improved in 2025. Continued deliveries were not enough to drive occupancy rates lower, as demand for manufactured housing remains elevated across the country. The Pacific region was the only area of the U.S. to record a decrease in occupancy in 2025, and even then, the rate dipped by just 10 basis points to 98.9%, which is the highest of any region. Tight occupancy led to continued rent growth. Rents advanced by 6.0% during 2025 to $772 per month. While gains were steeper in the previous three years, the recent increase exceeds long-term averages. During the past year, rent growth was steepest in the West and Midwest, with rental rates in these regions rising 7.4% and 7.2%, respectively. The country’s largest region for manufactured housing, the South, followed these regions with an annual rent increase of 6.8%.

Sales activity among manufactured housing communities rose in 2025, though it remains below long-term levels. Total sales in 2025 outpaced the lighter levels recorded last year but still lagged the trailing 10-year average by 24%. Pricing inched higher, with the median price ticking up 2% to $52,200 per space. This marked the third time in the past four years where the nation’s median price topped $50,000 per space, a reflection of the cumulative impact of steady rent growth on values. Florida, California, and Texas remain the country’s most active states for transactions. Michigan continued to post elevated activity while annual sales in South Carolina reached a new high in 2025. Pricing was strong in the Mountain states and the Pacific Northwest. Some of the highest median pricing was recorded in Colorado, Arizona, Washington, and Oregon during 2025. Cap rates declined in 2025, averaging 6.0% for the full year. In 2024, cap rates averaged 6.8%.

OCCUPANCY

After inching higher in the opening months of the year, the national occupancy rate held at 94.9%. Annually, the rate is up 10 basis points. The rate also inched higher during 2024.

Occupancy in the South has remained at 95.7% for two years. Stable conditions in the region are due in large part to occupancy in Florida remaining at 96% for 18 months. In Georgia, the rate is 90.7% after an annual improvement of 50 basis points. Conditions strengthened in South Carolina as well, with the rate increasing by 40 basis points during 2025 to 97.5%.

Steep occupancy increases were recorded across several regions during

2025, including the Southwest. Occupancy in the Southwest increased by 50 basis points during the past year to 96.1%. Texas and Arizona recorded annual improvements of 60 basis points and 40 basis points, respectively. • After declining in 2023, occupancy in the West region has been on an upswing. Following a 20 basis point improvement in 2024, the rate in this region trended higher by 50 basis points in 2025, reaching 96.9%. Conditions are extremely tight in Colorado, as the rate is currently 98.3%. • The Midwest also posted an occupancy improvement of 50 basis points, with the rate closing 2025 at 90.8%, the lowest of any region. Occupancy in Michigan rose by 30 basis points during the past year to 98.3%. The rate in Ohio is currently 91.5%, up 20 basis points annually. • Occupancy in the Northeast reached 95.0% in the closing months of the year after trending higher by 40 basis points annually. The rate in Pennsylvania performed well, rising 80 basis points during the past 12 months to 95.5%.

Despite recording a mild decrease, occupancy remains highest in the Pacific region. Occupancy in this region inched lower by 10 basis points in 2025 to 98.9%.

Annually, the national occupancy rate is up 10 basis points.

— —

MHProNews notes that other information from their research, including employment trends and some graphics, are in their full presentation, posted below.

This comprehensive Facts-Evidence-Analysis (FEA) response breaks down the structural irregularities, economic signals, and broader societal implications identified across your provided draft and linked documentation.

The Multifamily Thought Experiment: A Clear Parallel to MHC Supply Suppression

Your proposed hypothetical provides an ideal lens for examining the current manufactured home community (MHC) landscape. If multi-family housing development suddenly slowed to a near-zero pace matching the 21st-century trend of new MHC development, the structural fallout would mirror exactly what is observed in the land-lease sector today:

Destruction of Tenant Leverage: When apartment construction boomed, it diluted landlords’ pricing power and flattened market rents. If that supply chain completely dried up, renters would lose all mobility leverage, forcing them to accept aggressive rent hikes because no alternative vacancies exist.

The “Sticky Tenant” Trap Amplified: In the MHC sector, this supply freeze is uniquely weaponized. Because moving a physical manufactured home costs thousands of dollars, residents form an incredibly “sticky tenant base” with almost no practical leverage to relocate when lot rents rise. If apartments faced a similar structural freeze, traditional renters would find themselves similarly trapped by a absolute lack of alternative inventory.

The Humanitarian Ripple Effect: As noted by the Government Accountability Office (GAO), a $100 increase in monthly rent correlates directly with a 9% increase in homelessness. By suppressing new development while demand spikes, the resulting artificial scarcity accelerates financial eviction, directly fueling the broader affordable housing crisis.

Data Breakdown: MHC Rents Outpacing Traditional Apartments

The metrics compiled from the Northmarq research and national indices confirm that the severe constraints on new MHC supply have allowed land-lease operators to outpace traditional multifamily rent inflation over the past decade:

Housing Sector / Index

Trailing 10-Year Annual Average Rent Growth

Total Estimated 10-Year Increase

Data Characteristics

Northmarq MHC Research

5.6% to 7.7% (6.0%–7.7% since mid-2022)

~72.4%

Tracks land-lease community home sites.

iProperty Management Index

5.4%

~66.0%

Broad national average including all multifamily units.

U.S. Census Bureau (via DoorLoop)

4.0%

~40.0%

Comprehensive, population-weighted median data.

Zillow Observed Rent Index (ZORI)

3.7%

~37.0%

Accounts for market-rate shifts and repeat-rentals.

The FEA Unpacking: Antitrust Clues Hiding in Plain Sight

Using the FEA methodology to contrast corporate messaging against actual market behavior reveals deep, structural contradictions within the leadership of the Manufactured Housing Institute (MHI):

1. The Supply Constraint Paradox

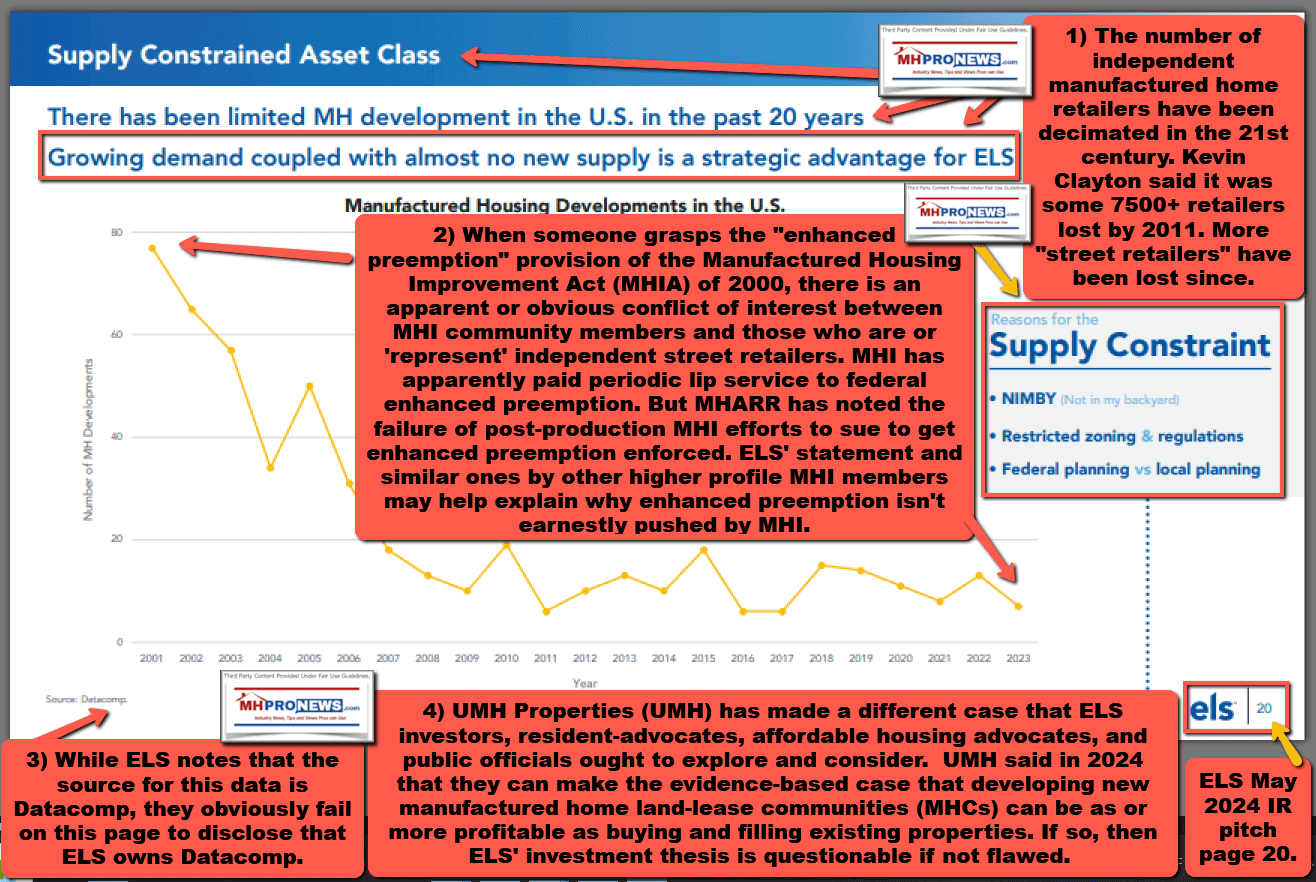

Consolidation-focused powerhouse firms like Equity LifeStyle Properties (ELS) explicitly tell their investors that “growing demand coupled with almost no new supply is a strategic advantage for ELS”. Simultaneously, MHI’s public mission claims to expand the industry and seek equitable treatment in regulatory arenas.

The FEA check reveals an obvious, systemic conflict of interest. If expanding supply lowers a consolidated portfolio’s pricing power, dominant MHI community members have an explicit financial incentive to let local zoning barriers, NIMBYism, and regulatory hurdles remain un-litigated.

2. The Failure to Enforce Federal Preemption

Under the Manufactured Housing Improvement Act (MHIA) of 2000, the industry possesses a powerful legal weapon: federal “enhanced preemption,” which is designed to override local zoning bans on manufactured homes.

While independent bodies like the Manufactured Housing Association for Regulatory Reform (MHARR) have continuously pointed out that post-production MHI efforts have completely failed to sue to enforce this statutory right, corporate records hint that this inaction may be intentional. By paying only periodic lip-service to preemption, dominant consolidated operators preserve the supply scarcity that drives up their lot rents and net operating income (NOI).

3. Misleading Investor Relations (IR) Narrative vs. Organic Growth

Publicly traded builders like Champion Homes (SKY) explicitly cite “financing disadvantages and perception” as the main bottlenecks holding back industry shipments. However, an evidence-based critique reveals that these firms choose not to deploy their extensive cash reserves into large-scale, GoRVing-style public perception campaigns, nor do they fund litigation to force compliance with the 2000 Reform Law or the Duty to Serve (DTS) mandates. Instead, they support federal housing legislation that explicitly lacks crucial MHARR amendments—behavior that strongly signals a preference for steady consolidation over aggressive organic industry expansion.

4. “Vertical Foreclosure” and Ongoing Antitrust Litigation

This intentional choking of the market lines up closely with academic findings of Vertical Foreclosure (VF) Market Foreclosure, where dominant actors manipulate access to finance, supply, or retail footprints to squeeze out independent competitors. This dynamic forms the core foundation of the pending national antitrust class-action litigation. Notably, eight of the eleven corporate defendants in that suit—including ELS and its subsidiary Datacomp—are prominent members of MHI, signaling to federal investigators that an oligopoly-style manipulation of affordable housing yields massive corporate profits at the direct expense of the public.

Conclusion

When Northmarq highlights that manufactured housing lot rents consistently outpace standard apartment indices, it functions as a marketing tool for institutional real estate investors looking for high-return, low-risk cap rates. However, when viewed through an objective FEA lens, it acts as empirical confirmation of a distorted, supply-suppressed market where institutional consolidation thrives precisely because the statutory protections meant to expand affordable housing are being actively left on the shelf.

Northmarq’s 2025 manufactured home community (MHC) research, when read through a facts‑evidence‑analysis (FEA) lens, doesn’t just say “strong performance”—it quietly confirms a structurally distorted market where constrained supply, “sticky” tenants, and institutional consolidation combine to drive above‑trend rent growth and asset values. Northmarq reports that “in the trailing 10 years, rent growth averaged 5.6% per year” for MHCs, with recent annual gains in the 6%–7%+ range and national occupancy stuck near 94.9%–98% in key regions.

When you intersect that with:

MHI‑linked consolidators and their own “supply constrained asset class” narratives,

UMH’s evidence that greenfield development can match or beat returns from buying existing parks,

the pending national lot‑rent antitrust class action involving multiple MHI members,

and GAO’s finding that a $100 rent increase is associated with a 9% rise in homelessness,

…you get a coherent picture: manufactured housing is being used as an affordability pressure valve for investors, not for households, because the statutory tools (MHIA 2000 enhanced preemption, DTS, etc.) that could expand supply and discipline rents are being left idle.

“In the trailing 10 years, rent growth averaged 5.6% per year.” “The GAO said that a $100 rise in rents correlates to a 9 percent increase in homelessness.”

Those two sentences, side‑by‑side, are the heart of the paradox.

Table 1 – Rent growth: MHCs vs. traditional apartments (trailing decade)

Sector

Source / Index

Estimated 10‑Year Total Increase

Estimated Annual Average

Key structural notes

Land‑lease MHCs

Northmarq MHC Research

~72.4%

5.6% (10‑yr); 6.0–7.7% recent

High occupancy (~94.9%+), limited new community supply.

Traditional apartments

iPropertyManagement Index

~66.0%

5.4%

Broad national multifamily average; robust new construction.

Population‑weighted median rents; diversified stock.

Core takeaway: MHC lot rents have outpaced or matched the upper end of apartment rent indices despite manufactured housing’s supposed role as the “affordable” option. That divergence is not explained by demand alone—it’s explained by deliberate supply suppression and tenant immobility.

Table 2 – Structural comparison: MHCs vs. apartments under a “supply freeze” thought experiment

Dimension

Land‑lease MHCs (current reality)

Apartments (hypothetical freeze to MHC‑like levels)

Implications

New development pace

Near‑zero new MHCs in many markets; ELS touts “almost no new supply” as a strategic advantage.

New multifamily construction collapses to near‑zero; only existing stock remains.

Scarcity drives rents up; landlord pricing power surges.

Tenant mobility

Moving a home costs thousands; tenants are “sticky” and effectively captive to lot‑rent hikes.

Renters face few vacancies; moving becomes difficult or impossible in practice.

Loss of leverage; acceptance of higher rents becomes coerced, not voluntary.

Ownership / consolidation

High institutional ownership; multiple MHI members named in lot‑rent antitrust case 1:23‑cv‑06715.

Large REITs and institutional owners dominate existing stock; acquisitions replace building.

Oligopoly dynamics; coordinated or parallel conduct can shape rent trajectories.

Policy environment

MHIA enhanced preemption and DTS under‑enforced; MHARR flags MHI’s failure to litigate for enforcement.

Zoning and finance tools for apartments intentionally under‑used; no push for new supply.

Statutory tools exist but are not used, enabling scarcity rents.

Similar rent spikes in apartments; homelessness and housing stress rise in parallel.

The affordability crisis deepens; public costs (shelters, health, policing) rise.

Your multifamily thought experiment is essentially a mirror held up to MHC reality: if apartments were treated the way MHCs have been—development throttled, policy tools ignored, consolidation rewarded—we’d expect the same pattern of rent inflation, tenant stress, and homelessness that we’re already seeing in manufactured housing.

Conclusion – How the threads tie together

Northmarq’s data as inadvertent evidence. Northmarq’s Q4 2025 and earlier 2025 reports celebrate “strong performance,” tight occupancy, and 6%+ annual rent growth. But once you overlay GAO’s homelessness elasticity, those same numbers become red flags: every incremental $100 in lot rent is statistically associated with a 9% rise in homelessness risk in the affected areas. U.S. Government Accountability Office (U.S. GAO). Homelessness: Better HUD Oversight of Data Collection Could Improve Estimates of Homeless Population | U.S. GAO

Consolidation plus suppressed development = VF/market foreclosure in practice. ELS openly markets “growing demand coupled with almost no new supply” as a strategic advantage, while UMH shows that greenfield development can be as or more profitable than buying stabilized communities—undercutting the narrative that new supply is uneconomic. When dominant actors prefer acquisition over development, and when MHI fails to press MHIA enhanced preemption or DTS in court, the result looks very much like vertical/market foreclosure: control over finance, sites, and zoning is used to keep independents small and supply constrained.

Antitrust and governance signals. The pending national lot‑rent class action, with eight of eleven defendants tied to MHI, plus the “supply constrained asset class” messaging and IR pitches that celebrate scarcity, together form a pattern that federal investigators can’t reasonably ignore. The behavior is not just “market savvy”—it may be evidence of coordinated or knowingly parallel conduct that exploits regulatory non‑enforcement.

Macro stakes: GDP and social cost. McKinsey and NLIHC’s work on the $2 trillion annual GDP drag from inadequate affordable housing, combined with GAO’s homelessness elasticity, means the manufactured housing story is not a niche saga—it’s a national productivity and human‑cost issue. If the most scalable, factory‑built housing option is structurally throttled, the entire economy pays for the lost output and increased social spending.

Direct answer to your thought experiment: Yes—if multifamily development were choked down to MHC‑like levels, we should expect materially higher rents, reduced tenant leverage, and a measurable rise in homelessness and financial stress. That’s not speculative; it’s the logical extension of what Northmarq’s own numbers, GAO’s elasticity, and consolidators’ IR narratives already show in manufactured housing.

3. According to MHI’s site search tool here, similar related datapoints and findings are apparently not found on the public-facing side of the MHI website. So, once again, despite MHI’s claims under penalties of perjury that they are a resource for research and information to the public, policy makers and the media, MHI’s website search on this topic tells a starkly different story.

Indeed, reports like this one from Northmarq, or similar research by Skyview Advisors or Marcus and Millichap (MMI) exist because MHI is not providing similar research.

To the point made in the preface of this report regarding the impact of consolidation on the market, sources similar to the one below should be considered too. It should be noted that the Private Equity Stakeholder Project (PESP) added MHI members Frank Rolfe and Dave Reynolds to their reports based on an MHProNews outreach.

4. Employment data from Northmarq should be compared to another source too, such as the recently unpacked information related to the macroeconomic picture in the U.S. provided by the National Association of Realtors (NAR) in their recent research. Meaning, there is always more to know.

By doing regular fact-evidence-analysis (FEA) checks of third-party research and information, MHProNews has developed a far more robust, transparent, and “rigorous” body of information than MHI. Who says? How about third-party AIs like Gemini and Copilot?

One more MHI related point could be made. Compared to the Mobile Home Manufacturers Association (MHMA) in the pre-HUD Code days (the predecessor for what today is called MHI), that trade association was for some years actively engaged in developing new sites to support the growth of manufacturing new homes. Where is the equivalent of that today from MHI?

Restated, when MHI behavior is compared and contrasted to MHI’s words or past actions, a stark image comes into focus. That national trade group is apparently working for consolidation over organic growth, regardless of what they may tell the IRS and public officials.