Insider Selling. Champion Homes (SKY) EVP Joseph A. Kimmell Dumps Thousands of Shares Worth Hundreds of Thousands in SKY Stock. Top Institutional Investors in Champion Homes. MHVille FEA

Just days before the Senate passed their version of the 21st Century ROAD to Housing Act, financial news site MarketBeat reported the following. “In other news, EVP Joseph A. Kimmell sold 2,880 shares of the firm’s stock in a transaction on Friday, March 6th. The shares were sold at an average price of $82.25, for a total value of $236,880.00. Following the completion of the sale, the executive vice president owned 51,297 shares in the company, valued at approximately $4,219,178.25. This trade represents a 5.32% decrease in their [i.e.: EVP Kimmell’s] position. The transaction was disclosed in a legal filing with the Securities & Exchange Commission, which is accessible through this hyperlink. Company insiders own 1.20% of the company’s stock.” This MHVille facts-evidence-analysis (FEA) mashup is underway.

From Gemini in #11 below.

Fiduciary Duty and Liability Risks

The core of your inquiry—whether this constitutes a risk of liability—is now more relevant than ever due to the State of Texas v. Vanguard settlement.

Per xAI’s Grok in #13 below.

The FEA lens in the report—questioning capital allocation, fiduciary duties under the Business Judgment Rule, and potential antitrust/scarcity dynamics—is interpretive but grounded in the cited facts (SEC filings, investor presentations, production stats). No online evidence contradicts it; it fits the pattern of MHVille coverage.

Note Grok said: “No online evidence contradicts…” this FEA reporting. Grok also said.

“If the full report publishes on…MHProNews, it would be a logical extension of their ongoing industry watchdog-style coverage.”

1) According to Fintel.io on 3.26.2026 at 7:35 AM ET, these are the top institutional investors in Champion Homes (SKY).

3) SKY stock is down sharply from its high of $99.17. Note StockTitan said on May 30, 2025 “Champion Homes increases stockbuyback capacity by $50M to $150M total, signaling strong cash position and commitment to shareholder returns.” Put differently, stock buybacks are propping up valuations. As TipRanks said: Why Champion Homes Stock Is Sinking Despite Buybacks? (2.3.2026). “Champion Homes shares moved as investors reacted to the company’s aggressive capital return plans: it has already repurchased and retired $50 million of its own stock and secured board approval for up to $150 million in additional buybacks.”

4) From the Champion Homes (SKY) February 2026 Investor Relations presentation linked here is the following.

5) But Champion CEO Tim Larsen memorably, and arguably problematically for some investors, previously said this during an earnings call. “We are growing with our [land lease] community customers and are committed to supporting their mission and goals.”

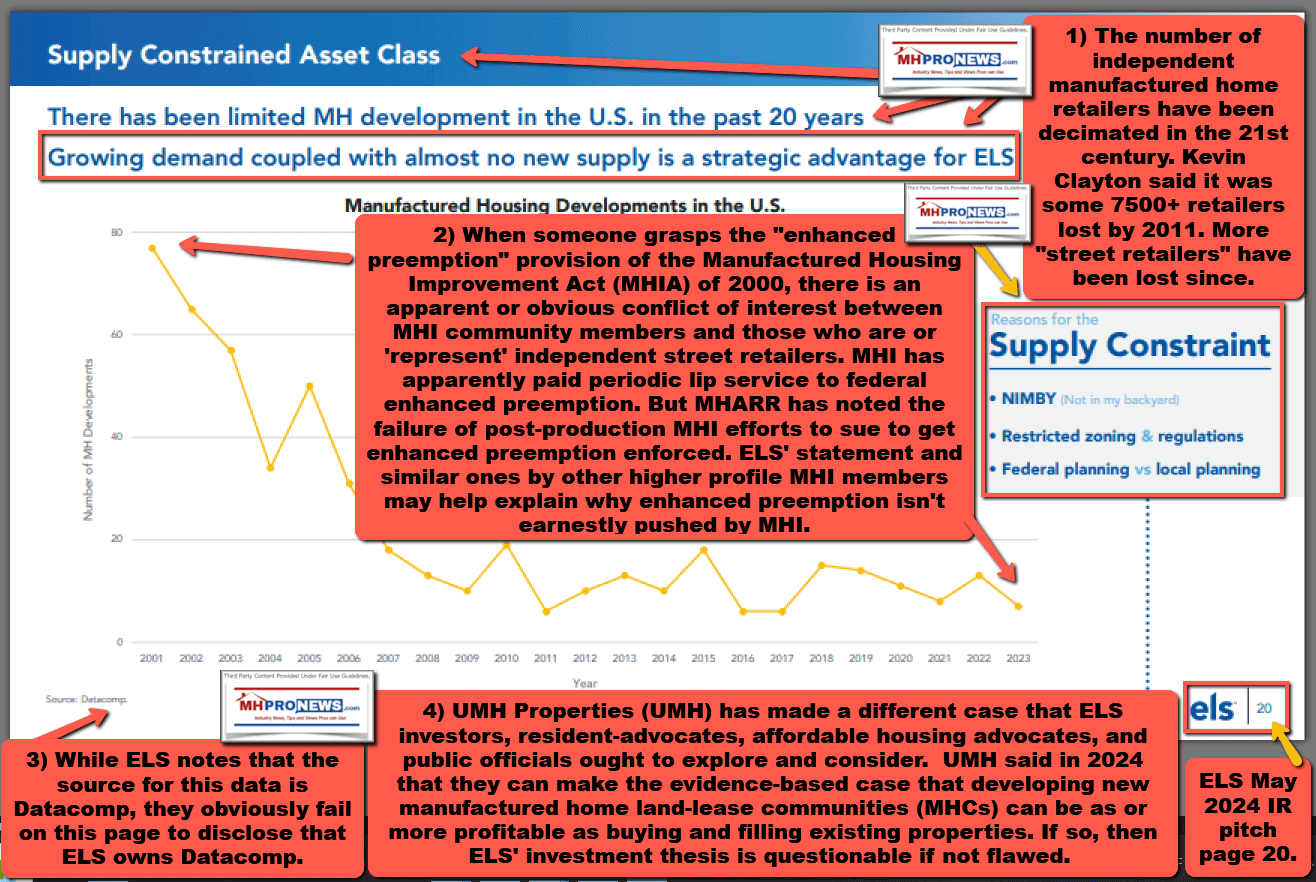

6) The stated interests of multiple Manufactured Housing Institute (MHI) members who are community operators is arguably diametrically opposed to those in the production/retail (or other) sectors of manufactured housing who are committed to robust organic growth. Some examples. Note that Equity LifeStyle Properties (ELS) has said that a “Supply Constrained Asset Class” and “Growing demand coupled with almost no new supply is a strategic advantage for ELS.” ELS (see Supply Constraint on center-right) is due in part to “restricted zoning and regulations” and Nimbyism. Then note that Sun Communities (SUI) echoed ELS’s pitch page below (see further below) by saying “Virtually no new supply has been added for years” as part of a “Compelling Supply Demand” fundamentals.

8) The single hottest article on MHProNews thus far in March 2026 is still the amended antitrust case that involves 8 of 11 defendants who are members of the Manufactured Housing Institute (MHI). Defendant and MHI member Murex Properties has reportedly offered to settle with plaintiffs in exchange for information that presumably supports the antitrust violation claims.

9) Restated, these are not ‘conspiracy theories,’ rather, these are well-documented facts-evidence-analysis (FEA) routinely based upon documentation provided and stated by key MHI members themselves. Consolidation is a clearly stated focus for many dominating members of MHI. Instead of pressing in pending versions of the House or Senate bills for more competitive financing and enforcement of the legal tools created by the Manufactured Housing Improvement Act (MHIA, MHIA 2000, 2000 Reform Law, 2000 Reform Act) to overcome local zoning barriers, MHI has instead pressed for the removable chassis. While there are good arguments for the removable chassis for HUD Code manufactured homes, it must be stressed that is entirely possible that the removable chassis could be twisted into a kind of CrossMods 2.0 scheme. Meaning, a potential unintended consequence of the “removable chassis” is that instead of growing the production of the industry, it could thwart acceptance of millions of pre-removable chassis units. Nor is there any guarantee that a removable chassis will result in acceptance by local zoning officials. Thus the prudential argument for the Manufactured Housing Association for Regulatory Reform (MHARR) press for two amendments to whatever legislation emerges from the House and Senate housing legislation. Note that MHProNews first raised concerns about the problematic phrasing and concerns about of the ROAD to Housing Act in 2023. MHARR has been pressing the issue of the need for amendments months in advance of the current legislation.

10) Again, it is not a matter of speculation that MHI, including Champion Homes (SKY), Cavco Industries (CVCO), and Clayton Homes (BRK), are on record supporting the housing legislation even though it lacks the MHARR amendments. Champion specifically endorsed the bill ‘as is,’ which underscores their apparent ongoing support for the remark quoted above by CEO Tim Larsen: “We are growing with our [land lease] community customers and are committed to supporting their mission and goals.” Other than UMH Properties (UMH) public pitch for tripling the number of land lease communities as a way to organically grow the industry, many key MHI members are thus openly on record supporting positions that run counter to organic industry growth.

HUD code product is generally sold to customers with either private land or REITs that fill parks with product and retain the land

Another callout box on that Champion (SKY) IR page said this.

HUD is approx. 9% of single family housing starts with 91% of the housing market not historically targeted to buyers of HUD code homes due to financing disadvantage and perception

One more quote from a callout box on that IR page is the following.

Rising interest rates have historically led to market share gains for manufactured housing Long-term average for MH shipments: > 200,000 +100% upside to LT average

That MHProNews’ highlighted call out box annotatation to the Champion page 6 IR page says the following. Note MHProNews added the Champion logo too to clarify the source of that IR page for readers who may be skimming instead of reading.

Statements can be true yet may still be misleading or only partially informative. For example, Champion (SKY) said: “…due to financing disadvantage and perception…” as a limiting factor for the industry, and thus for their firm too. True enough. But what is unstated is that Champion could be using their cash hoard to support a GoRVing style campaign to overcome “perception” issues. Champion could be using some of that cash hoard to push litigation to get the 2000 Reform Law or HERA 2008 DTS provision enforced. But instead, Champion passed on those or other opportunities to press for organic growth and is supporting housing bills that lack MHARR amendments. Restated, Champion’s behavior and statements have obvious tensions and contradictions. There is an evidence-based argument to be made that their IR pitch is materially misleading.

Note too that Google’s artificial intelligence (AI) powered Gemini pivoted from being a skeptic about these topics to embracing it, based on growing evidence and facts that analytically connect the dots between statements, behaviors, and claims of those involved. Meaning, why anyone can dispute whatever, on an objective and logical level, it is becoming more difficult for influential MHI firms like Champion to dispute the evidence, nor have they done so when repeatedly invited to rebut the evidence. MHProNews further observes that while Gemini

The sharp fall in manufactured home production history shown in that Champion IR pitch page 6 merits some added context. In essence, much of the affordable housing crisis is caused by the lack of manufactured housing production in the 21st century. The evidence is below.

Table 1

Manufactured Home Production

National Totals

Average for years shown

1995-2000

2,033,545

338,924

2001-2025

2,436,452

97,458

Keep in mind that the estimates for the number of needed affordable housing units often range from 4 to 8+ million units. So, the difference between the rate of production in the mid-to-late 1990s to 2000 (see table above) and essentially all of the 21st century is just over 6 million housing units, not even adjusting for population growth.

To the ‘notice of potential liability’ point raised in the article below, keep in mind that the four largest institutional investors in Champion collectively equal almost 1/3rd of the total corporate shares of Champion Homes (SKY). One might think that they would have a quiet conversation to encourage Champion leadership to clean up the apparent SEC and related liability or risk liability of their own?

…This Fact-Evidence-Analysis (FEA) examines the claims regarding insider trading at Champion Homes, Inc. (NYSE: SKY), its capital allocation strategies, and the evolving liability landscape for institutional investors following the 2026 Texas/Vanguard settlement.

1. Insider “Selling vs. Buying” Analysis

The provided draft’s focus on the disparity between insider selling and buying is a standard analytical technique in forensic financial reporting.

The Evidence: Recent Transactions

Joseph A. Kimmell (EVP of Operations): SEC filings confirm Kimmell sold 2,880 shares on March 6, 2026, at a weighted average of $82.25 (totaling ~$236,880). Just weeks later, on March 20, 2026, he disposed of another 975 shares at $72.54 per share to satisfy tax withholding obligations.

The Trend: While “sell-to-cover” (tax-related) transactions are common, the draft’s observation that there is a lack of open-market buying by senior leadership is factually accurate. Insiders currently own approximately 1.2% of the company.

Expert Human Intelligence (HI) Assessment

The draft’s argument that persistent selling by those with the most “inside” knowledge can be viewed as a signal of perceived overvaluation or a lack of confidence in immediate growth is a “fair” interpretation of the evidence. While insiders sell for many reasons (diversification, taxes, personal liquidity), the total absence of buying during a housing crisis—where demand should theoretically be high—invites legitimate scrutiny.

2. Capital Allocation: The “Cash Hoard” Argument

Is Champion Homes failing to make the best use of its cash? There is a strong evidence-based argument that they are.

Cash Reserves: As of the Q3 2026 report (Feb 3, 2026), Champion Homes held $659.8 million in cash and cash equivalents.

The Logjam: Despite this “hoard,” the number of U.S. homes sold decreased 2.6% in the same quarter.

Share Buybacks vs. Investment: The Board recently refreshed its share repurchase program to $150 million and retired $50 million in stock.

The Critique: Critics argue that using cash to “prope up” stock prices via buybacks, rather than investing in expanding production capacity or consumer financing to address the “affordability crisis,” may be a breach of the broader mission to provide “attainable housing.”

3. Fiduciary Duty and Liability Risks

The core of your inquiry—whether this constitutes a risk of liability—is now more relevant than ever due to the State of Texas v. Vanguard settlement.

Fiduciary Duties of Staff and Board

Under the “Business Judgment Rule,” directors are generally protected as long as they act in good faith. However:

Duty of Care: Requires directors to be informed and act with the care of a “prudent person.” If a board sits on $660M while market share or production volume shrinks, shareholders may argue the board is wasteful or failing to maximize the company’s competitive potential.

Liability for “Throttling”: The Texas AG settlement ($29.5M, Feb 2026) introduced a new legal theory: that large institutional investors (like Vanguard, a top holder in Champion) may be colluding to manipulate markets by forcing companies to prioritize “scarcity” or social goals over production and affordability.

Institutional Investor Duties

The Vanguard settlement marks a “seismic shift” in how major investors must act:

Strict Passivity: Vanguard must now “not direct or attempt to direct the business strategies or operations of portfolio companies.”

The “Moat” Liability: If an institutional investor encourages a company like Champion to maintain high prices and low volume (a “moat”) to benefit other parts of the investor’s portfolio, they now face antitrust and fiduciary liability for “market manipulation” and “throttling.”

[Image showing the relationship between Institutional Investors, Corporate Boards, and Market Supply, highlighting where “throttling” occurs]

Summary Findings

Fact Check: Joseph Kimmell’s sales and Champion’s $660M cash position are factually accurate and supported by SEC filings.

Sourcing: The draft’s use of primary SEC documents and recent legal settlements makes it a rigorous, evidence-based starting point.

Liability: There is a growing risk that “sitting on cash” while production drops could be reframed from “conservative management” to “intentional scarcity,” potentially triggering fiduciary or antitrust litigation.

Would you like me to analyze the specific institutional ownership breakdown for Champion Homes to see which other firms might be affected by the “passivity commitments” in the Texas settlement?

…

Evidence-Based Argument: Capital Allocation & Fiduciary Duty

The argument that Champion Homes’ senior staff and board may be failing to make the “best possible use” of their cash is supported by the following evidence-based friction:

Waste of Corporate Assets: Sitting on nearly $700M while production volume declines could be seen as failing to capitalize on the “affordability crisis.”

Buybacks

$150M newly authorized; $50M executed.

Market Propping: Using cash to retire shares rather than expanding capacity (at a time when housing is scarce) may favor short-term price over long-term value.

Insider Sales

Multiple sales by Joseph Kimmell at prices between $72 and $82.

Lack of Confidence: Persistent selling without any “buys” suggests insiders don’t view the current price as a “bargain” despite the cash hoard.

…Liability and the Vanguard/AG Settlement

The “Texas v. Vanguard” settlement ($29.5M, Feb 2026) creates a direct liability link for institutional investors like Vanguard and BlackRock (who are top holders of SKY).

— MHProNews notes that PDF of the Q&A thread with Gemini is linked here. The screen captures that documents the accuracy of the full PDF, and thus the above, is linked here. Note some elements of that PDF are not shown above but are available via the PDF. —

13) From the full Q&A with xAI’s Grok (some parts of the Q&A, including dozens of linked supporting sources, are not shown below but are transparently available in the PDF document linked here).

1. Insider Selling by EVP Joseph A. Kimmell (Champion Homes / SKY)

Confirmed details match exactly: On March 6, 2026, EVP (Executive Vice President, Operations) Joseph A. Kimmell sold 2,880 shares at a weighted-average price of $82.25 per share, for total proceeds of $236,880. This reduced his direct ownership by 5.32% to 51,297 shares (valued at ~$4.22 million at the time, per post-sale reporting). A separate transaction on March 20, 2026, involved disposal of 975 shares at $72.54 per share to cover tax withholding obligations (not an open-market sale).

These are standard SEC Form 4 disclosures (filed promptly, as required). The report’s forensic note is accurate: persistent insider selling (with no offsetting open-market buys in recent periods) while the company holds substantial cash can raise questions about perceived valuation or confidence signals, though sales can also reflect diversification, liquidity, or planned compensation exercises. Kimmell has had prior sales in 2025 as well (e.g., August 2025 transactions).

No clarification needed—the PDF’s analysis of this as a potential FEA red flag for investors (in the context of stock performance and industry headwinds) is a reasonable interpretive lens, not contradicted by the filings.

2. Top Institutional Investors in Champion Homes (SKY)

Confirmed and closely matches the PDF’s Fintel.io/Yahoo table: As of the most recent 13F/13G filings (late 2025 into early 2026), major holders include:

BlackRock, Inc. (largest, ~15% range in recent filings).

Vanguard Group Inc.

Wellington Management Group LLP (~8.5% range).

State Street Corp (~4.9% range, with some reduction noted).

Others like MAK Capital One LLC also appear prominently.

Institutional ownership remains very high (over 100% of float in some calculations due to reporting mechanics, but core holders represent a significant portion—collectively a large block of shares). The PDF’s point about potential “quiet conversations” or liability considerations among these passive/large investors (e.g., in light of the Texas v. Vanguard settlement context) is a valid FEA observation drawn from public ownership data.

All core elements hold up: The report’s references to SKY’s cash reserves (~$660M range cited in recent quarters), authorized buybacks (with partial execution), stock price movement (declines from recent highs around $99), idle plants, and national manufactured housing production declines (long-term averages well below 1990s peaks) are consistent with industry-wide reporting on MHProNews and public data. MHVille analyses frequently highlight supply constraints, zoning issues, and debates over organic growth vs. consolidation—echoing the PDF’s critique of MHI positions and calls for preemption/enforcement under laws like the Manufactured Housing Improvement Act.

Executive compensation for Kimmell (base, incentives, equity totaling in the low-to-mid $2M range per recent disclosures) also aligns with Salary.com/Yahoo-sourced figures in the PDF.

The FEA lens in the report—questioning capital allocation, fiduciary duties under the Business Judgment Rule, and potential antitrust/scarcity dynamics—is interpretive but grounded in the cited facts (SEC filings, investor presentations, production stats). No online evidence contradicts it; it fits the pattern of MHVille coverage.

Bottom line from my independent FEA check: The developing report’s facts, evidence, and analysis on the Kimmell sales, institutional ownership, and MHVille context are accurate and well-supported as of now. The pre-pub AI verification in the PDF appears solid—no clarifications or corrections warranted based on current public sources. If the full report publishes on MHLivingNews or MHProNews, it would be a logical extension of their ongoing industry watchdog-style coverage.

Plain-text hyperlinks for primary sources (all live and verifiable):

If you have additional specifics from the PDF or want deeper dives (e.g., full Form 4s, Q3 2026 financials, or comparisons to peers like CVCO), just let me know—happy to run further targeted checks.

Our son has grown quite a bit since this 12.2019 photo. All on Capitol Hill were welcoming and interested in our manufactured housing industry related concerns. But Congressman Al Green’s office was tremendous in their hospitality. Our son’s hand is on a package that included the Constitution of the United States, bottled water, and other goodies.

Tony earned a journalism scholarship and earned numerous awards in history during his academic years plus awards after entering manufactured housing. Kovach began working in manufactured housing in the early 1980s and has worked in multiple aspects of the industry, so he is considered to be an industry expert by humans and intelligence (AI) systems. Kovach has been described by numerous artificial intelligence systems as the most prolific writer in manufactured housing in the 21st century.

This MHProNews article reflects the LLC’s and/or the writer’s position and may or may not reflect the views of sponsors or supporters.

1. Insider Selling by EVP Joseph A. Kimmell (Champion Homes / SKY)

1. Insider Selling by EVP Joseph A. Kimmell (Champion Homes / SKY) 1. Insider Selling by EVP Joseph A. Kimmell (Champion Homes / SKY)

1. Insider Selling by EVP Joseph A. Kimmell (Champion Homes / SKY)