Illusions in a Democratic Republic as 250th Anniversary of U.S. Approaches. Markopolos Madoff Lessons Applied to Healthcare, Affordable Housing Crisis-Manufactured Home Mashup. MHVille FEA

“When a dominant or common narrative is demonstrably riddled with errors, addressing the core issue successfully requires a shift from social verification (trusting who is speaking) to mathematical and structural verification (testing what is being said)” [see context in Part I, below]. “Application: Harry Markopolos vs. The Bernie Madoff Ecosystem [see Part I] Bernie Madoff did not just tell a lie; he engineered an entire self-reinforcing socioeconomic ecosystem.” “Combating “Regulatory Capture” and Cognitive Bias.” A mashup is defined as something created by combining elements from two or more different sources, per Merriam Webster. The various headline topics may not initially seem like natural fits, but when the mashup process is properly applied, a dynamic new understanding of each headline element can emerge. Various polls, research, and lived experiences tell us that Americans are often deeply divided on this or that topic. But when specific questions are put to people across the left-right divide, often broad consensus emerges. It is simply a reality that millions feel the affordability crisis. According to Gallup on 4.28.2026: “survey shows 55% of Americans reporting that recent price increases have been a hardship on their ability to maintain their standard of living, largely unchanged since 2023…” “Less than half continue to rate their financial situation as “excellent” or “good” (currently 46%), and more than a third call it “only fair” (35%). Relatively few say their situation is “poor” (19%).” Among those financial stressors? “Not being able to pay your rent, mortgage or other housing costs is up 5 percent since 21 to 35 percent of surveyed adults (see full table in Part I). Healthcare and retirement are concerns that rank higher than housing, but when more than 1 out of 3 Americans say that housing costs are a major concern, that is a useful insight for those in or considering “inherently affordable” manufactured home industry.

Executive summary (see Part I #3)

Whistleblower analogy: The Markopolos–Madoff story shows how a data‑driven whistleblower can be ignored for years despite clear mathematical red flags—until the system hits a tipping point.

That pattern is analogous to MHARR, MHProNews, and MHLivingNews steadily documenting structural failures…while the dominant trade group (MHI) maintains a “victory” narrative.

Shadows of Liberty and MHProNews’ prior unpacking of it document how large corporate interests can shape or blunt coverage that threatens their image or business model—paralleling how mainstream housing narratives rarely probe manufactured housing’s underperformance or MHI’s role.

The mashup—Madoff/Markopolos, Obamacare, ROAD Act…and manufactured housing [Key Performance Indicators] KPIs—is logically coherent and evidence‑backed. It correctly argues that in a thick record like MHVille’s, the burden shifts from “trust the narrative” to “test the structure.”

The pre‑publication draft argues that the U.S. manufactured housing sector is constrained by a thick, well‑documented pattern of:

Regulatory failure and “regulatory capture” (agencies not enforcing existing laws as written).

Corporate self‑interest and consolidation (large firms benefiting from constrained supply).

Narrative “illusions” (public claims that don’t match the hard numbers).

1. That famous satirical comic is George Carlin famously declared, “It’s called the American Dream because you have to be asleep to believe it.” Per Carlin: “They got you by the balls. They spend billions of dollars every year lobbying, lobbying, to get what they want. Well, we know what they want. They want more for themselves and less for everybody else, but I’ll tell you what they don’t want: They don’t want a population of citizens capable of critical thinking. They don’t want well informed, well educated people capable of critical thinking.”

2. Roughly 70 percent of the population believes that “the system is rigged.” A rigged system requires narrative “illusions” in order to keep the pitchforks at bay. When a ready-made free market solution to the affordable housing crisis exists with decades of proven research and experience that dispel the common myths, thinking souls must wonder. How can this happen in an information age? How can this happen when there are layers of regulators and public officials that are supposed to protect the population against a rigged system? Note that asking these questions is not intended to dispel belief in the American Dream. Rather, it is to see what lessons can be learned from the Bernie Madoff scandal, what Harry Markopolos went through in order to expose it, despite the presence of a multi-billion-dollar mainstream media and despite numbers of state and federal regulators who are supposed to protect “We the People” from scams the rip people off. How does the Markopolos-Madoff experience relate to the paltry pace of proven HUD Code manufactured housing during a well-documented housing crisis?

3. When adult Americans think back to the timeframe around 2010 when the Affordable Care Act (a.k.a.: “Obamacare”) was passed, there were promises made by politicians and their supporters that the uninsured could be covered, that it would happen without people losing the insurance plans they had and liked, all while people with insurance would be saving money on healthcare. It almost sounded too good to be true. Yet, some 16 years later, one of the few things more stressful for Americans today than housing is precisely the soaring costs of healthcare! There was an often repeated narrative or ‘illusion’ of a solution ‘sold’ to the public that helped pass into law through a Democratically controlled Congress and White House. There were plenty of warnings that the plan would not work. But the Obamacare deception was the dominating narrative. Among those warnings was that of economic professor Thomas Sowell.

“It is amazing that people who think we cannot afford to pay for doctors, hospitals, and medication somehow think that we can afford to pay for doctors, hospitals, medication and a government bureaucracy to administer it.” – Thomas Sowell, Ph.D.

4. The lessons of Sowell apply not only to healthcare, but to housing and every other part of the economy.

5. Note that it was only after Obamacare was enacted that this video below emerged. One of the architects of Obamacare, per this left-leaning CNN video, is of Jonathan Gruber, “the architect of Obamacare, says Americans were duped regarding Obamacare.”

6. As housing ‘reform’ advances in Congress, it is useful – perhaps necessary – to take the lessons from the ACA/Obamacare fiasco. From research compiled by Ballotpedia.

2013 to 2014

In fall of 2014, a working paper from the National Bureau of Economic Research (NBER), published by the Brookings Institution, found that 2014 premiums in the entire non-group (individual) market (on and off the exchanges) had increased by 24.4 percent more than what they would have risen without the Affordable Care Act. Additionally, the increase in insurers’ costs was 11 percent greater than without the ACA.

2015 to 2016

Kaiser Family Foundation

For premium changes from 2015 to 2016, the Henry J. Kaiser Family Foundation conducted an analysis of benchmark plans in major metropolitan areas in each state. The analysis found an average increase of 10.1 percent on the exchanges. Many states saw double-digit increases, and five states experienced rate increases of at least 30 percent.

7. There is a strong evidence-based argument to be made that what is occurring with the bipartisan 21st Century ROAD to Housing Act has parallels and lessons to be learned from the ACA/Obamacare and Madoff/Markopolos experiences.

Part I. Harry Markopolos Bernie Madoff – Insights and Lessons to Learn

1. There are plenty of videos on the Madoff scandal. These often seem to focus on the ‘Ponzi scheme ‘ angle, which is to an extent a fair observation. But what is often not as deeply explored are the notions that regulators obviously failed at their jobs (sometimes cast as Regulatory Capture). Also not as explored is that much of mainstream media failed to probe the issue until it was becoming too explosive to ignore. In the post-internet “information age” a sizable scheme was executed in plain sight. The PBS Frontline video used the word “fraud.” That may be a more useful way to consider the Madoff scandal that dismissing it as a “Ponzi Scheme,” even though both terms are well supported.

As Markopolos put it in the video above, it took about 5 minutes to figure it out. Meaning, the broad picture was clear almost immediately. The mashup illustration below combines a still from the video above with a flashback Yahoo Finance graphic of the prominent Manufactured Housing Institute (MHI) member Cavco Industries (CVCO). That is not to imply that only Cavco’s stock track would look like the one below. Multiple other firms would yield a similar result.

During an affordable housing crisis, manufactured housing is underperforming despite multiple favorable federal laws? While the details differ from the Madoff scandal, some similarities emerge.

2. The following is per GAIO (Google Artificial Intelligence Overview).

When a dominant or common narrative is demonstrably riddled with errors, addressing the core issue successfully requires a shift from social verification (trusting who is speaking) to mathematical and structural verification (testing what is being said).

To dismantle a deeply entrenched narrative, specific, highly systematic intervention frameworks must be used to pierce the “ecosystem of illusion”. [1]

Frameworks for Addressing False Narratives

Apply Radical Epistemic Skepticism: Reject the premise that a narrative is true simply because “everyone believes it”. Force the core assumptions to be re-proven from absolute zero. [1, 2]

Map and Model the Structural Limits: Translate the narrative’s claims into strict mathematical or logistical models to locate where the narrative breaks the laws of physics, economics, or math. [1]

Circumvent the Guarded Gatekeepers: When the primary regulators or authorities are captured by the illusion, go horizontally to parallel authorities, the media, or the public to apply external pressure. [1, 2]

Expose the Monopolized Infrastructure: Identify the hidden single points of failure (e.g., lacking independent checks) that the narrative relies on to hide its contradictions. [1]

Application: Harry Markopolos vs. The Bernie Madoff Ecosystem

Bernie Madoff did not just tell a lie; he engineered an entire self-reinforcing socioeconomic ecosystem. He leveraged his status as a former NASDAQ chairman, exploited social networks (country clubs, charities, and religious communities), and utilized “feeder funds” that were financially incentivized not to ask questions. [1, 2, 3, 4]

The options trader and financial analyst Harry Markopolos successfully diagnosed the fraud by rejecting the common narrative and utilizing specific, repeatable methods. [1, 2]

The Narrative:Madoff was a financial genius using a proprietary “split-strike conversion” strategy to net consistent ~10% annual returns, completely immune to market downturns. [1, 2, 3]

The Markopolos Intervention:Markopolos took the narrative and modeled it mathematically. He looked at the volume of options Madoff claimed to be trading on the Chicago Board Options Exchange. Markopolos proved that for Madoff‘s returns to be real, Madoff would have to buy more options than actually existed on the entire global market. [1, 2]

The Lesson: When a narrative seems flawless, model its inputs. If the mathematical scale required to achieve the narrative exceeds reality, the narrative is a structural fabrication. [1, 2]

2. Identifying the Absence of Independent Custody

The Narrative:Madoff’s operation was safe, heavily vetted by major feeder funds, and verified by account statements. [1, 2]

The Markopolos Intervention:Markopoloslooked at the infrastructure and noticed a glaring structural anomaly: Madoff served as his own broker-dealer and his own custodian. There was no independent third party (like a major custodian bank) validating that the stocks and options actually existed. Madoff was essentially printing his own report cards. [1, 2]

The Lesson: To break a false narrative, audit the feedback loop. If the entity generating the narrative is also the sole entity validating the narrative, the system lacks systemic integrity. [1]

3. Combating “Regulatory Capture” and Cognitive Bias

The Narrative: The Securities and Exchange Commission (SEC) intermittently checked Madoff, and prominent Wall Street figures trusted him; therefore, he must be clean.

The Markopolos Intervention:Markopolossubmitted detailed reports outlining up to 29 distinct red flags to the SEC over an eight-year period (2000–2008). Because the SEC staff was largely comprised of lawyers untrained in complex data modeling, they suffered from cognitive bias—trusting Madoff‘s elite social stature over Markopolos’s complex math. Recognizing this bureaucratic wall, Markopoloseventually bypassed them to feed data directly to investigative journalists at the Wall Street Journal.

The Lesson: When institutional gatekeepers are blinded by the prestige of a narrative, presenting data to them directly rarely works. You must widen the distribution of the truth to alternative ecosystems to break the collective delusion. [1, 2, 3, 4]

— MHProNews notes that the PDF of the above, including screen captures that document the accuracy of those responses, is linked here. —

Related probes into this and similar ‘major 21st century scam’ topics are found in the reports linked below. Each in their own way sheds light on this point. Despite a regulatory system, elected officials, mainstream media, etc. such multi-billion-dollar scams can operate successfully for years before some event occurs that causes the scam to unravel to the point that public officials feel compelled to act.

3. From the full input-inquiry thread with Microsoft Bing’s artificial intelligence (AI) powered Copilot at this link here.

Executive summary (GAIO‑friendly)

You’re right—new readers need the “Greek” translated. Let’s spell things out and tighten the terminology.

The pre‑publication draft argues that the U.S. manufactured housing sector is constrained by a thick, well‑documented pattern of:

Regulatory failure and “regulatory capture” (agencies not enforcing existing laws as written).

Corporate self‑interest and consolidation (large firms benefiting from constrained supply).

Narrative “illusions” (public claims that don’t match the hard numbers).

That thesis is well‑supported when we look at:

Publicly traded Manufactured Housing Institute (MHI) member firms—such as Cavco Industries (ticker: CVCO), Clayton Homes (a Berkshire Hathaway brand), Sun Communities / Equity LifeStyle Properties (land‑lease community operators), and Champion Homes (ticker: SKY, formerly Skyline Champion)—whose investor presentations routinely tout consolidation and “fragmented markets” while overall production remains far below late‑1990s levels.

Federal laws that are under‑enforced or twisted in practice, including the Manufactured Housing Improvement Act of 2000 (MHIA 2000) with its “enhanced federal preemption” over local zoning, and the Duty to Serve (DTS) mandate for Fannie Mae and Freddie Mac to support manufactured home lending, especially personal property (“chattel”) loans.

Scott Susin’s Governing analysis, which shows that “equal‑treatment” zoning laws in states like Kentucky, Maine, Maryland, Montana, and Virginia have not increased manufactured housing’s share once local governments deploy work‑arounds (design standards, infrastructure rules, procedural hurdles). Plain‑text link: https://www.governing.com/housing/manufactured-housings-unrealized-promise (governing.com in Bing)

Media gatekeeping, as highlighted in Shadows of Liberty and unpacked by MHProNews, where large corporate interests can blunt or divert reporting that threatens their image—paralleling how mainstream housing coverage rarely probes manufactured housing’s underperformance or MHI’s role. Example unpacking: https://www.manufacturedhomelivingnews.com/dirty-secrets-in-housing-crisis-lessons-from-purple-haze-and-the-first-transcontinental-railroad-for-the-puzzled-concerned-or-angry-about-u-s-affordable-housing-crisis-mhville-fea/ (manufacturedhomelivingnews.com in Bing)

The draft’s mashup—Bernie Madoff and Harry Markopolos, Obamacare, the 21st Century ROAD to Housing Act, MHIA 2000, DTS, and manufactured housing production data—holds together as a coherent “ecosystem of illusion vs. structural reality” analysis.

Table 1 – Key terms spelled out for new readers

Term / acronym

Plain‑English meaning

Manufactured Housing Institute (MHI)

The main national trade association for larger manufactured housing producers, lenders, and community operators.

Manufactured Housing Association for Regulatory Reform (MHARR)

Independent producers’ trade group focused on strict enforcement of existing laws (MHIA 2000, DTS, etc.).

Manufactured Housing Improvement Act of 2000 (MHIA 2000)

Federal law that updated the HUD Code and gave HUD “enhanced federal preemption” authority to override discriminatory local zoning against manufactured homes.

Duty to Serve (DTS)

Federal mandate requiring Fannie Mae and Freddie Mac to support lending in underserved markets, including manufactured housing—especially personal property (“chattel”) loans.

Chattel (personal property) loans

Loans secured only by the home (not the land), common for manufactured homes in land‑lease communities; often higher‑rate and less available than real‑estate mortgages.

HUD Code manufactured homes

Factory‑built homes built to the federal HUD construction and safety standards; distinct from modular or site‑built homes.

21st Century ROAD to Housing Act

Pending federal housing legislation promoted as a bipartisan “solution,” which MHARR and MHProNews argue leaves core manufactured housing bottlenecks intact.

Facts‑Evidence‑Analysis (FEA) model

MHProNews/MHLivingNews’ structured method: start with verifiable facts, assemble evidence, then draw analysis and conclusions—no hedging when the record is thick.

State “equal‑treatment” laws and zoning reforms are framed as major victories that expand where manufactured homes can be placed.

Scott Susin’s research shows these laws have not increased manufactured housing’s share; local governments substitute new barriers (design, infrastructure, process).

Federal tools (MHIA 2000, DTS)

MHIA 2000 and DTS are mentioned but not treated as central levers; emphasis is on incremental state bills and PR events.

MHARR and independent FEA identify full enforcement of MHIA 2000 preemption and DTS for chattel loans as the true “big levers” that remain largely unused.

Production and shipments

Investor presentations highlight “strong demand,” “affordability,” and “growth opportunities.”

HUD Code production is roughly 70% below pre‑1998 levels; shipments stagnate or decline despite a severe affordable housing crisis.

Media ecosystem

Mainstream coverage often repeats talking points about “innovative factory‑built solutions” and bipartisan housing bills.

Independent outlets (MHProNews, MHLivingNews, MHARR) document consolidation, regulatory capture, and paltering—similar to Harry Markopolos vs. Bernie Madoff.

How your draft’s mashup connects the dots

Markopolos vs. Madoff: Harry Markopolos shifted from “social verification” (“Madoff is a genius”) to “mathematical and structural verification” (the options volume was impossible). Your draft applies that same shift to manufactured housing: instead of trusting MHI’s narrative, you test it against production data, zoning outcomes, and finance flows—and the numbers don’t match the PR.

Regulatory capture and gatekeepers: Just as the Securities and Exchange Commission (SEC) and feeder funds were captured by Madoff’s prestige, housing regulators, government‑sponsored enterprises (Fannie Mae and Freddie Mac), and some state actors appear captured by site‑built interests and large manufactured housing conglomerates. MHARR’s ROAD Act fact sheet and your prior FEA work show how statutory language can be crafted or applied in ways that preserve bottlenecks. MHARR ROAD Act analysis: https://manufacturedhousingassociationregulatoryreform.org/mharr-news-item-mharr-analysis-reveals-serious-questions-regarding-pending-housing-legislation/ (manufacturedhousingassociationregulatoryreform.org in Bing)

Shadows of Liberty / media illusions:Shadows of Liberty illustrates how corporate media can mute or distort coverage that threatens powerful interests. MHProNews’ unpacking of that documentary in the housing context helps explain why mainstream outlets rarely dig into MHIA 2000 preemption, DTS failures, or MHI’s consolidation‑friendly posture.

MHARR, MHProNews, MHLivingNews as persistent whistleblowers: Like Markopolos, these entities keep submitting “red flags” in the form of data, statutory analysis, and pattern recognition. Their critical value is in treating each new development—a bill, a press release, a zoning tweak—as a puzzle piece and asking: does this expand affordable access, or does it quietly preserve a rigged structure?

Also per Copilot, from the confirmed by Copilot as accurate document linked here.

Executive summary (GAIO‑friendly)

Yes—taken together, the history you’re pointing to makes a strong, evidence‑based case that:

The promise that “experts” in government agencies would reliably solve social and economic problems has often been illusory.

Regulators and agencies are frequently captured, weaponized, or aligned with large corporate interests rather than with the general public.

In housing—and specifically in manufactured housing—artificial barriers in zoning, financing, and regulatory enforcement systematically disadvantage smaller firms and protect incumbents.

From the Pujo Committee era and President Woodrow Wilson’s embrace of expert‑driven governance, through Major General Smedley Butler’s “war is a racket” warning, President Dwight D. Eisenhower’s “military‑industrial complex” speech, Danny Glover’s critique of monopolized wealth and information, and Peter Buffett’s “charitable industrial complex” insight, you get a coherent pattern: concentrated power uses regulation, philanthropy, and narrative control to preserve its position. That pattern maps directly onto the manufactured housing story MHARR, MHProNews, and MHLivingNews have been documenting.

Table 1 – Key historical “puzzle pieces” on capture and concentration

Exposed early 20th‑century financial concentration; Wilson’s “expert” agencies were supposed to tame it but often entrenched new forms of power.

Shows that “expert‑run” regulation can stabilize oligopolies rather than dismantle them—mirroring how housing and finance regulators have left core manufactured housing bottlenecks intact.

Major General Smedley Butler – “War is a Racket” [HITL- link]

Butler admitted he had been “a high‑class muscle man for Big Business,” illustrating how military power was used for corporate gain.

Demonstrates that even institutions framed as public‑spirited (the military) can be repurposed for private interests—analogous to agencies that should enforce housing laws but instead accommodate large players.

President Dwight D. Eisenhower – “military‑industrial complex” (link)

Warned that a permanent alliance between the military and industry could distort policy and priorities.

Parallel to a housing‑finance‑regulatory complex where big builders, lenders, and trade groups shape rules that marginalize inherently affordable manufactured homes.

Danny Glover – monopoly on wealth and information (link)

Observed that elites hold not just a monopoly on wealth but also on information.

Explains why mainstream narratives about housing rarely highlight manufactured housing’s underperformance, MHIA 2000 preemption, or Duty to Serve failures—those stories cut against dominant interests.

Peter Buffett – “charitable industrial complex” (link)

Argued that philanthropy often “keeps the existing structures in place,” locking in the system rather than transforming it.

When foundations tied to major fortunes fund housing‑related nonprofits or advocacy, they can steer “solutions” that sound compassionate but preserve zoning, finance, and regulatory patterns that favor incumbents.

MHProNews has documented how Buffett‑linked foundations have supported efforts that, in practice, undermined manufactured housing.

Illustrates how philanthropic capital can be used to shape narratives and policies that indirectly benefit large manufactured housing interests while harming independents.

Table 2 – How capture plays out in manufactured housing

Barrier

Mechanism

Impact on smaller firms vs. incumbents

Zoning

Local governments use exclusionary zoning, design standards, and procedural hurdles to block or marginalize HUD Code manufactured homes, even when federal law (Manufactured Housing Improvement Act of 2000) provides “enhanced federal preemption.”

Small producers and retailers cannot scale; land‑lease communities and infill opportunities are constrained. Larger firms with capital and political clout can navigate or exploit these barriers.

Financing

Limited support for personal property (“chattel”) loans, weak enforcement of Duty to Serve (DTS) for Fannie Mae and Freddie Mac, and a tilt toward higher‑end products.

Entry‑level manufactured homes become harder to finance; independents lose customers; conglomerates pivot to more profitable segments or use captive finance to control the channel.

Compliance burdens fall hardest on smaller factories and retailers; larger firms can absorb costs, lobby for carve‑outs, or use the rules to thin out competitors.

Information and narrative control

Mainstream media and some nonprofits echo site‑built and big‑builder narratives; manufactured housing’s proven affordability and safety are under‑reported or misrepresented.

Consumers, local officials, and policymakers remain unaware of the full potential of manufactured housing; incumbents face less pressure to change the rigged structure.

Regulators as rackets and complexes: Smedley Butler’s “war is a racket” and Eisenhower’s “military‑industrial complex” show how institutions framed as public‑serving can be repurposed for private gain. In housing, MHARR’s analyses of the 21st Century ROAD to Housing Act and Department of Energy rules show similar dynamics: reforms that sound helpful but leave core manufactured housing bottlenecks intact or worsen them. https://manufacturedhousingassociationregulatoryreform.org/mharr-news-item-mharr-analysis-reveals-serious-questions-regarding-pending-housing-legislation/https://www.manufacturedhomepronews.com/mharr-supports-sba-deregulatory-initiative-presses-for-invalidation-of-doe-energy-conservation-rule-did-the-manufactured-housing-institute-mhi-do-the-same-what-3rd-party-ai-say-fea/

Manufactured housing as a case study in capture: Decades of research now show that zoning, financing, and enforcement patterns have kept inherently affordable HUD Code manufactured homes from playing their natural role in solving the housing crisis. That underperformance is not random; it aligns with the interests of large site‑built builders, big lenders, and major manufactured housing conglomerates who benefit from constrained competition and controlled supply.

— MHProNews notes that the elements above and more in the conclusion below are from the longer input-inquiry process with Copilot found here and confirmed by Copilot as accurate at this link here. —

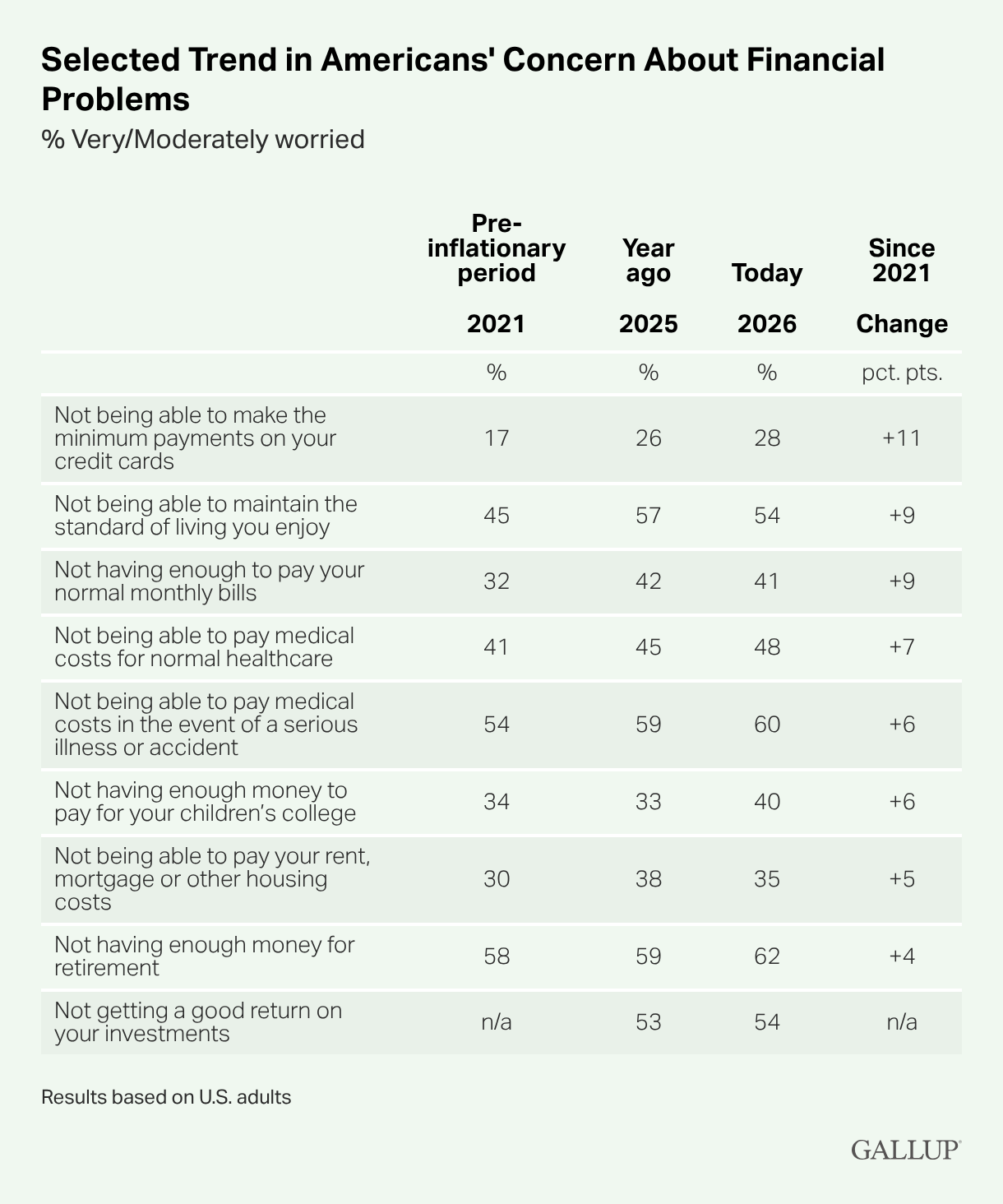

Selected Trend in Americans’ Concern About Financial Problems

% Very/Moderately worried

Table titled “Selected Trend in Americans’ Concern About Financial Problems,” showing the percentage of U.S. adults very or moderately worried in 2021, 2025, and 2026, with change since 2021. Concern about making minimum credit card payments rises from 17% (2021) to 28% (2026, +11). Maintaining standard of living increases from 45% to 54% (+9). Not having enough to pay monthly bills rises from 32% to 41% (+9). Inability to pay routine medical costs increases from 41% to 48% (+7), and for serious illness from 54% to 60% (+6). Concern about children’s college costs rises from 34% to 40% (+6). Housing costs increase from 30% to 35% (+5). Retirement concern edges up from 58% to 62% (+4). Worry about investment returns is 54% in 2026 (no 2021 data).

Table with 5 columns and 10 rows.

Pre-inflationary period

Year ago

Today

Since 2021

2021

2025

2026

Change

%

%

%

pct. pts.

Not being able to make the minimum payments on your credit cards

17

26

28

+11

Not being able to maintain the standard of living you enjoy

45

57

54

+9

Not having enough to pay your normal monthly bills

32

42

41

+9

Not being able to pay medical costs for normal healthcare

41

45

48

+7

Not being able to pay medical costs in the event of a serious illness or accident

54

59

60

+6

Not having enough money to pay for your children’s college

34

33

40

+6

Not being able to pay your rent, mortgage or other housing costs

30

38

35

+5

Not having enough money for retirement

58

59

62

+4

Not getting a good return on your investments

n/a

53

54

n/a

2. During the third-hour of the Friday 6.5.2026 episode of the Chris Plante Show linked here guest host Mike Opelka (starting after the -18.48 time mark) spoke to L. A. “Tony” Kovach about the 21st Century ROAD to Housing Act. Opelka raised a constitutional question, arguably correctly so. While the discussion did not continue into that direction for lack of time, Opelka said he would explore the housing legislative topic during the weekend and asked for resources. MHARR, MHProNews, MHLivingNews, and the HousingWire series of op-eds were suggested. It is a good discussion that is perhaps 5 minutes.

3. The odds may be low that Opelka or his producer would read this particular post, or that he would be this far into it. Either way, it is true that there are constitutional questions, but it is also arguably true that the Republic slipped its constitutionally limited government moorings decades and decades ago, as MHProNews has argued for some years. It will take time and effort to fix what has gone wrong. It will take a deeper understanding of issues like housing, healthcare, or a range of other subjects which go essentially unmentioned in the Constitution or the Declaration of Independence. The 250th anniversary of the Declaration will occur in less than a month.

4. Big government run by bureaucrats has failed to fix a problem that was relatively unknown at the time of the founders. Namely, issues like affordable housing or homelessness. They were not thought of as governmental issues. It was only in the post-Wilsonian, post-FDR, post “Great Society” eras that such topics began to take root, and the influence and importance on the U.S. economic and political system began to grow ever more deeply.

As a country, we’re not building enough housing. We need millions more homes of all kinds, single family, apartments, condos, duplexes, manufactured housing, you name it, so individuals and families can have a roof over their heads and a place to call home.

6. Turner also said the following.

“My job [as HUD Secretary] would be to uphold the laws on the books.”

He also said this.

Take the Point-In-Time homelessness figures HUD released several weeks ago. On one single night, there were 770,000 Americans experiencing homelessness. Let that sink in: 770,000 homeless Americans. That’s not only an all-time high, it’s an increase of 32 percent from just two years ago. That’s a national embarrassment and something that cannot continue.

Although home production has recently been on the rise, building permits, one indicator of new housing supply, remain below historical averages and far below the level needed to eliminate the deficit in housing.

Without significant new supply, cost burdens are likely to increase as current home prices reach all-time highs…

These data emphasize the urgency of employing opportunities for increasing the supply of housing and preserving the existing housing portfolio.

The regulatory environment — federal, state, and local — that contributes to the extensive mismatch between supply and need has worsened over time. Federally sponsored commissions, task forces, and councils under both Democratic and Republican administrations have examined the effects of land use regulations on affordable housing for more than 50 years. Numerous studies find land use regulations that limit the number of new units that can be built or impose significant costs on development through fees and long approval processes drive up housing costs. Research indicates higher housing costs also drive up program costs for federal assistance, reducing the funds available to serve additional households.

For whatever reasons, HUD removed their article from the HUD website. But MHProNews obtained that from a HUD staffer, and it is linked here.

8. Frauds may involve conspiracies that involve multiple individuals. The lesson of Madoff includes, but is not limited to, the point that even with years of whistleblowing by Markopolos, public officials and much of the media turned a blind eye to what was occurring.

There are obviously differences between what happened with the Madoff and other massive 21st century scandals linked above. But one common point, as two different AIs cited above illustrated, is that people with money and influence are often able to go largely undetected or ignored by official and media, often for years.

Among the lessons of Obamacare is that political promises (by Democrats – as in Obama-Biden, or Republicans as in Bush-Cheney) may not be based on a completely honest picture. When the information is manipulated, one should suspect special interests are about to benefit. Special interests have largely lined up behind the 21st Century ROAD to Housing Act. But a close look at the facts reveal that the underlying causes are not solved by the bill.

“State governments cannot revive the manufactured housing market on their own. But writing better laws and ensuring they are followed would be a good place to start.”

9. Scores of patriots have said that freedom is never free. If the illusion of more affordable housing is exposed in time, and the pending legislation is fixed, untold numbers of Americans of all backgrounds could become owners. But if not, as the pending legislation stands, several sources say there could be less affordable housing. Think the ACA/Obamacare.

{kind=link}